How to Find a Trusted Adult Platform to Browse Kurla Escorts Listings?

Other |

2026-06-03 08:30:02

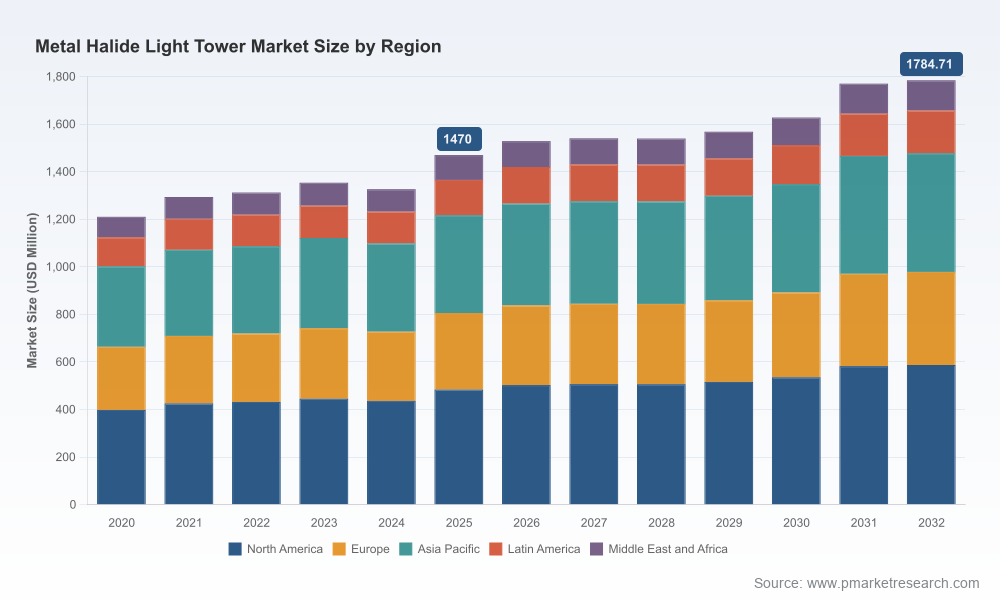

As capital planning cycles firm up for 2026, executives across OEMs, rental fleets, industrial end-users and private equity sponsors must reconcile a nuanced marketplace: stable, technically specialized demand that coexists with evolving regulatory and supply‑chain pressures. PW Consulting’s new Metal Halide Light Tower Market report (base year 2025; historical 2020–2025; forecast 2026–2032) provides a focused, practitioner‑oriented intelligence package to guide those decisions. The market reached approximately USD 1,470 million in 2025 and, at a compounded annual growth rate of 2.81% across the forecast window, is projected to approach USD 1,785 million by 2032. This briefing highlights the strategic value of that intelligence for 2026 without disclosing the granular segmentation tables reserved for report subscribers.

Metal Halide Light Tower Market

Capital allocation clarity: The report converts headline growth into investable signals—where to expand product lines, scale rental fleets, or prioritize aftermarket services within the metal halide segment.

Metal Halide Light Tower Market

Regulatory and operational alignment: We map emissions compliance (notably Tier 4 Final implications for diesel powertrains) to lifecycle cost modeling so procurement, engineering and compliance teams can coordinate capex and retrofit timelines.

Metal Halide Light Tower Market

Risk‑sensitive forecasts: Our scenario engine stresses the market against raw‑material shocks (specialized metal halides and quartz arc tube availability), policy shifts, and demand volatility from construction, mining and energy sectors.

Competitive choreography: A benchmarked view of incumbent and specialist manufacturers helps strategic teams prioritize partnerships, geographic focus and product roadmaps for 2026.

Prioritize niches where metal halide’s lumen density is non‑substitutable. Despite LED migration in many lighting applications, metal halide towers retain a technical advantage for very high‑lumen, large‑area illumination scenarios common in mining and certain oil & gas operations.

Plan fleet renewals around emissions compliance. For diesel‑powered assets, Tier 4 Final certification is now a procurement inflection point; retrofit costs and downtime assumptions materially affect total cost of ownership and rental rate design.

Hedge raw‑material exposure. Key lamp components remain concentrated in specialized supply chains; contingency sourcing and strategic inventory policies reduce vulnerability to price and delivery swings.

Extract aftermarket upside. With modest top‑line CAGR but high operational intensity, aftermarket services (spares, rapid repair, lamp refurbishment) are a high‑margin lever for OEMs and rental operators alike.

Embed modularity and electrification in new designs. Incremental product architectures that support both metal halide and alternative light sources — and offer battery or hybrid power options — provide flexibility as customer preferences evolve.

Top‑line market sizing and a seven‑year forecast built on granular demand drivers and scenario analysis (base year 2025; forecast 2026–2032).

Practical segmentation frameworks (by geography, product type, and application) with downloadable model templates—intended for integration into your finance and strategy planning tools. Note: detailed segment tables are accessible on our report page.

Unit economics and lifecycle cost models comparing purchase vs. rental, diesel vs. hybrid/electric configurations, and lamp technology tradeoffs.

Supplier scorecards and procurement playbooks that translate technical specs into negotiation levers and warranty strategies.

Aftermarket and service playbook, including SLA designs, parts stocking strategies and training curricula for field technicians.

Regulatory appendix outlining global emissions standards and anticipated compliance timelines that influence product certification and retrofitting.

Risk heatmaps covering raw material availability, regulatory shocks and demand concentration by end‑use sectors, with mitigation playbooks tailored for OEMs, rental houses and large industrial users.

The metal halide light tower market presents a mixture of global engineering leaders, localized specialists and rental‑focused manufacturers. Market concentration metrics indicate a moderately consolidated market (CR3 ~38.5%; CR5 ~52.3%), creating room for both scale advantages and targeted niche plays. The report’s vendor profiles and scorecards distill the strengths, product choices and strategic levers of the most relevant suppliers for 2026 planning.

Atlas Copco (Stockholm): Known for rugged HiLight series portable towers, Atlas Copco combines high‑output metal halide options with robust enclosures and service networks—an attractive partner for rental companies and quarry operators requiring durability.

Generac Mobile / Magnum (Waukesha, WI): The Magnum MLT models emphasize compact, vertical mast designs ideal for construction sites; their product positioning supports rental penetration where transportability and fast deployment matter.

Wacker Neuson (Munich): Focused on jobsite versatility, their LTV/LTS series deliver practical configurations for concrete pours and event lighting—an option that balances performance and lifecycle serviceability.

Grandwatt Electric Corp (USA/China operations): A supplier that combines standard catalog items with bespoke configurations, useful for projects with unusual power or mounting requirements.

Boss LTG (Baton Rouge): Trailer‑mounted, high‑lumen models aimed at large construction and industrial turnarounds where broad coverage and simple towability are priorities.

DMI Light Towers (Greenwell Springs): Large, multi‑fixture, high‑mast solutions for heavy industrial sites where one unit must illuminate many acres—this is a specialized, high‑value end of the market.

Trime USA: Builds mobile towers that combine field resilience with flexible lamp options—well‑positioned to serve regional rental fleets seeking reliable mid‑range assets.

Larson Electronics (Kemp, TX): Targets hazardous and general industrial markets with high‑lumen, rugged fixtures—an important name where compliance and certifications for hazardous locations are required.

Recent third‑party analysis (Analysts Insights releases in September 2025 and April 2026) aligns with our view: demand remains anchored in construction, mining and events, while supplier architectures are diversifying. PW Consulting’s marketplace mapping complements these studies with operationally actionable guidance—supplier scorecards, procurement levers and integration pathways for electrification and emissions compliance.

Raw materials: Metal halide lamps depend on specialized halide blends and precision glass/quartz components. Disruptions or price moves in these inputs can affect replacement lamp availability and aftermarket margins.

Regulation: For diesel‑powered towers, emissions standards (Tier 4 Final in the U.S. being a primary example) alter retrofit and procurement economics. Our models quantify breakpoints where electrified or hybrid alternatives become financially preferable.

Demand profile: The market is characterized by high utilization in certain applications (e.g., mining, large‑scale energy projects) and episodic peaks in construction and events—rental operators need sophisticated fleet orchestration to capture upside while managing idle assets.

Technology substitution: LEDs and distributed battery systems are encroaching in many lighting niches. However, for very high‑lumen demands over extensive areas, metal halide remains competitive today; the timing of substitution varies by application and total cost sensitivities.

For OEMs: Integrate modular architectures that allow quick swapping between metal halide and LED modules; standardize Tier‑compliant powertrains to lower certification costs.

For rental operators: Reassess fleet composition using our lifecycle models—optimize for utilization, retrofit costs and regional emission rules; pilot hybrid units where load profiles permit.

For industrial end‑users (mining, oil & gas): Tender specifications should include lifecycle cost metrics and retrofit clauses; negotiate extended parts warranties and rapid lamp replacement guarantees.

For investors: Target service‑oriented business models and companies with differentiated OEM partnerships or aftermarket advantage; look for vendors with credible electrification roadmaps.

PW Consulting’s market sizing uses a bottom‑up approach calibrated with supplier shipment data, rental fleet inventories, end‑user procurement records and primary interviews across the value chain. Historical datapoints span 2020–2025, the base year is 2025, and forecasts run to 2032. We supplement quantitative modeling with qualitative scenario analysis and supplier benchmarking; sensitivity tests include raw‑material price shocks, accelerated regulatory timelines and LED adoption curves.

This briefing emphasizes the strategic implications that should shape boardroom and capex conversations in 2026. To access the complete dataset, segmentation tables, vendor scorecards and downloadable financial models that underpin these conclusions, please consult the PW Consulting report landing page. The full report contains the granular inputs and practical tools your team will need to convert insight into action.

PW Consulting remains available for bespoke briefings, scenario workshops and implementation roadmaps tailored to your organization’s strategic priorities for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Metal Halide Light Tower Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com