PTFE Lined Dip Pipes Market — Strategic Preview for 2026 Decision-Making

As PW Consulting's Senior Strategy Advisor and Lead Industry Analyst, I present a focused strategic preview of our latest Ptfe Lined Dip Pipes Market report. This briefing outlines the high‑value takeaways senior executives, product leaders, procurement heads, and investment teams need to shape decisions in 2026. It highlights market momentum, competitive structure, supply‑chain levers, regulatory drivers, and the practical, executable intelligence contained in the full report — while intentionally withholding granular segment tables and regional/application breakdowns to protect the proprietary modeling that underpins our forecasts.

Ptfe Lined Dip Pipes Market

Market snapshot: growth trajectory and structural signals

The global PTFE lined dip pipes market has reached meaningful scale, with our base‑year assessment (2025) indicating a market size just below the USD 200 million threshold. Our 2026–2032 forecast period projects steady expansion at a compound annual growth rate (CAGR) of 5.2%, bringing the market to roughly USD 284 million by 2032 under the baseline scenario. This growth is sustained rather than speculative — driven by industrial corrosion‑mitigation upgrades, tightening environmental and containment regulations, and growing demand for high‑purity fluid handling in specialty sectors.

Ptfe Lined Dip Pipes Market

Two structural characteristics stand out for strategic planners. First, market concentration is moderate: the top three players together account for just under 40% of revenue, and the top five about half of the market. This creates a competitive environment where both scale and niche engineering capabilities matter. Second, the market’s growth profile is resilient but lumpy — annual expansion is steady overall, but product cycles, capital project timing in end markets, and raw‑material swings create episodic volatility that requires tactical agility from suppliers and buyers alike.

Ptfe Lined Dip Pipes Market

Why this matters for 2026 strategic choices

- Resource allocation for product and capacity investments. With mid‑single‑digit CAGR and predictable demand for upgraded corrosion‑proof systems, executives should prioritize incremental capacity that can be rapidly configured for variant demand rather than large, single‑purpose buildouts. Investment timing should be synchronized with regulatory waves and major capex cycles in chemical, pharmaceutical, and wastewater projects.

- M&A and partnership prioritization. The moderate concentration and the technical differentiation between continuous lined designs, jacketed solutions, and solid PTFE components make bolt‑on acquisitions and distribution partnerships high‑impact plays. Targets that add either proprietary lining technology or channel access in high‑growth end markets will be especially valuable.

- Procurement and margin resilience strategies. Raw material dynamics materially affect manufacturing economics: PTFE resin pricing volatility accounts for a large percentage of manufacturing cost for both solid and lined products, and lined configurations typically exhibit higher cost sensitivity. Supply contracts, dual‑sourcing strategies, and formula‑based pricing pass‑through clauses should be immediate priorities for procurement leaders.

What our report delivers — pragmatic, executable intelligence

The full PW Consulting report blends deep technical understanding with commercial rigor to produce decision‑ready outputs. Key deliverables include:

- Proprietary market-sizing and trend models calibrated to 2020–2025 historicals and stress‑tested against multiple macro and regulatory scenarios for 2026–2032.

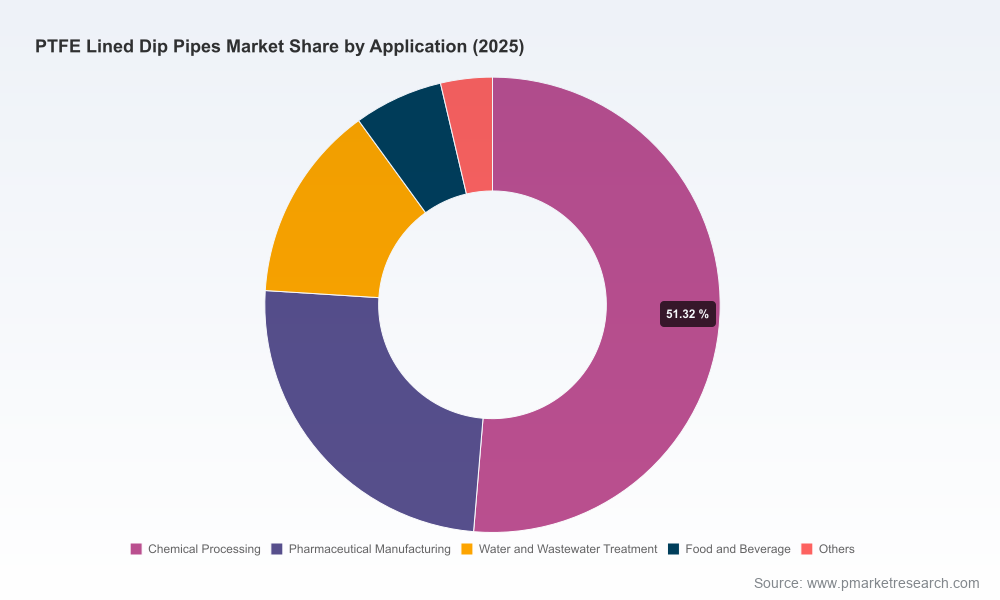

- Segment and subsegment assessment (by product configuration, end‑use class, and geographic cohort) with scenario forecasts, growth levers, and sensitivity matrices — withheld here to preserve competitive advantage and encourage report access.

- Unit‑economics playbooks for manufacturing and lining processes, including cost build‑ups, margin improvement pathways, and break‑even analyses for capacity additions and material substitutions.

- Supply‑chain heat maps that identify single‑point risks in resin sourcing, fabrication bottlenecks, and logistics constraints — each mapped to mitigation playbooks (e.g., hedging, strategic inventory, nearshoring).

- Commercial and pricing strategies: go‑to‑market frameworks for engineered vs. standard products, OEM partnerships, aftermarket and service monetization, and tender response playbooks for large capital projects.

- Regulatory and standards tracker with impact scenarios — from hazardous‑fluid containment rules to water treatment regulations — and a decision tree that quantifies regulatory uplift opportunities for suppliers.

- Competitive landscaping with company profiles, capability matrices, and prioritized M&A / JV target lists that account for technological differentiation, channel reach, and cost structure synergies.

- Risk register and early‑warning indicators for executives — covering raw material volatility, regulatory changes, and substitution threats — with pre‑mapped contingency actions.

Competitive landscape — who matters and why

Our qualitative and quantitative work identifies a set of core incumbents and specialist players that shape technology and access across end markets. Key differentiators we observed include lining technology (continuous vs. segmented linings), engineering for agitated/pressure service, and channel strength for high‑purity applications.

- Corrosion Resistant Products (CRP) — Known for continuously lined designs and engineering rigor for agitated reactor vessels. Their stress‑calculation approach for agitated service is a market differentiator for complex chemistries.

- Micromold Products, Inc. — Offers jacketed and lined steel solutions under established trade names, balancing standard portfolio depth with custom corrosion‑resistant configurations for larger nozzle interfaces.

- Andronaco Industries (Ethylene) — Provides branded ChemTite®/Ethylarmor® solutions engineered for high‑stress injection and agitated applications, making them a natural partner for clients running severe service chemistries.

- Edlon (GMM Pfaudler) — Focuses on high‑purity and glass‑lined integration use cases, with product literature targeting semiconductor and specialty chemical tanks.

- Regional fabricators and specialists (India and others) — Several smaller manufacturers and suppliers deliver competitive cost structures and localized service. These players are important for on‑the‑ground project execution and shorter lead‑times.

Strategically, the marketplace favors companies that combine credible engineering (lining adhesion, stress analysis, and agitation compatibility) with reliable channel relationships into higher‑value contracts. For suppliers, differentiating on service levels, lead times, and documentation for regulated industries can win pricing power even in a moderately concentrated market.

Supply chain, raw materials, and regulatory tailwinds

Two forces dominate near‑term dynamics: material cost volatility and regulatory tightening. Our analysis shows PTFE resin price swings are a primary cost driver, representing a significant portion of manufacturing cost for both solid and lined components; lined products tend to have higher cost sensitivity due to additional processing and quality controls. As a result, margin variability can be meaningful unless suppliers execute disciplined procurement and pass‑through strategies.

On the regulatory side, stricter containment rules and environmental compliance requirements — across chemical processing, water treatment, and specialty manufacturing — are a durable demand driver for corrosion‑proof, lined solutions. These regulations not only increase replacement and retrofit demand but also shift specification preferences toward products with robust traceability and testing documentation.

Recent market signals to watch in 2026

- Early‑2026 manufacturing updates emphasize improved adhesion technologies in lining processes — an incremental but meaningful quality lever that reduces delamination risk and extends service life.

- Late‑2025 partnership announcements expanded distribution for branded lined products, illustrating how channel alignment accelerates adoption in targeted end markets.

- Product guides and technical releases from established glass‑lined and high‑purity vendors highlight increasing attention on semiconductor and high‑purity chemical applications, revealing an opportunity to command premium pricing for validated, documented solutions.

These signals reinforce our view that incremental technical innovation, combined with strengthened channel distribution and compliance documentation, will generate outsized returns in 2026.

Practical moves for 2026 — a concise executive checklist

- Embed material‑price contingency into all project contracts and retender major supply agreements with indexed pricing clauses.

- Prioritize retrofit and service offerings with documented lifecycle benefits — warranty extensions and maintenance packages can be margin enhancers.

- Accelerate partnerships with distributors and engineering partners in target end markets to shorten sales cycles for capital projects.

- Screen M&A targets for lining IP, channel access, and fabrication scale; prefer targets that deliver both technological uplift and immediate commercial reach.

- Implement an early‑warning regulatory monitoring dashboard to quantify demand uplifts from compliance updates and adjust capacity plans accordingly.

Concluding perspective and next step

The PTFE lined dip pipes sector presents a clear, actionable opportunity set for companies that combine engineered differentiation with supply‑chain sophistication. The market is growing at an orderly pace (5.2% CAGR for 2026–2032), and a blend of regulatory mandates and material‑driven economics will determine winners and losers in 2026. PW Consulting’s full report provides the operational models, scenario analyses, and deal‑level guidance necessary to move from insight to execution. For the detailed regional and application splits, vendor market shares, and the proprietary scenario models that inform our headline forecasts, access the complete Pw Consulting Ptfe Lined Dip Pipes Market report.

Contact the PW Consulting report portal to obtain the report and our tailored executive briefing package, which includes a 60‑minute strategy workshop and a customized market‑entry or M&A roadmap aligned to your strategic priorities for 2026.

For detailed analysis of this topic, please visit the official page:Ptfe Lined Dip Pipes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com