Ophthalmic Operational Microscope Market Size, Share, Trends, and Industry Forecast by 2032

Other |

2026-06-05 11:10:23

As hyperscale AI workloads, cloud-native optics and carrier densification reshape the optical landscape, coherent optical modules are moving from niche long‑haul roles into the heart of data center interconnect (DCI), metro edge and AI-driven transport architectures. PW Consulting’s forthcoming Coherent Optical Module Market report (base year 2025, historical 2020–2025, forecast 2026–2032) synthesizes commercial realities and technology trajectories to help executives convert optical innovation into measurable business outcomes.

Coherent Optical Module Market

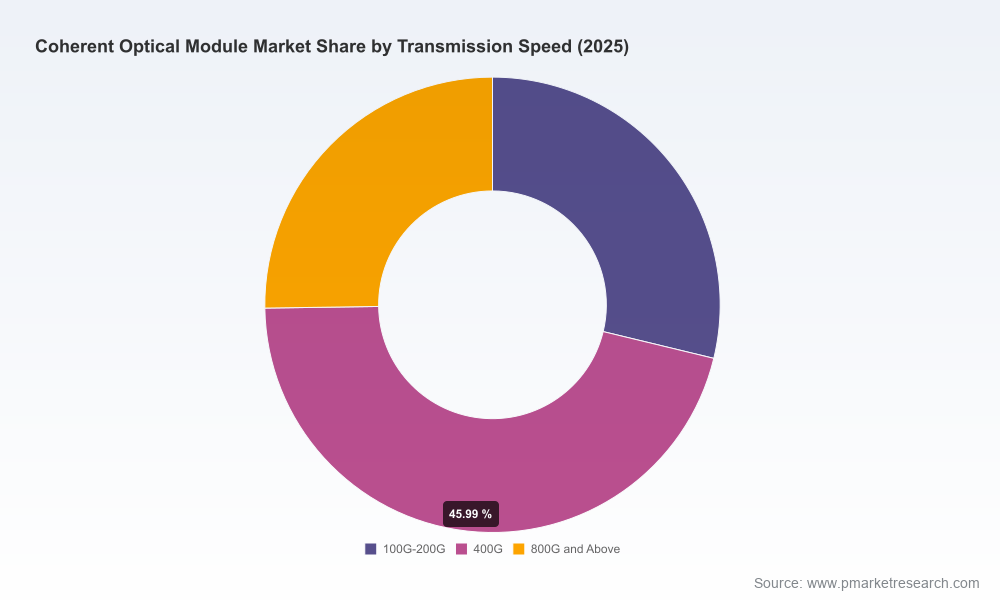

At the macro level, the market expanded from roughly USD 3.4 billion in 2020 to USD 6.25 billion in 2025, and our forecast projects sustained expansion at a compound annual growth rate (CAGR) of 13.52% through 2032, when the market surpasses USD 15.1 billion. Those topline dynamics mask important inflection points — migration to 400G and beyond in pluggables, the emergence of 1.6T+ coherent solutions for AI-scale fabrics, and a shifting concentration profile among leading suppliers — all of which the full report unpacks with practical guidance for 2026 decision cycles.

Coherent Optical Module Market

Technology adoption is accelerating: Pluggable coherent optics are no longer an experimental option for DCI and regional transport — they are a procurement imperative for organizations balancing capital and operating cost pressures. Timing of integration and compatibility with existing fiber plant will determine near‑term TCO and upgrade paths.

Coherent Optical Module Market

Power and space economics have become determinative. Energy and infrastructure costs at scale — exemplified by rapidly growing electricity demand from U.S. data centers and the high annual cost to power a single high‑density AI rack — push coherent choices to be evaluated not only on bandwidth per port, but on watts per bit and optical layer efficiency.

Regulatory shifts influence network design and supplier selection. New regional electricity pricing regimes and spectrum sharing rules reshape network deployment models and create operating risk that must be priced into procurement and site selection analyses.

Executive frameworks for vendor selection: scorecards that weigh technical fit, integration risk, lifecycle energy cost and roadmap alignment against procurement and support models.

Technology deep dives: comparative analysis of pluggable form factors, DSP roadmaps, coherent engine architectures, coherent package integration trends (including CPO/XPO trajectories), and the implications of moving to 1.6T and multi‑terabit coherent line rates.

Scenario-based demand modeling: near‑term and medium‑term scenarios (conservative, base, aggressive) calibrated to realistic DCI, metro and enterprise adoption curves — enabling CAPEX and inventory planning tied to network rollout windows.

Energy and TCO models: watt-per-bit benchmarking templates and site-level power cost sensitivity analyses that translate optical performance into operating expense impacts across different data center and edge topologies.

Supply chain and manufacturing risk assessment: analysis of critical photonics component constraints, assembly footprint options, and strategies for securing capacity during technology transitions.

Commercial playbook: recommended contracting structures, lead-time hedging tactics, co‑development and strategic partnership approaches tailored to vendor profiles and market concentration dynamics.

The coherent optical module market shows a moderate-to-high level of concentration at the top: the top three suppliers account for a majority share of revenues, with the top five controlling well over two‑thirds of the market. This structure favors suppliers with scale in photonics, DSP IP and system integration, but pockets of opportunity remain for specialized entrants and regional vendors — particularly where cost, power and customization matter.

Coherent Corp. — With integrated photonics capability and a visible push into AI‑scale optics, Coherent’s demonstrations (including 1.6T and experimental 3.2T technologies, along with cross‑technology CPO approaches showcased at OFC 2026) underscore a strategy that blends vertical integration with flagship module roadmaps. For buyers, Coherent represents a supplier likely to lead on performance and integration, making it a natural partner for early adoption among hyperscalers and tier‑1 carriers.

Lumentum — Lumentum’s strength in high‑bandwidth driver‑modulators and component supply positions it as a critical partner for system OEMs and module makers targeting 400G/800G ZR/ZR+ pluggables. Their technology cadence is particularly relevant to buyers seeking optimized component supply chains and validated component-to-module performance.

Fujitsu Optical Components (FOC) — FOC’s commercial deployments of 800G CFP2‑DCO and ZR/ZR+ pluggables for metro DWDM speak to their focus on high‑performance coherent pluggables tuned for operational flexibility. Organizations planning metro upgrades should evaluate Fujitsu for power‑optimized, modulation‑flexible modules.

Marvell Technology — Marvell’s COLORZ family and the announcement of 1.6T pluggables and advanced coherent DSPs signals the commoditization of higher line rates into pluggable formats. For network operators, Marvell is notable for bringing ASIC/DSP integration expertise that shortens time‑to‑market for new pluggable variants.

Acacia (Cisco) — Acacia’s leadership in pluggable coherent optics, across CFP2‑DCO and QSFP‑DD 400G ZR formats, remains a benchmark for interoperability and ecosystem support, particularly for vendors requiring broad multi‑vendor validation and serviceability.

Infinera (Nokia) & Ciena — Both companies bring system-level optics and engine expertise; Infinera with its ICE‑X architectures and Ciena with WaveLogic platforms provide high‑capacity coherent engines ideal for operators consolidating optical layer spend into system and pluggable strategies.

Huawei, Accelink, InnoLight — Regional OEMs and module specialists continue to compete vigorously on cost, production scale and regional support. Their presence keeps pricing and delivery options open for buyers with regional preferences or cost‑sensitive deployments.

Product momentum is unmistakable: major demonstrations and announcements in 2025–2026 across 800G, 1.6T and experimental multi‑terabit coherent solutions compress adoption timelines and raise interoperability and testing requirements for network operators.

Energy and infrastructure disclosures are becoming board‑level items. With significant electricity demand growth tied to AI deployments and high per‑rack power costs, optics selection now materially affects site economics and sustainability targets.

Policy changes, from special electricity pricing regimes to updated spectrum-sharing rules, introduce new externalities that should be scenarioized within procurement and network planning exercises.

Adopt a two‑track sourcing strategy: qualify a performance leader for early access to 1.6T and innovative CPO/XPO offerings, and a cost/performance optimizer for volume supply of established pluggables. This balances innovation access with price resilience.

Incorporate power‑aware procurement clauses: include watts‑per‑bit SLAs, energy benchmarking periods and incentives for power reduction over multi‑year contracts to align supplier incentives with operational efficiency goals.

Stress‑test vendor roadmaps against platform lock‑in risks: require interoperability labs and multi‑vendor validation windows before committing to large rollouts, particularly where new DSP/PHY combinations are involved.

Embed regulatory and site‑level scenarios into rollout plans: model local electricity tariff changes, demand charges and potential spatial constraints to avoid stranded deployments or renegotiation exposure.

Pursue selective co‑development where differentiation matters: for hyperscalers or carriers pursuing unique spectral efficiency or operational automation, co‑developed modules or early partnership agreements can secure roadmap influence and supply priority.

Maintain modular upgrade budgets: plan optical layer investments assuming stepwise upgrades (400G → 800G → 1.6T) and reserve budget for DSP/firmware-enabled performance improvements that do not require full hardware replacement.

Our full Coherent Optical Module Market report delivers the analytical building blocks that senior executives and procurement leaders need to operationalize the above recommendations: validated demand scenarios, supplier scorecards, TCO templates, energy sensitivity models and a risk register tailored to coherent optics transitions. Crucially, we provide executable checklists for vendor qualification and deployment sequencing that can be embedded into procurement cycles in Q1–Q2 2026.

This article is a strategic preview designed to surface the forces shaping coherent optics through 2032 and to outline the decisions you should prioritize in 2026. It intentionally omits granular segmentation tables and specific regional/application share figures — content that our clients rely on for procurement negotiations, capex planning and M&A diligence. For the full dataset, interactive models and supplier matrices referenced here, please consult the complete PW Consulting Coherent Optical Module Market report.

For detailed analysis of this topic, please visit the official page:Coherent Optical Module Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com