Aeroengine Accessory Drive Train (ADT) Market — Strategic Preview for 2026 Decision‑Makers

PW Consulting’s latest market intelligence release, the Aeroengine Accessory Drive Train (ADT) Market Report, delivers a forward‑looking, action‑oriented perspective designed to inform executive decisions throughout 2026. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, the study establishes a clear macro baseline: the ADT market reached approximately USD 1,025.0 Million in 2025 and is modeled to grow at a compound annual growth rate (CAGR) of 6.85% over the 2026–2032 forecast period, with our central scenario projecting market expansion toward roughly USD 1,629 Million by 2032. For senior leaders weighing sourcing strategies, R&D allocation, M&A, or aftermarket monetization, the report converts these macro tendencies into executable steps and measurable KPIs.

Aeroengine Accessory Drive Train Adt Market

Why this report matters for 2026 strategic planning

- Investment timing and sizing: Our forecast and scenario suite help portfolio managers and CFOs align capital deployment with realistic demand trajectories, balancing near‑term supply constraints with mid‑cycle growth.

- Procurement and supply chain resilience: Procurement teams receive prioritized actions to mitigate raw‑material exposure and supplier concentration risks that are already shaping costs and lead times.

- Product and program positioning: OEMs and Tier‑1 suppliers can use the report’s competitive mapping and platform analysis to refine bidding strategies for OEM engine programs and aftermarket service contracts.

- Regulatory and certification planning: Engineering and certification leaders get an operational timetable for FAA/EASA milestones that materially affect time‑to‑market for new ADT designs and material adoption.

What’s inside — practical, operational intelligence (without giving away the core datasets)

PW Consulting’s ADT Report is structured to move teams from insight to action. The publication includes:

Aeroengine Accessory Drive Train Adt Market

- Proprietary market sizing and demand modeling (2020–2032) calibrated to fleet, engine build, and aftermarket economics.

- Scenario and sensitivity analyses — baseline (6.85% CAGR), upside (rapid fleet recovery and defense procurement), and downside (prolonged raw‑material disruption) — with cash‑flow and break‑even implications for program managers.

- Supply‑chain heat maps that identify single‑point failures, critical suppliers, and strategic nodes for dual‑sourcing or nearshoring interventions.

- Technology readiness assessments and certification roadmaps for new alloys, coatings, and gearbox topologies, tied to FAA/EASA approval pathways.

- Commercial playbooks: RFP response templates, aftermarket service contract structures, and pricing levers for spares and repairs.

- Competitive scorecards and M&A screens built to reveal partnership targets and acquisition candidates based on engineering fit, backlog, and margin profiles.

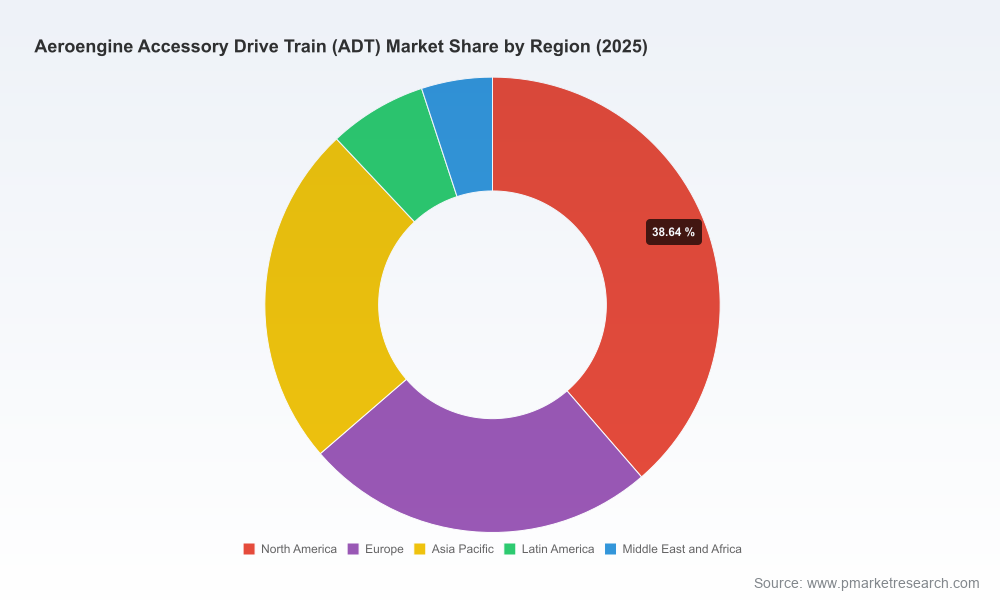

To preserve the competitive value of this research — and in keeping with the “trailer” principle — detailed regional and component splits, as well as granular revenue tables, are intentionally excluded from this preview. Those datasets and interactive models are available in full on the report landing page.

Aeroengine Accessory Drive Train Adt Market

Market dynamics and 2026 inflection points

Three structural dynamics will dominate boardroom discussions in 2026:

- Demand normalization with selective acceleration: Commercial narrowbody replacements and military modernization programs continue to underpin steady ADT unit demand. The market’s projected mid‑single digit CAGR reflects both the steady aftermarket pull and new program deliveries.

- Raw‑material and production cost volatility: Titanium and nickel‑based superalloys remain critical inputs for lightweight, high‑temperature ADT components. Geopolitical concentration of supply and price swings have already pushed procurement teams to revisit long‑term sourcing contracts, explore alternative alloys, and accelerate material substitution research where feasible.

- Certification and technology adoption friction: FAA and EASA regulatory regimes continue to be the gating factor for new materials and novel gearbox architectures. Certification timelines must be built into program schedules from day‑one, and accelerated certification pathways should be pursued where available.

Competitive landscape — what the leading players signal for 2026

The ADT sector shows moderate concentration: the top three suppliers account for a substantial portion of market share while the top five approach a clear majority. That structure favors firms that can combine platform access, manufacturing depth, and aftermarket reach. Key competitive positions to watch include:

- Avio Aero (GE Aerospace) — advantage: platform integration. Avio Aero’s deep engineering alignment with GE engine programs positions it to capture both OEM and early‑life aftermarket revenues. Its capabilities across inlet, transfer and accessory gearboxes make it a natural partner for platform OEMs seeking tight system integration.

- Safran Transmission Systems — advantage: breadth across civil and military markets. Safran’s portfolio and established certification track record reduce adoption risk for customers, especially on high‑demand platforms. Their recent collaborative moves underscore a strategy combining in‑house manufacturing with strategic partnerships.

- BMT Aerospace International — advantage: niche complexity and program responsiveness. BMT’s demonstrated capability to deliver flight‑critical gearboxes (recently evidenced by a full gearbox delivery for a business‑jet engine program) signals an ability to execute on time‑sensitive, high‑complexity programs — a valuable trait for both OEM primes and defense primes.

- Liebherr‑Aerospace — advantage: precision gear and integrated systems expertise. Liebherr is a go‑to supplier for high‑precision transmissions and gear solutions where tolerances and lifecycle performance are paramount.

- Triumph Group & Northstar Aerospace — advantage: manufacturing scale and aftermarket services. These firms combine volume manufacturing with MRO and repair capabilities, offering attractive aftermarket economics to airlines and defense operators.

- The Timken Company — advantage: component specialization. As a leading bearings and components supplier, Timken remains a critical upstream player whose material and design choices ripple across gearbox lifecycle costs and reliability metrics.

Two recent developments crystallize how competition and collaboration will evolve in 2026: BMT Aerospace’s April 2026 delivery of a fully assembled, flight‑critical gearbox demonstrates accelerated program execution capacity among specialist suppliers; and the Safran Aero Boosters / BMT Aerospace partnership (formalized in October 2025) illustrates an emerging model — strategic manufacturing alliances between systems integrators and niche specialists to de‑risk complex defense and civil programs.

Strategic implications and recommendations for 2026

Based on the market baseline and the scenarios modeled, we advise executives to prioritize the following actions in 2026:

- Lock in raw‑material positions: Establish multi‑year supply agreements or strategic off‑take arrangements for titanium and nickel alloys. Explore hedging strategies and material substitution pilots to limit cost exposure.

- Certify early, manufacture later: Begin regulatory engagement for new materials and gearbox designs well ahead of production decisions. Early certification investment reduces program risk and shortens time‑to‑revenue.

- Balance vertical integration with strategic partnerships: Where core IP and aftermarket margins are at stake, consider vertical investments; where speed and flexibility matter, pursue alliances with proven gearbox specialists or precision manufacturers.

- Monetize aftermarket through service models: Design spares pools, long‑term repair agreements, and data‑enabled predictive maintenance offerings to capture higher‑margin recurring revenue as fleet sizes normalize.

- Pursue targeted M&A and capability buys: Use the market’s moderate concentration to acquire specialists that close capability gaps in high‑value gearbox design, testing, or certification.

Operational playbook — first 90‑day actions for 2026

- Run a rapid supplier resiliency audit focused on the top 10 suppliers for critical alloys and precision machining capacity.

- Initiate joint development agreements with at least one gearbox specialist to accelerate certification and share program risk.

- Implement a forward‑pricing strategy for long‑lead raw materials and finalize inventory policies tied to delivery cadence.

- Deploy digital‑twin pilots on one platform to reduce test cycles and create a data foundation for aftermarket services.

Conclusion — where this preview leads you

For 2026, the ADT market represents a blend of stable aftermarket revenue, program‑driven OEM opportunity, and concentrated supplier dynamics that reward both strategic foresight and operational rigor. PW Consulting’s ADT Market Report translates the market’s projected 6.85% CAGR and multi‑year demand trajectory into concrete actions — from procurement hedges and certification timelines to partnership models and M&A playbooks. While this preview outlines the strategic contours and operational priorities, the full report contains the granular regional, component and engine‑type breakdowns, interactive forecast models, and supplier scorecards that procurement, engineering and corporate development teams need to execute with confidence.

Access the complete study and the downloadable executive toolkit on our report landing page to obtain the data tables and scenario models referenced here. PW Consulting stands ready to support bespoke strategy workshops, supplier negotiations, and M&A due diligence to turn these insights into measurable outcomes for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Aeroengine Accessory Drive Train Adt Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com