4‑Ethylnitrobenzene Reagent Market — Strategic Outlook for 2026: A PW Consulting Intelligence Brief

Executive preview

PW Consulting today releases an executive intelligence brief accompanying our upcoming full-market report on the 4‑Ethylnitrobenzene reagent market. This document synthesizes validated market sizing, near‑term dynamics, and critical strategic implications designed to inform executive decisions in 2026. Our base-year analytics use 2025 as the reference point and our modeling projects through 2032, capturing both cyclical commodity swings and structural demand drivers.

4 Ethylnitrobenzene Reagent Market

Market snapshot: trajectory and scale

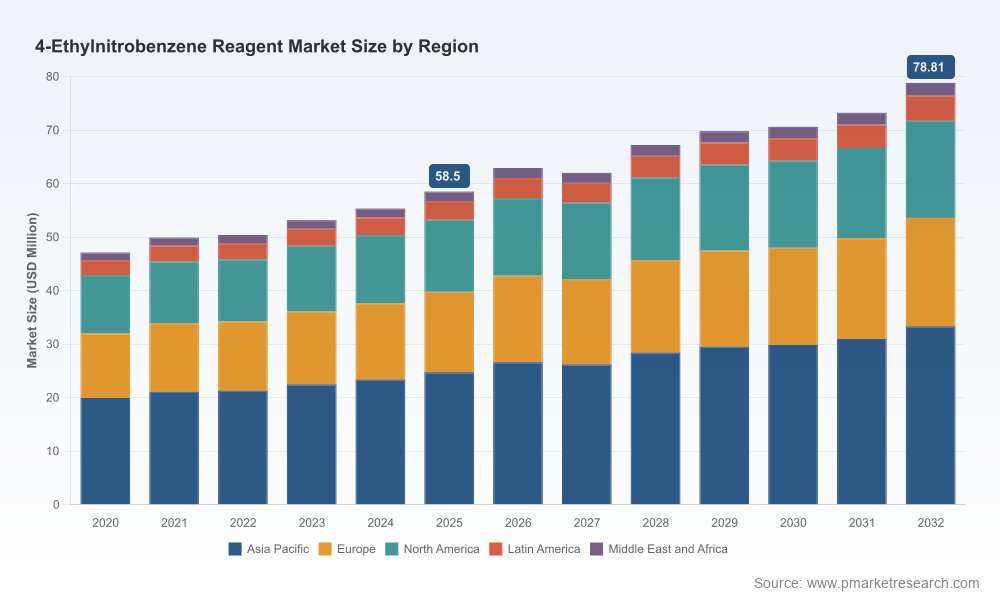

After tracking the reagent market through a five‑year historical window (2020–2025), PW Consulting’s bottom‑up model pegs the global market at USD 58.5 Million in 2025 (base year). Our forecast indicates the market will expand to approximately USD 62.9 Million in 2026 and continue on a steady compounding path to reach roughly USD 78.8 Million by 2032 — reflecting a compound annual growth rate (CAGR) of 4.35% over the 2026–2032 horizon. These macro figures capture the aggregate commercial footprint for research and industrial grades across laboratory, pharmaceutical, agrochemical, and specialty chemical applications.

4 Ethylnitrobenzene Reagent Market

Why this matters for 2026 decision‑making

- Pace of growth is predictable but sensitive to upstream feedstocks. A mid‑single digit CAGR signals a market large enough to justify targeted investments but not one that tolerates inefficient capital deployment. Small shifts in feedstock prices or customer inventory strategies can materially influence margins in the short term.

- Procurement and sourcing are immediate priorities. With raw feedstock (notably nitrobenzene, benzene and nitric acid) driving input cost volatility, purchasing teams must combine shorter tactical buys with longer strategic hedges to protect margin and availability.

- Opportunity windows are regional and application specific. Growth pockets continue to emerge for advanced reagent grades and specialty usage profiles; however, granular opportunity mapping is required to prioritize capex, sales coverage, and regulatory resources.

Operational and commercial implications — granular levers for 2026

Executives preparing 2026 plans should treat this market as a bifurcated contest: companies that optimize supply‑chain resilience and product‑level differentiation will capture outsized returns, while those who rely purely on scale will face margin erosion from feedstock swings.

4 Ethylnitrobenzene Reagent Market

- Supply‑chain risk management: Nitrobenzene price volatility has been uneven across regions — for example, recent Northeast Asia price indications reached approximately USD 1.18/kg in March 2026, while U.S. markets showed weakening in late 2025. Companies should stress‑test sourcing strategies against both regional price spreads and logistical constraints.

- Price‑to‑value commercial models: For buyers of analytical and high‑purity grades, willingness to pay for traceability and documentation is increasing. Suppliers that can certify upstream provenance and deliver consistent analytical specifications command price premia.

- Portfolio prioritization: R&D and mid‑sized manufacturers should evaluate SKU rationalization and focus on reagent grades that align with higher margin downstream applications. Where R&D spend is concentrated, consider channel partnerships that supply research quantities with predictable lead times.

- Regulatory and sustainability readiness: With feedstock chemistry centered on nitration routes, regulatory scrutiny and environmental compliance remain non‑negotiable. Investment in cleaner nitration processes, solvent management, and EHS controls will reduce long‑term exposure and can be a differentiator for tender and contract wins.

What our report delivers — practical analytics and tools

The full PW Consulting report goes beyond narrative to provide practical resources for strategy teams and functional leaders. Highlights include:

- Proprietary market sizing and forward forecasts (2026–2032) by grade and application class, with scenario variants reflecting raw‑material price paths and demand shocks.

- Detailed supply‑chain maps identifying critical upstream feedstocks, synthesis bottlenecks, typical lead times and supplier dependency indices.

- Commercial playbooks for procurement, including tiered sourcing strategies, contractual clauses for price pass‑through and inventory optimization models calibrated to reagent shelf life.

- Supplier scorecards and benchmarking templates that translate qualitative supplier attributes (purity controls, pack sizes, documentation) into decision‑ready metrics.

- Deal‑making and M&A due‑diligence checklists, including integration risk matrices for bolt‑on acquisitions in high‑purity reagent segments.

- Scenario analyses that overlay commodity price scenarios (benzenoid and ethylbenzene feedstock swings) with demand elasticity in pharma, agrochemical synthesis and dye intermediates.

Competitive landscape — who to watch (and why)

The market displays moderate concentration: the top three suppliers account for a meaningful but not dominant share of industry revenues, and the leading five suppliers together approach half the market. This structure creates room for both global volume players and specialized niche providers to coexist.

- Tokyo Chemical Industry (TCI, Tokyo, Japan) — A recognized research reagent supplier with high‑purity catalog offerings and flexible pack sizes, TCI maintains strong brand trust among laboratory and discovery customers.

- Merck KGaA / Sigma‑Aldrich (Darmstadt, Germany) — Global reach and integrated catalog capabilities make this group a default supplier for many discovery and QC labs; their catalog positioning supports early‑stage research demand.

- Thermo Scientific / Acros Organics (Waltham, MA) — Known for high‑specification reagents with guaranteed analytical purity, they are particularly relevant for regulated industries and institutions requiring rigorous documentation.

- Biosynth (Staad, Switzerland) and regional specialty distributors — These players serve R&D and small‑batch pharmaceutical testing customers, often competing on speed, custom packaging and technical support.

- U.S. and India‑based players (multiple). — Several fine chemical distributors and manufacturers provide building blocks and bulk quantities that feed into larger syntheses; their agility in custom synthesis is a recurring advantage.

For companies evaluating supplier strategies or M&A targets in 2026, the choice is rarely between global scale and local service — winning strategies will hybridize global quality assurance with locally optimized logistics and pricing models.

Raw‑material and cost intelligence — the critical context

Understanding the upstream chemistry is essential. 4‑Ethylnitrobenzene is a derivative in a nitration chain where benzene and nitric acid act as the core feedstocks; therefore, cost and availability of those inputs directly influence reagent economics. Ethylbenzene price volatility and regional nitrobenzene market movements have translated into uneven supplier cost bases and shifting margin profiles across geographies. The PW model explicitly incorporates these inputs into forward price scenarios so procurement teams can quantify exposure and design hedge strategies.

Action checklist for executives (2026 planning)

- Embed PW Consulting’s feedstock scenario outputs into 2026 budgeting cycles and stress‑test profitability under adverse price trajectories.

- Segment customers by willingness‑to‑pay and regulatory needs; align sales coverage and product specification investment accordingly.

- Negotiate multi‑tiered supply contracts with optionality for short‑term spot top‑ups to balance cost and availability risk.

- Prioritize investments in EHS upgrades for nitration and solvent handling to reduce compliance exposures and improve bid competitiveness.

- Use supplier scorecards to identify potential bolt‑on targets that can accelerate access to high‑margin niches or fill geographic coverage gaps.

Next steps — where to get the full intelligence

This brief is designed as a strategic trailer: it highlights the research scope, key directional metrics and the types of operational levers that matter in 2026, while reserving detailed splits and tables for the full report. The complete PW Consulting 4‑Ethylnitrobenzene Reagent Market report includes full regional and application breakouts, pricing models, supplier revenue banding and downloadable spreadsheets for internal scenario analysis. Organizations looking to translate the market projections into executable action plans should access the full dataset and modeling workbench to inform procurement mandates, product development roadmaps and M&A diligence.

Closing perspective

For companies engaged in the 4‑Ethylnitrobenzene value chain, 2026 is a year to move from reactive sourcing toward strategic alignment: integrate commodity intelligence into commercial policy, prioritize product differentiation that customers value, and selectively deploy capital where the market’s structural growth and regulatory tailwinds converge. PW Consulting’s full report equips leaders with the granular inputs and decision tools needed to execute those priorities with confidence.

For detailed analysis of this topic, please visit the official page:4 Ethylnitrobenzene Reagent Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com