Avian Influenza Vaccines market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-05-15 09:32:12

PW Consulting’s latest Fan Convectors Market report (base year 2025, forecast 2026–2032) delivers an operationally focused intelligence package designed to guide boardrooms, product teams, and investors as they set strategy for 2026. At a macro level, the global market reached USD 1,376.5 Million in 2025 and — driven by a convergence of energy‑efficiency regulation, the heat pump retrofit cycle, and product innovation — is forecast to grow to USD 2,046.19 Million by 2032 at a compound annual growth rate (CAGR) of 5.85%. This release summarizes the report’s strategic value, highlights market dynamics manufacturers must master, and outlines the practical steps firms should take over the next 12–24 months.

Fan Convectors Market

Market momentum: The steady medium‑term growth trajectory signals that fan convectors are transitioning from niche retrofit components to mainstream elements of low‑temperature HVAC architectures. Firms that align product roadmaps and go‑to‑market plans to this structural shift will capture disproportionate share as adoption accelerates.

Fan Convectors Market

Moderate concentration, strong opportunity: Market concentration metrics indicate a market where three to five established players hold meaningful shares, yet significant room remains for differentiated entrants — especially those with system integrations and retrofit‑focused products.

Fan Convectors Market

Regulatory and technology tailwinds: Tighter energy efficiency standards and the proliferation of heat pumps are driving technical requirements (e.g., reliable operation at lower supply temperatures) that reshuffle competitive advantage toward agile R&D and tested field performance.

Operational leverage for suppliers and installers: The retrofit opportunity favours vendors who can pair product innovation with installation-friendly designs, digital commissioning tools, and service offerings that reduce project friction and warranty risk.

Robust market model: A transparent global model with historical series (2020–2025) and a multi‑scenario forecast (2026–2032). The model supports “what‑if” sensitivity for price, unit mix, and channel penetration and is delivered in an editable spreadsheet so teams can test customized hypotheses.

Competitive playbooks: Deep vendor profiles, product comparisons, and strategic positioning maps that show where incumbent brands win today and where insurgents can create new niches (e.g., ultra‑slim ceiling solutions or heat‑pump‑optimized fan convectors).

Product benchmarking and technical testing guidance: Protocols and scorecards for comparing unit noise, start‑up thresholds, low‑temperature performance, airflow characteristics, and serviceability — enabling procurement teams to move beyond marketing claims.

Commercial tools: Go‑to‑market playbooks, channel compensation models, tender templates, and a retrofit installer kit designed to shorten sales cycles and reduce on‑site variability.

M&A and partnership intelligence: Target archetypes, value creation plans, and integration checklists aimed at acquirers wishing to accelerate capability builds in controls, heat‑pump integration, or localization.

Regulatory tracker and standards implications: A concise digest of evolving energy and product standards affecting product design, testing, and market access across major markets.

Low‑temperature readiness is table stakes. Recent product updates from manufacturers confirm the market’s shift: vendors are re‑engineering activation thresholds and control strategies so fan convectors operate reliably at much lower water temperatures characteristic of heat pumps and optimized hydronic systems. These changes have immediate implications for product architecture, control integration, and test protocols.

Form factor and installation ease drive adoption. Slimline designs and ceiling‑tile compatible models are enabling penetration into retrofit and constrained‑space projects. Products that reduce disruption, simplify mounting, and minimize floor space impact materially shorten specification cycles in commercial and residential refurbishments.

Noise and occupant comfort remain differentiators. Quiet operation combined with fast response is a premium feature for schools, healthcare, and high‑end residential projects — categories where specification authority and reputational risk raise the bar for entrants.

Integration with heat‑pump ecosystems. Strategic partnerships with heat pump OEMs, controls vendors, and commissioning providers will determine which suppliers establish long‑term relevance as systems shift from higher‑temperature boilers to low‑temperature sources.

Service and digitalization extend value. Remote diagnostics, simple commissioning apps, and performance warranties reduce operational risk for specifiers and building owners — converting product sales into revenue streams and differentiation for suppliers.

Established specialists bring domain depth. Companies with deep product families and strong OEM reputations continue to lead on reliability and channel relationships. Their focus on quiet operation and low‑temperature performance keeps them relevant in retrofit and healthcare segments.

European innovators push slim, high‑performance formats. Manufacturers investing in ultra‑slim profiles and low‑temperature designs have an edge in high‑density retrofit markets where space and performance constraints are acute.

Product updates underscore the industry pivot. Recent manufacturer announcements demonstrate a prioritized feature set: reliable activation at lower water temperatures, compact footprints for ceiling and floor installations, and controls capable of tight integration with modern heat‑pump systems. These incremental product moves will influence procurement specifications in 2026.

Mid‑market consolidation probable. Given concentration levels and the need for scale in R&D and service networks, expect continued M&A activity as firms acquire complementary technologies, distribution reach, or service capabilities.

Manufacturers — Prioritize product qualification for low‑temperature systems. Establish a testing and certification roadmap aligned to the performance thresholds buyers now require, and quantify tradeoffs between noise, airflow, and energy use in standardized scorecards.

Product teams — Design for retrofit. Invest in shallow depths, ceiling‑tile compatibility, and modular connection kits that reduce installation time and risk. Deliver clear commissioning protocols and digital setup tools to simplify field onboarding.

Commercial leaders — Re‑tool channel programs. Develop bundled offerings with heat pump suppliers, provide installer incentives for performance‑based contracts, and train sales teams to sell systems rather than components.

Investors and acquirers — Focus on capability gaps. Targets that bring systems integration, controls expertise, or localized service footprints will unlock higher multiples as buyers prioritize end‑to‑end performance and reduced project friction.

Distributors and installers — Build competence centers. Offer standardized commissioning, warranties tied to measured performance, and finance options to lower immediate project cost barriers.

Platform plays: Buyers seeking scale will look to combine complementary portfolios (e.g., slimline specialists + ceiling tile systems + service networks) to gain specification leverage and unit economics improvements.

Service monetization: Aftermarket diagnostics, preventive maintenance contracts, and performance guarantees are high‑margin extensions that increase customer stickiness and smooth revenue streams.

Adjacency expansion: Strategic entrants can accelerate growth by adding controls, heat‑pump interfaces, or retrofit kits — capabilities that shorten sales cycles and increase win rates in tendered projects.

Methodology: The report’s forecasts combine primary interviews with OEMs, distributors, and installers, a bottom‑up assembly of unit economics, and cross‑checked technical evaluations where product performance claims were validated against independent test criteria.

Confidence and scenarios: We provide base, upside, and downside scenarios that stress test adoption timelines for heat pumps, regulatory implementation dates, and price/cost trends. Sensitivity analysis is included in the deliverable model to support bespoke corporate planning.

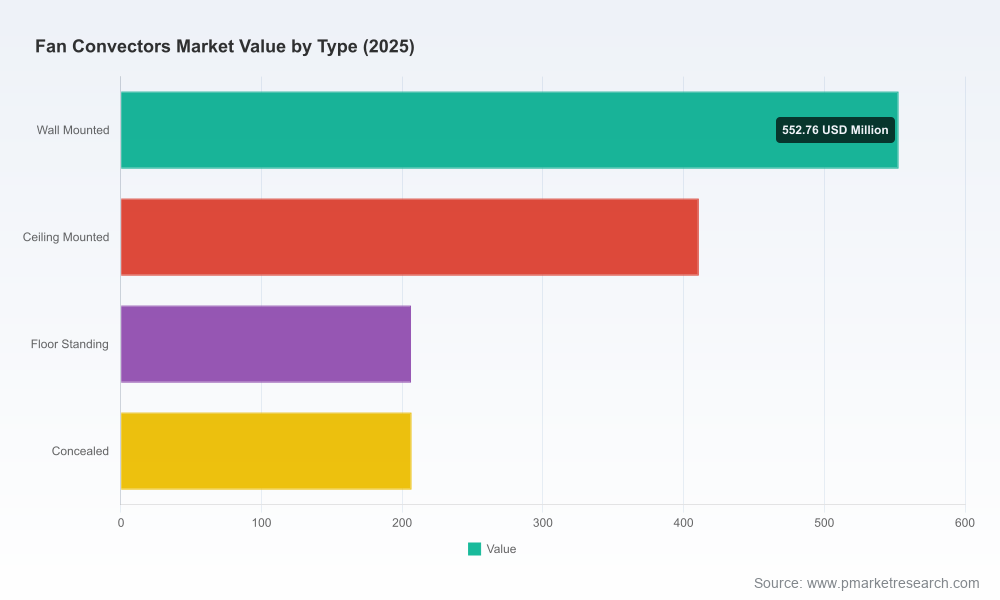

What we withheld: In line with our “trailer” approach, this briefing surfaces high‑value conclusions while deliberately omitting granular segment‑level charts and precise regional/application splits. The full report contains the detailed segmentation, product‑level sizing, and price curves necessary for transactional diligence and bid‑level modeling.

For executives planning budgets, product roadmaps, or M&A activity in 2026, the decision window is now. The market’s projected mid‑term expansion offers room for both incumbents and fast‑moving challengers — but success will flow to organizations that convert product technical competitiveness into installation simplicity, control integration, and reliable field performance. Use 2026 to validate low‑temperature readiness, close partnership gaps with heat‑pump ecosystems, and pilot service propositions that monetize post‑sale performance.

PW Consulting’s full Fan Convectors Market report includes the complete segmentation, regional and application breakdowns, product benchmarking tables, and an editable forecast model. Accessing the full dataset will equip teams to size opportunities at the project level, stress test business cases, and prioritize investments with precision.

For detailed analysis of this topic, please visit the official page:Fan Convectors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com