Kanchi Silver: Supporting Local Artisans with Sustainable Pahadi Jewellery

Other |

2026-06-27 11:16:16

PW Consulting’s latest market research on the Car Blind Spot Surveillance Lens market delivers an actionable, forward-looking intelligence package designed to inform boardroom strategy and operational plans across OEMs, Tier‑1 suppliers, lens manufacturers, and aftermarket specialists. Our proprietary analysis frames market expansion, competitive dynamics, regulatory tailwinds, and input‑cost sensitives that will materially influence capital allocation and product roadmap choices in 2026 and beyond.

Car Blind Spot Surveillance Lens Market

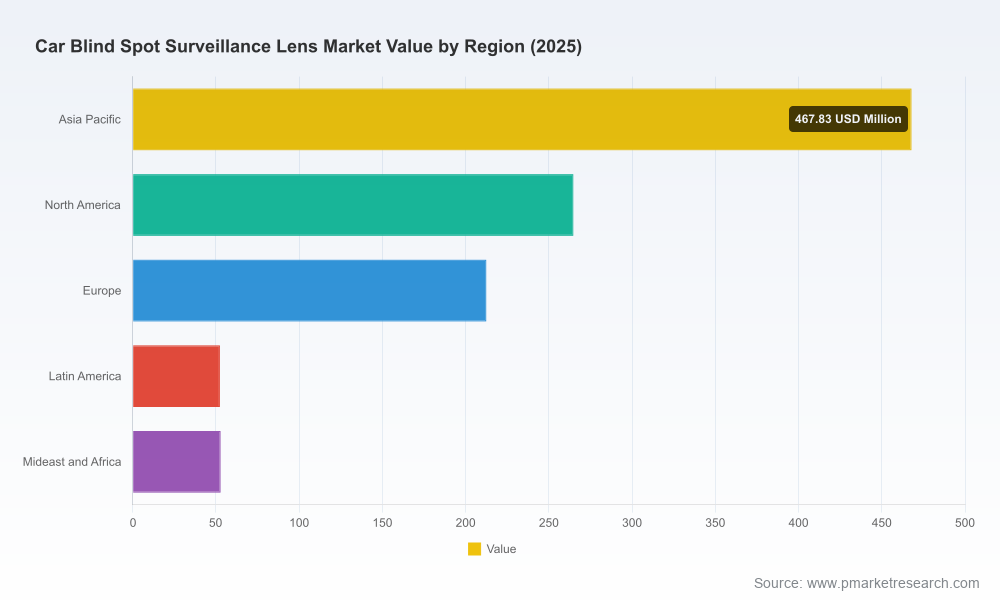

Blind spot surveillance lenses — the optical front‑end components that enable side‑view and multi‑angle camera performance for ADAS and BSIS solutions — are no longer a niche commodity. PW Consulting’s base‑year assessment (2025) places the global market at approximately USD 1.05 billion, and our forecasting model projects sustained growth through 2032 on a compound annual growth rate of 7.85%. The trajectory is driven by regulatory mandates, escalating ADAS content per vehicle, and a shift toward higher resolution and wider field‑of‑view camera modules that demand more sophisticated optics.

Car Blind Spot Surveillance Lens Market

For executive teams planning investments or partnerships this year, the implication is clear: optical capability is a strategic lever. Decisions taken in 2026 about capacity, materials strategy, and channel focus will disproportionately shape competitive positioning for the next generation of ADAS platforms.

Car Blind Spot Surveillance Lens Market

Forward forecasts and scenario analysis: A base forecast extending to 2032, supplemented by sensitivity runs that stress raw material volatility, adoption rates of Level 2+ ADAS, and regulatory acceleration scenarios.

Commercial playbooks: Go‑to‑market templates for lens manufacturers, including Tier‑1 integration strategies, OEM procurement engagement frameworks, and aftermarket commercialization options.

Supply‑chain risk maps: Line‑by‑line assessment of upstream exposure to polycarbonate and glass supply, plus mitigation levers such as dual‑sourcing, long‑term contracts, and strategic inventory buffers.

Technology decision matrices: Practical guidance on when to prioritize glass versus plastic versus hybrid optics based on durability, weight, image performance, thermal budget, and cost trajectory.

Regulatory compliance playbook: Testing, certification, and timeline requirements to meet EU and UNECE mandates relevant to blind spot systems, with checklist templates for product development cycles.

Executive dashboards: Investor‑grade KPIs, margin impact modeling, and a tailored M&A heat map highlighting consolidation targets and capability gaps.

Note: This briefing contains high‑level market sizing and growth metrics intended to guide strategic prioritization. The full report includes granular segmentation tables, regional and application breakdowns, and downloadable financial models reserved for report licensees.

The competitive landscape exhibits characteristics of a maturing but still dynamic market. Market concentration metrics indicate a moderate level of consolidation — the top three players account for a significant share of industry sales, and the top five further increase cluster effects. This creates a dual opportunity: established players can defend margins through scale and OEM relationships, while well‑capitalized challengers with differentiated optics or reliability claims can win design‑wins.

Key strategic observations on participant types and moves:

Large automotive suppliers (system integrators) are integrating optics into broader ADAS solutions. Established names in this cohort leverage global OEM relationships to embed camera‑plus‑lens modules into lane change assist and side monitoring systems. Their strength is systems expertise and certification scale; their challenge is moving quickly enough on optics innovation without incurring heavy legacy cost structures.

High‑volume optical manufacturers, particularly from Asia, are expanding capacity and upgrading production to support higher megapixel counts and stricter quality tolerances required by Level 2+ cameras. These firms are pursuing OEM tender wins and are rapidly qualifying to Tier‑1 supply chains.

Aftermarket and specialist suppliers provide low‑profile and retrofit solutions that remain attractive for commercial vehicle fleets and regions with slower OEM electrification or ADAS penetration. Their agility is a competitive advantage for immediate revenue capture, especially where regulation mandates retrofit compliance.

Regional optics champions from China have scaled rapidly and now combine high‑volume manufacturing with ADAS‑grade design capability. Their investments in higher‑resolution production lines are reshaping cost and lead‑time dynamics for OEM sourcing decisions.

European Tier‑1 system suppliers continue to bundle camera modules with sensor fusion capabilities, offering OEMs a single‑supplier compliance pathway for lane‑change and side‑monitoring systems. This bundling strategy accelerates time‑to‑market but raises the bar for optics suppliers seeking to move beyond pure‑component status.

Aftermarket providers and specialized camera vendors maintain a presence where retrofit demand or niche vehicle segments (e.g., heavy commercial) require tailored blind‑spot solutions that meet evolving standards.

PW Consulting’s full company profiles and scorecards present strengths, weaknesses, and strategic levers for each major participant, including R&D focus, qualification pipeline, and customer concentration metrics.

Two regulatory trends are especially material for investment timing and product specification:

Mandates requiring advanced obstacle detection and blind‑spot information systems in new vehicles create a structural uplift in optical camera content per vehicle and accelerate qualification timetables for suppliers. Companies must align product development cycles with regulation‑linked OEM ordering windows to monetize accelerated adoption.

UNECE standards for monitoring and incident observation in commercial vehicles continue to raise technical thresholds for blind‑spot systems, particularly for pedestrian and vulnerable road user detection. Compliance will require investment in verification testing and field validation.

On the materials side, demand for lightweight optical components is pressuring upstream commodity markets. Lens‑grade polycarbonate is expanding and exhibiting price and availability dynamics that can materially alter BOM cost structures. At the same time, automotive optical plastics have become the predominant choice for many ADAS camera systems due to their impact resistance and weight benefits — a material preference that has consequences for manufacturing methods, certification testing, and recyclability strategies.

Based on our assessment, we recommend executives prioritize five actions this year to capture upside and manage downside risk:

Lock in supplier pathways for both glass and advanced polymer optics to mitigate lead‑time and price volatility; consider hybrid sourcing models that pair tiered suppliers with strategic long‑term contracts.

Invest in qualification pipelines aligned to regulatory rollouts — early certification shortens sales cycles for OEM tenders and raises switching costs for customers.

Differentiate through optical performance and system integration — deliver demonstrable benefits in low‑light, wide‑FOV, and thermal stability to command premium pricing rather than competing on price alone.

Assess M&A and partnership opportunities selectively: target capability gaps (e.g., higher‑MP lens design, coating technologies, or automated inspection) rather than chasing volume alone.

Prepare aftermarket and retrofit channels as complementary revenue streams, particularly for commercial fleets subject to UNECE standards and regions where OEM ADAS penetration lags.

Two concrete developments illustrate the market dynamics at play. First, launches of dual‑camera blind‑spot and incident recording systems underscore demand for integrated solutions that blend optics with recording and analytics. Second, investments in high‑resolution lens production lines reflect a technology shift: optical suppliers are moving to 8MP and higher design and qualification standards to support Level 2+ camera modules. Together, these signals confirm both the near‑term commercial momentum and the technological escalation that will define supplier selection criteria.

For executives preparing budgets, negotiating supplier contracts, or sizing R&D bets in 2026, the question is not whether the blind spot surveillance lens market grows — it is how to position to capture the value created by that growth. PW Consulting’s report supplies the combination of quantitative forecasts, operational playbooks, and competitor intelligence necessary to make that choice with confidence.

We present a rigorous top‑line view (base year 2025 and forecasts to 2032, with clearly stated CAGR assumptions) while intentionally reserving granular segment tables and company scorecards for the full report. That structure is designed to give you immediate strategic orientation while protecting the detailed market modeling that informs procurement negotiations and M&A diligence.

To obtain the comprehensive dataset, segmentation breakdowns, downloadable models, and full company profiles, visit PW Consulting’s report page for Car Blind Spot Surveillance Lenses. Our analysts are available for executive briefings and tailored scenario modeling to support specific portfolio and geographical decisions in 2026.

For detailed analysis of this topic, please visit the official page:Car Blind Spot Surveillance Lens Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com