Smart Card IC Market Outlook 2034: Global Industry Set to Reach US$ 5.2 Billion Amid Rising Demand for Secure Digital Transactions and Smart Identification Solutions

Other |

2026-06-09 08:55:07

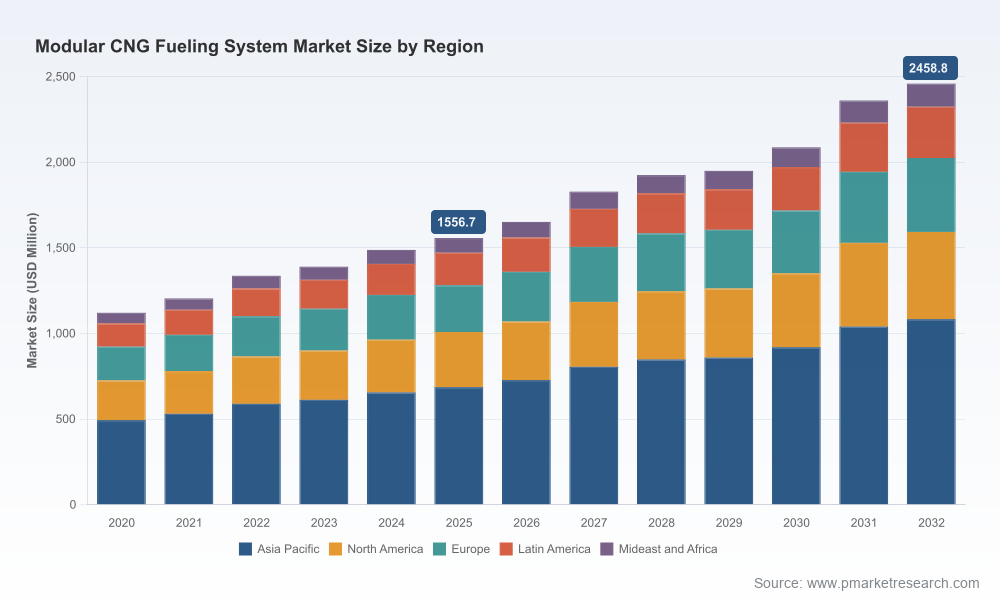

PW Consulting’s latest market study on Modular CNG Fueling Systems arrives at a decisive moment for fleet operators, infrastructure investors, and equipment suppliers. The global market reached approximately USD 1,556.7 Million in 2025 and — under our base assumptions — is forecast to expand at a compound annual growth rate (CAGR) of about 6.75% through 2032, reaching an expected USD 2,458.8 Million. Those headline figures only begin to tell the story: 2026 will be the year in which policy, commodity dynamics, and technology choices converge to make or break project economics for a generation of CNG and RNG projects. This release summarizes the strategic value of our full report for corporate decision-makers preparing budgets, bids, and partnerships in 2026.

Modular Cng Fueling System Market

Policy windows are opening. Proposed U.S. regulations tied to Clean Fuel Production Credits (Section 45Z) materially change the reward calculus for low‑emission fuels. Under draft guidance, credits range from a base level to materially higher values when prevailing wage and other criteria are met — requirements that will alter project structuring and supplier selection for CNG/RNG projects.

Modular Cng Fueling System Market

Carbon value is real and differentiated. Regional credit mechanisms — notably California’s Low Carbon Fuel Standard — assign highly favorable carbon intensity to bio‑CNG, enabling carbon‑negative pathways for fleets when RNG enters the fuel mix. That dynamic creates premium economics for fueling stations configured to accept RNG or biogas.

Modular Cng Fueling System Market

Fuel price and power infrastructure matter. Natural gas spot prices (Henry Hub) and on‑site power options materially affect operating costs and capex tradeoffs. As of March 2026, Henry Hub averaged near USD 3.05/MMBtu; at that price point, compressor efficiency, waste heat recovery, and on‑site generation choices (including microturbines) change total cost of ownership (TCO) outcomes for operators.

Deployments are accelerating and diversifying. Leading network operators and single‑site fleet adopters continue to expand installed base through both proprietary and partner models. Recent orders, station openings, and commissioning activities demonstrate an industry shifting from isolated pilots to scalable, repeatable deployments.

Our objective is to convert market intelligence into executable strategy. The full report is built around tools and deliverables that procurement, strategy, and engineering teams can apply directly in 2026:

Robust market sizing and baseline scenario forecasts (2020–2032) that reflect regulatory and commodity sensitivities.

Investment-level TCO models and sensitivity dashboards, enabling rapid comparison of fast‑fill, time‑fill, mother‑daughter, and virtual‑pipeline approaches under multiple incentive scenarios.

Supplier scorecards and procurement playbooks — technical checklists, compliance matrices, and a scoring framework for turnkey vendors versus specialized component suppliers.

Site selection and roll‑out sequencing frameworks that combine demand clustering, permitting complexity, and incentive capture into a prioritized deployment roadmap.

Risk matrices and mitigation playbooks covering feedstock availability for RNG, interconnection and power resilience, safety and standards compliance, and retrofit pathways for legacy stations.

Commercial contract templates and sample commercial terms for supply, maintenance, and RNG offtake agreements designed to accelerate procurement while protecting project returns.

The market shows moderate concentration: the top three suppliers account for a meaningful share of industry revenue, with the top five capturing more than half the market — a structure that both stabilizes standards adoption and opens room for differentiation through service and integration.

CMD Alternative Energy Solutions — a U.S. specialist in portable, scalable modular systems. Strengths: fleet-oriented products, standards compliance, and real‑time monitoring offerings that reduce commissioning risk for customers.

Galileo Technologies — notable for plug‑and‑play compression modules and biogas compatibility. Strengths: fast installation footprints and solutions tailored to constrained sites.

BAUER Kompressoren — established European technology provider focused on turnkey systems and capital protection. Strengths: engineering depth for high‑duty applications and global service networks.

ANGI Energy Systems (Gilbarco Veeder‑Root group) — offers fully integrated, fleet‑tested turnkey stations with a strong emphasis on operational reliability.

Chart Industries — brings modular fuel‑handling expertise and cryogenic know‑how applicable in hybrid CNG/LNG/RNG deployments.

CORE Fueling — innovator in virtual pipelines that enable on‑site fueling without traditional pipeline ties, opening remote markets and attractive service models.

Other capable providers (regional OEMs, compressor specialists and distributors) are pursuing niches in aftermarket service, fast vs. time‑fill differentiation, and climate‑hardened equipment for extreme environment installations.

For corporate strategists, the implication is clear: scale matters for procurement leverage and standardization, but differentiated service models and RNG‑readiness drive premium returns. Expect continued consolidation and strategic partnerships as OEMs, fleet operators, and energy companies jockey for control of integrated value chains.

Modularization and interoperability: Plug‑and‑play compressor modules and standardized skid configurations compress deployment timelines and reduce engineering risk.

RNG/biogas compatibility: Equipment that accepts variable feedstocks and manages gas quality will be a competitive advantage in markets where LCFS and tax credits boost RNG economics.

Virtual pipelines and delivery models: For dispersed fleets, virtual pipeline models remove the need for traditional interconnection and shift value toward logistics and scheduling platforms.

Digital telematics and remote operations: Real‑time monitoring, predictive maintenance, and integrated card/payment systems reduce downtime and optimize maintenance CAPEX.

Integrated power solutions: On‑site generation choices—including microturbines and waste heat recovery—change lifecycle costs and enable deployments in constrained grid environments.

Prioritize modular, RNG‑ready designs in new procurements to protect upside from carbon credits and emerging fuel incentives.

Accelerate pilot projects that couple fueling sites with RNG supply or virtual pipeline delivery to demonstrate carbon‑negative pathways and to access premium credits.

Lock in supplier service agreements and remote monitoring capabilities to shorten time to revenue and improve uptime, particularly for fast‑fill network nodes.

Structure project bids to capture prevailing wage and domestic content incentives where applicable; the difference in credit realization can be material to project returns.

Assess M&A or partnership opportunities with regional integrators to gain market access and spare‑parts/service density in high‑growth corridors.

Use scenario‑based TCO models to stress‑test projects against gas price moves and incentive expiration timelines — and embed flexibility to pivot between RNG and pipeline gas as market signals change.

Our report is intentionally practical: it pairs market‑level forecasts with procurement templates, vendor scorecards, and live TCO workbooks that clients can adapt to their own cost structures and contracting environments. We refrain from publishing the granular segment tables and proprietary supplier weightings in this summary — those are included in the full subscription product to preserve the integrity of our benchmarking methodology and to protect commercial value for clients.

If you are evaluating greenfield rollouts, network expansions, or acquisitions in 2026, the full report will help you prioritize capital under real‑world regulatory permutations, quantify the impact of evolving tax credit regimes and carbon credit markets, and accelerate procurement without sacrificing technical rigor.

PW Consulting’s full Modular CNG Fueling System Market report contains the granular datasets, supplier benchmarking dashboards, and downloadable modeling templates referenced above. For decision teams preparing 2026 budgets, the report translates market intelligence into executable decisions: which sites to greenlight, which vendors to shortlist, how to structure contracts to capture credits, and where to invest in service capabilities.

To access the complete analysis and data packages, including our proprietary TCO model and vendor scorecards, visit the PW Consulting report page or contact our subscriptions desk. Our analysts are available to run tailored scenario workshops to align your 2026 investment plan with the rapidly evolving regulatory and commercial landscape.

For detailed analysis of this topic, please visit the official page:Modular Cng Fueling System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com