Rosin Resin Market Outlook 2026: Strategic Imperatives for Industry Leaders

PW Consulting’s latest market study on the Rosin Resin industry provides an actionable roadmap for executives preparing for 2026 and beyond. Drawing on a detailed historical review (2020–2025) and a forward-looking forecast (2026–2032), the report synthesizes market fundamentals, supply-chain dynamics, competitive moves, and regulatory trends to translate raw data into strategic options. Our base-year calibration (2025) anchors a market-size view that continues to expand under steady demand, underpinned by a forecast compound annual growth rate (CAGR) of 4.42% across the 2026–2032 horizon.

Rosin Resin Market

Market snapshot: stability with room for premiumization

After recalibrating the 2020–2025 trajectory, PW Consulting’s model sets the 2025 industry revenue benchmark at USD 2,637.2 Million (base year 2025). Our granular scenario mapping points to a market that resumes growth in 2026 and progresses toward a mid-single-digit CAGR through 2032, culminating in a market approaching USD 3.57 Billion by the end of the forecast period. This path reflects a balance of mature downstream demand (adhesives, inks, rubber compounding, coatings) and pockets of premiumization driven by bio-based, low-VOC formulations.

Rosin Resin Market

Why this report matters for 2026 decision-making

- Translate macro growth into tactical choices: The report converts topline expansion into quantified demand corridors by product family and end-use pathway, enabling capex prioritization and supply-commitment sizing for 2026 planning cycles.

- Anticipate margin pressure and sourcing risk: We map raw-material volatility and tariff exposures onto gross-margin scenarios so procurement and finance leaders can stress-test contracts and hedging strategies ahead of budget approvals.

- Prioritize R&D and portfolio moves: Our assessment identifies where technological differentiation (e.g., hydrogenated rosin, rosin esters, bio-based derivatives) will unlock premium pricing and new customer specifications.

- Inform M&A and alliance strategies: By combining market concentration measures with company positioning, the report surfaces the most attractive targets and partnership archetypes for bolt-on acquisition or JV activity in 2026.

Market dynamics: what’s driving direction in 2026

- Sustainability as a demand lever: Rosin resins continue to benefit from the broader shift toward bio-based and low-VOC chemistries, especially in regions enforcing stringent emissions standards. This creates a two-track market: bulk commodity demand on one hand and differentiated, higher-margin eco-formulations on the other.

- Upstream supply volatility: Pine-resin tapping patterns and harvesting policies in key producing geographies have created episodic swings in feedstock availability and price, which reverberate through procurement decisions and inventory strategies.

- Regulatory and trade context: Recent trade policy adjustments and reciprocal tariff implementations have introduced new sourcing complexities for multinational users of rosin resins. Firms with nimble logistics and diversified supplier networks can turn this into a competitive advantage.

- Application-side resilience: Adhesives and printing inks remain major, stable demand pools, while coatings and specialty rubber compounding present cyclical but strategic opportunities for formulation-driven growth.

Segmentation and channels: where to focus without drowning in data

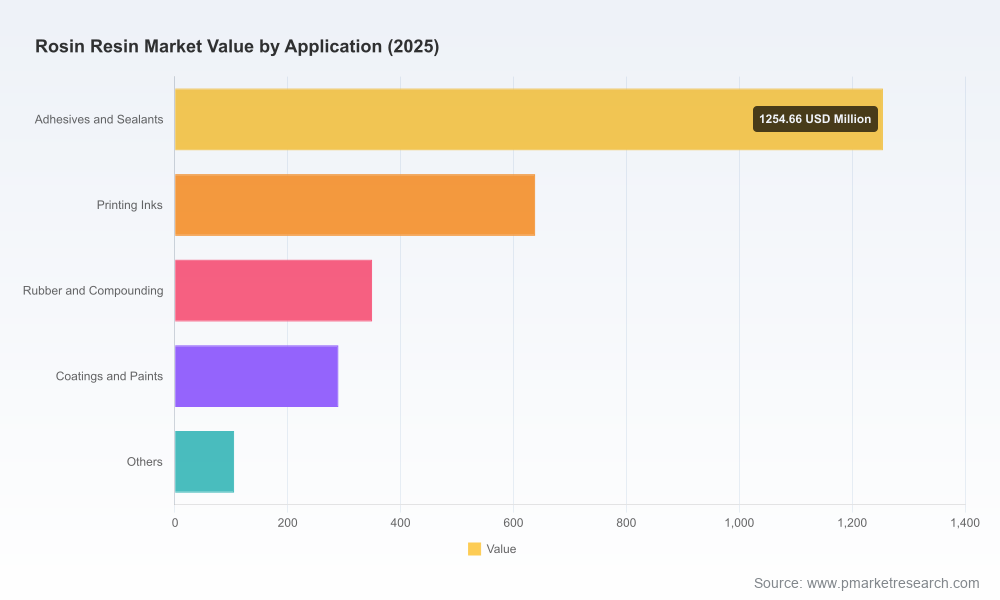

PW Consulting’s report preserves the commercial confidentiality of our proprietary splits while delivering the actionable intelligence buyers and sellers need. We segment the market by type (gum rosin, tall-oil based variants, wood-derived rosin) and by end-use (adhesives & sealants; printing inks; rubber & compounding; coatings & paints; and other specialty uses). Each segment analysis links demand drivers to margin profiles, formulatory constraints, and specification trends so product managers can size R&D bets and GTM moves. For readers seeking the detailed numerical breakdowns, the full dataset and model are available in the report portal.

Rosin Resin Market

Regional contours to watch in 2026

- Demand geography remains uneven: Some regions show robust industrial demand and formulation upgrade cycles, while others exhibit more price-sensitive, volume-driven purchasing behavior. This bifurcation influences route-to-market choices and inventory strategies.

- Supply-side concentration impacts: The locus of raw pine-resin production continues to shape logistics and hedging priorities; intermittent reductions in tapping activity in certain provinces have previously caused short-term disruptions that ripple through global trade lanes.

- Trade policy noise: New reciprocal tariffs and selective exemptions introduced in recent policy cycles add complexity to sourcing decisions—cross-functional teams should incorporate tariff scenarios into supplier evaluations for 2026 contracts.

Competitive landscape: strategic positioning of core players

The rosin resin industry is best described as moderately fragmented: the top three suppliers account for less than one-third of the market, and the leading five capture well under 40%. This structure supports differentiated plays—scale players exploit integrated upstream feedstock advantages, while specialized producers compete on formulation expertise and customer intimacy.

- Eastman Chemical Company (Kingsport, Tennessee, USA): A technology-driven incumbent with a broadened portfolio of rosin esters and hydrogenated derivatives. Recent product introductions underscore Eastman’s push into heat-activated and sanitary-packaging adhesive niches.

- Harima Chemicals Group (Japan): Deep vertical integration in pine chemicals and a strategic emphasis on eco-friendly rosin products position Harima as a go-to supplier for clients pursuing low-VOC formulations.

- Arakawa Chemical Industries (Japan): Focuses on tackifier and specialty applications—its R&D cadence strengthens value propositions for formulators requiring tailored resin properties.

- Kraton Corporation (Houston, USA): Turning tall-oil derivatives and bio-based innovations into competitive offerings for adhesives, sealants, and rubber compounding customers.

- DRT (Dax, France) and other European specialists: Strong in rosin derivatives for adhesives, coatings, and fragrance platforms; European suppliers are well-placed to serve stringent regulatory regimes with compliant chemistries.

- Regional producers across China, Southeast Asia, South America, and Europe: These firms collectively supply bulk gum rosin and derivative streams and are critical to short-cycle demand fulfilment and feedstock arbitrage plays.

Noteworthy recent moves—such as the 2025 launches of bio-based rosin resins and new rosin esters for heat-activated adhesives—signal a clear industry pivot: product innovation is the primary mechanism for margin capture in an otherwise commodity-anchored chain.

Strategic playbook for 2026

- Prioritize dual sourcing with conditional allocations: Given upstream volatility, procurement should lock baseline volumes with spot-flex capacity for upside, supported by pricing collars and indexed contracts.

- Invest selectively in formulation IP: R&D investments that deliver low-VOC, bio-based or heat-activated solutions are most likely to compound returns, especially in regulated markets.

- Optimize pricing through product-tiering: Create a tiered portfolio—commodity-grade resins for price-sensitive channels and premium differentiated products for high-growth specification segments.

- Mitigate trade risk via footprint strategy: Manufacturers and distributors should stress-test supply chains under tariff and logistics scenarios; regional stocking hubs and contractual flex can buffer shocks.

- Assess consolidation opportunistically: With a fragmented market structure, bolt-on acquisitions for geographic reach or specialty capabilities remain attractive—our M&A chapter provides prioritized target criteria and valuation heuristics.

What PW Consulting’s full report delivers

Beyond the strategic overview above, the full Rosin Resin Market Report contains:

- Proprietary demand models with scenario-sensitive forecasts for 2026–2032 calibrated to our 2025 base year;

- Actionable procurement playbooks and contract templates tailored to raw-material cost volatility and tariff scenarios;

- Detailed segmentation matrices with margin and growth profiles for product types and end-use sectors (note: detailed splits and company-level sales data are available in the paid report);

- Competitor profiles with capability maps, recent development timelines, and prioritized partnership/acquisition targets;

- Implementation roadmaps for R&D, manufacturing footprint adjustments, and commercial commercialization aimed at capturing premiumization opportunities.

Final takeaways for leaders planning 2026

Rosin resins will remain a foundational industrial resin class through the late 2020s, offering predictable baseline demand alongside pockets for margin expansion via product innovation and sustainability positioning. For 2026 planning, the imperative is twofold: de-risk the supply chain against upstream volatility and invest where formulation differentiation meets regulatory tailwinds. Executives who align procurement, R&D, and commercial strategies around these dynamics will convert a modest market growth profile into outsized returns.

For a comprehensive set of model outputs, competitive scorecards, and the operational playbooks referenced here, access the full PW Consulting Rosin Resin Market Report via our report portal. The full dataset and proprietary segment-level forecasts are available to subscribers and strategic clients.

For detailed analysis of this topic, please visit the official page:Rosin Resin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com