Identifying Key Position Proximity Sensor Market Trends and the Rise of Smart Sensing Solutions in Industry 4.0

Other |

2026-05-07 09:16:53

As enterprises prepare capital allocation, architecture refreshes, and strategic vendor partnerships for 2026, PW Consulting’s latest Network Interface Controller (NIC) Market report delivers a concise, actionable intelligence package. Our analysis synthesizes historical performance, near-term catalysts, and seven-year forecasts to equip CIOs, procurement leads, and infrastructure architects with the insights required to make high-confidence decisions in an era of accelerated network acceleration and software-defined infrastructure.

Network Interface Controller Nic Market

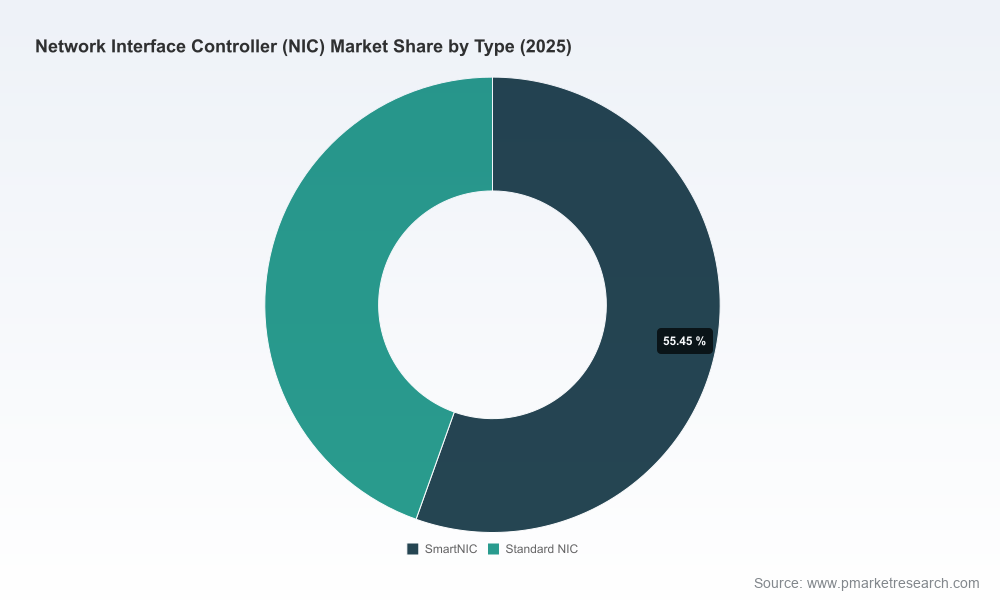

The NIC market is on a rapid growth trajectory. After accelerating through the early 2020s, the market reached approximately USD 6.8 billion in 2025 and, under a set of realistic adoption scenarios, is forecast to expand at a compound annual growth rate (CAGR) of roughly 16.5% over 2026–2032, reaching a near-term multibillion-dollar scale by the end of the decade. Market concentration is meaningful: the top three vendors account for the majority share, and the top five vendors control around three quarters of the market — a structure that shapes pricing dynamics, standards influence, and channel power.

Network Interface Controller Nic Market

For enterprise decision-makers, these macro signals imply three immediate imperatives: (1) align procurement cycles to benefit from rapid product-cycle innovation, (2) design for interoperability and workload portability to avoid lock-in with dominant suppliers, and (3) incorporate energy and infrastructure cost volatility into total cost of ownership (TCO) models.

Network Interface Controller Nic Market

Rapid growth driven by AI and hyperscale networking: Adoption of programmable NICs, DPUs/SmartNICs, and higher-speed Ethernet ports is being propelled by AI workloads, disaggregated infrastructure, and cloud-native designs. These trends drive disproportionate demand for high-performance, offload-capable NICs that reduce host CPU burden and enable software-defined packet processing.

Consolidation and strategic differentiation: With the market exhibiting a high degree of concentration, scale gives incumbents the advantage in silicon roadmaps, software ecosystems, and channel reach. New entrants and niche suppliers still find opportunities in specialized segments — ruggedized, embedded, telco, and cost-optimized consumer NICs — but must partner or specialize to move beyond limited share positions.

CapEx vs. OpEx trade-offs sharpen: Infrastructure costs – particularly energy consumption and data center power provisioning – are significant drivers of lifecycle economics. Electricity expenses and utility tariff structures materially affect NIC strategy where offload efficiency and power-per-Gbps matter to TCO.

Our report maps the ecosystem across region, NIC type (from commodity controllers to SmartNICs and DPUs), and transmission-rate tiers (spanning 10GbE up to 400GbE+). Rather than reproducing sensitive granularity in this release, we highlight directional trends: SmartNIC/DPU adoption accelerates in cloud, telco, and AI-centric environments; ultra-high-speed transmission tiers are becoming table stakes for hyperscale operators; and regional adoption patterns continue to reflect differing investment cycles and regulatory drivers.

The NIC vendor landscape blends major semiconductor incumbents, networking OEMs, and specialized niche players. Our competitor analysis in the report evaluates product roadmaps, software stacks, ecosystem integrations, and go-to-market models. Key observations:

Intel Corporation — Continuing its emphasis on programmable Ethernet controllers and high-speed connectivity, Intel’s strategy targets both data center and edge automation use cases. Recent platform launches position the company to defend server OEM relationships while moving further into deterministic networking for industrial and telecom edge deployments.

Broadcom Inc. — Broadcom is leveraging its deep silicon and developer-offload capabilities to target cloud-native hypervisors and AI clusters. Its NIC portfolio emphasizes offload functionality and high-throughput optics compatibility, appealing to operators prioritizing performance density.

NVIDIA Corporation — With its DPU/SmartNIC roadmap, NVIDIA has positioned itself at the nexus of AI acceleration and network offload. The company’s approach tightly couples NIC hardware with software-defined security and telemetry, attractive to hyperscalers and AI-dominant data centers.

Marvell Technology Group — Marvell’s focus on DPUs and CXL-friendly designs addresses emerging needs for memory coherency and disaggregated compute. Its platform-level integrations appeal to cloud providers and telco operators planning for CXL-enabled futures.

Cisco, Juniper, Fujitsu — Networking incumbents continue to bundle NICs into broader switching and SDN portfolios, reducing integration friction for enterprise customers that prefer end-to-end solutions.

Realtek, TP-Link, NETGEAR — These players preserve strong positions in consumer, SMB, and cost-sensitive segments, where price-performance and form-factor diversity determine buying behavior.

Specialized vendors (Chelsio, Silicom, Abaco, Lantronix, LR-LINK) — These firms offer purpose-built solutions for storage offload, security, telecom and defense markets; their technical differentiation is often tied to protocol offloads, ruggedization, or regulatory certifications.

New platform launches from silicon leaders are accelerating the deployment of 400 Gbps-capable NICs and DPUs, with production ramps expected across 2026. These platforms emphasize PCIe Gen 5/6 compatibility, hardware offload for virtualization and RDMA, and expanded cryptographic features to support secure, high-throughput AI fabrics.

Hyperscale commitments to fiber and interconnect expansion — highlighted by multi-year supplier agreements — are reducing lead-time risks for high-speed optics while reshaping supply-chain footprints.

Regulatory moves to streamline technology transitions (for example, policy changes reducing certain local barriers) are smoothing network modernization paths in several jurisdictions, lowering administrative friction for upgrades.

Energy and infrastructure costs: Rising electricity prices and utility tariff reforms create variability in data center Opex. Since power consumption represents a substantial share of operating budgets, the energy efficiency of NICs — particularly at scale — must be integrated into procurement evaluations.

Capital intensity of data center buildouts: Broad investments in fiber and power infrastructure over the coming years increase the opportunity costs of equipment choices. Enterprises must weigh near-term performance gains against longer-term compatibility with evolving facility footprints.

Supply-chain and strategic sourcing: Large-scale fiber and cable deals by hyperscalers signal both opportunities and competition for capacity. Vendors that secure upstream partnerships can offer more predictable lead times — a competitive advantage for buyers seeking continuity.

Standards and interoperability: As DPU and SmartNIC capabilities deepen, the enforcement of open standards and well-documented APIs will be critical to avoid software lock-in and preserve workload mobility across vendors.

Proprietary market model covering historical performance and a 2026–2032 forecast horizon, built from bottom-up unit shipments, ASP trends, and software-enabled pricing dynamics.

Vendor scorecards evaluating technology maturity, ecosystem depth, partner integrations, and supply-chain resilience to support vendor selection and negotiation strategies.

Use-case driven TCO models and scenario planners for co-locating AI workloads, telco edge deployments, and enterprise virtualization environments.

Procurement playbooks, risk checklists, and migration templates that help infrastructure, network, and procurement teams operationalize strategic choices within 90–180 day planning cycles.

Executive decision matrices and board-ready briefing decks designed to bridge technical findings to investment and capital planning discussions.

Short-term (90–180 days): Freeze long lead-time purchases only where vendor roadmaps create immediate value; otherwise, prioritize modularity and contractual flexibility. Leverage TCO calculators to translate power and density metrics into annualized cost impacts.

Medium-term (6–18 months): Pilot SmartNIC/DPU integrations on critical AI or storage workloads to understand operational impacts and mitigation needs. Use vendor scorecards to qualify partners for scale deployments.

Long-term (18+ months): Design procurement windows aligned with predicted silicon ramps and facility upgrades. Establish interoperability requirements and contractual escape clauses that protect against rapid market consolidation and software lock-in.

PW Consulting’s NIC Market report is crafted for leaders who must reconcile rapid technological evolution with constrained budgets and increasing operational complexity. With an expected market expansion at a ~16.5% CAGR through 2032 and pronounced vendor concentration, the 2026 planning cycle is a pivotal moment to shift from reactive upgrades to proactive architecture and sourcing strategies. Our analysis points to clear actionables: prioritize energy-aware procurement, invest in interoperability, validate DPU/SmartNIC value through targeted pilots, and renegotiate supplier terms with an eye toward long-term roadmap alignment.

This release previews the report’s strategic insights but intentionally omits the detailed segment-level breakdowns, regional shares, and granular price and volume tables that are included in the full publication. To obtain the complete dataset, scenario models, and vendor-specific metrics necessary for board-level decisioning and tactical procurement execution, please visit the PW Consulting report page or contact our research team for licensing and briefing options.

For detailed analysis of this topic, please visit the official page:Network Interface Controller Nic Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com