Collector Auto Insurance Market 2026: Strategic Imperatives from PW Consulting’s New Report

Executive summary

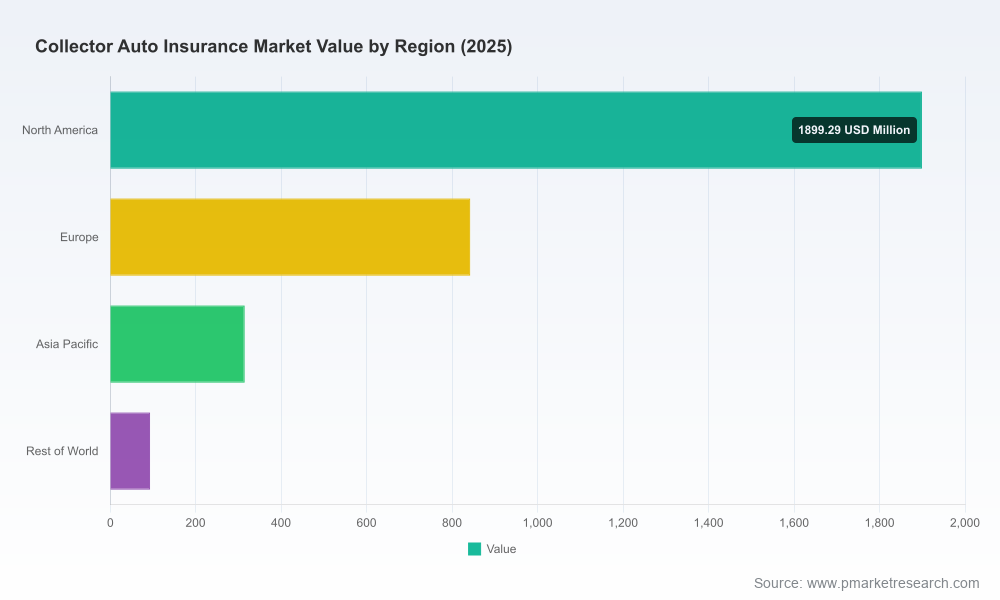

PW Consulting’s latest market study on Collector Auto Insurance—anchored on a 2025 base year and covering historical performance from 2020–2025 with a forecast through 2026–2032—delivers a pragmatic, decision-ready view for insurers, brokers, platform partners, and investors planning for 2026. The specialist market has demonstrated resilient expansion through the pandemic recovery and into 2025; our analysis places the market at approximately USD 3.15 billion (Million, base year 2025) and projects a compound annual growth rate (CAGR) of 6.5% through 2032, taking the market toward the USD 4.9 billion range by the end of the forecast horizon.

Collector Auto Insurance Market

This release outlines why that trajectory matters for capital allocation, distribution strategy, underwriting economics, and product design in 2026—while intentionally withholding the granular cell-level tables and proprietary segment models contained in the full report to encourage direct engagement with PW Consulting’s research platform.

Collector Auto Insurance Market

Why 2026 is a strategic inflection point

- Mature but under-penetrated specialty risk: Collector auto insurance occupies a niche where hobbyist demand, asset appreciation dynamics, and unique usage profiles create differentiated underwriting and pricing opportunities that larger personal lines carriers may overlook.

- Distribution reconfiguration: Strategic alliances between specialty underwriters and mainstream insurers or digital marketplaces (including recent announced partnerships) are reshaping reach and cost-to-serve—making 2026 the year to lock in distribution partnerships or build defensive integration capabilities.

- Data + privacy constraints: The accelerating policy adoption of telematics-like products for classic and custom vehicles confronts a rapidly evolving privacy and regulatory environment. Firms that align their data strategies with both product innovation and compliance will secure competitive advantage—and avoid material enforcement risks.

Market trajectory and macro sizing (what the numbers imply)

From a quantitative perspective, the collector auto insurance market growth path from roughly USD 2.45 billion in 2020 to USD 3.15 billion in 2025 reflects steady demand growth plus premium expansion driven by higher declared values and digital distribution efficiencies. With an anticipated 6.5% CAGR for 2026–2032, the market will support enhanced scale economics for mid-sized specialists while remaining sufficiently fragmented to allow new entrants and InsurTech-enabled adjacencies.

Collector Auto Insurance Market

Key implications of this trajectory:

- Capital deployment for underwriting capacity and reinsurance should be calibrated to a market that is expanding at mid-single digits annually—large enough to support bolt-on M&A yet modest enough that pricing discipline remains critical.

- Technology investments (policy administration, claims triage for high-value assets, and customer experience platforms) will increasingly be the differentiator that converts collector enthusiasts into long-term policyholders.

- Product innovation targeted at low-frequency/high-severity exposures (agreed value, transit coverages, new acquisition protection) will drive retention and margin uplift for carriers that execute well.

Report contents: practical tools and deliverables

PW Consulting’s Collector Auto Insurance Market report is designed as an operational playbook, not just a snapshot. It contains:

- Macro and micro market models (historical 2020–2025 and forecast 2026–2032) with sensitivity testing and scenario-based stress cases.

- Underwriting scorecard templates and loss-ratio benchmarks calibrated to collector use patterns and asset classes.

- Distribution economics playbooks comparing direct, agency, affinity and platform partnerships—with actionable metrics for customer acquisition cost, lifetime value, and break-even premium.

- Claims handling protocols and cost-containment strategies for high-value repairs, restoration valuation disputes, and parts sourcing.

- A 12–18 month go-to-market roadmap for specialty insurers and incumbent carriers considering a collector-auto vertical build vs partnership approach.

- M&A screening matrix and target profiles based on capability gaps in underwriting, distribution and digital servicing.

Each deliverable includes worksheets and templated presentations that teams can adapt for board papers, investor diligence, or new product launch plans. The full granular datasets and proprietary segment matrices are reserved for subscribers and report purchasers to preserve the competitive insight contained therein.

Competitive landscape: who matters and why

The market remains moderately concentrated: the top three firms account for roughly 42.5% of industry premiums, while the top five reach approximately 58.7%. That structure produces both stability and openings—specialists retain pricing power with core hobbyist audiences, while partnerships with mainstream carriers expand footprint.

- Hagerty (Traverse City, Michigan) — the clear bellwether among specialists, Hagerty combines an enthusiast-centric brand, agreed-value product expertise, and increasingly broad distribution reach following strategic alliances with larger carriers. Recent public results show robust premium acceleration in early 2026, underscoring the payoff from its community- and content-driven acquisition strategy.

- American Collectors Insurance (West Chester, Pennsylvania) — a long-tenured specialist with strong customer-service metrics and affinity relationships. Its established brand and broker relationships make it a frequent partner or acquisition target for insurers seeking instant access to specialty portfolios.

- Grundy Insurance (Horsham, Pennsylvania) — known for broad eligibility and flexible mileage offerings, Grundy’s 2026 preferred-provider announcement with a major collector marketplace exemplifies the distribution-first playbook gaining traction across the sector.

- American Modern Insurance Group, Heacock Classic, J.C. Taylor — regional and national specialists that maintain loyalty through deep product knowledge, strong claims handling, and lifestyle positioning toward collector communities.

- Chubb and Safeco (Liberty Mutual) — incumbent high-net-worth and mainstream carriers that have expanded collector coverage via partnerships or in-house specialty teams. Their involvement raises industry benchmarks for underwriting sophistication and claims indemnity limits.

Competitive dynamics to watch in 2026:

- Alliance velocity—partnerships between specialists and national carriers or marketplaces are accelerating distribution reach while preserving underwriter margins.

- Brand as a moat—community engagement, events, editorial content and valuation services increasingly act as customer-acquisition engines that pure price competition cannot easily replicate.

- Scale vs. specialization trade-offs—larger carriers bring capital and distribution, specialists bring underwriting expertise; winners will effectively combine both through JV-like arrangements or capability-focused M&A.

Regulatory and data privacy dynamics

Data strategy is now a board-level concern for collector-auto players. Recent regulatory developments are reframing the permissible use of vehicle- and driver-linked data:

- California’s privacy regime (effective January 1, 2026 changes) now captures certain marketing and analytics processing outside traditional insurance-specific exemptions—impacting third-party data vendors and any direct-to-consumer analytics initiatives.

- Oregon’s 2025 update explicitly extends controls to motor-vehicle manufacturers and affiliates handling vehicle-use data—adding compliance obligations for dealers, telemetry partners and OEM-integrated offerings.

- Enforcement attention in Texas in 2025 targeted insurers and analytics firms for telematics data handling practices—illustrating that usage-based approaches carry state-specific legal risk.

Implications for business leaders:

- Embed privacy-by-design in telematics pilots and valuation analytics; avoid ad-hoc data collection that triggers notice-and-consent or sale restrictions.

- Negotiate clear data ownership and processing clauses with marketplace partners and vendors to preserve monetization optionality while meeting regulatory obligations.

- Prioritize auditability—regulators expect demonstrable controls around data minimization, retention and subject access processes.

2026 playbook: five actions for market leaders and fast followers

- Lock in distribution partnerships now: Secure preferred provider arrangements or API-level integrations with vehicle marketplaces and enthusiast platforms to capture inbound demand with low acquisition cost.

- Operationalize agreed-value economics: Standardize valuation processes, salvage resale channels, and restoration-provider networks to reduce claims leakage and improve loss-adjustment timelines.

- Invest selectively in digital servicing: Prioritize policy lifecycle features that matter to collectors—digital valuation updates, auction monitoring alerts, and streamlined claims for restorations—over broad consumer mobility features.

- Govern data rigorously: Create cross-functional privacy and product committees to vet telematics pilots, ensure compliance with state-level privacy laws, and define acceptable uses that preserve customer trust.

- Assess M&A defensively and offensively: Use the PW Consulting M&A screening toolkit in the full report to identify bolt-on targets that bring distribution, valuation IP, or claims-servicing capabilities.

Concluding perspective and where to find the full intelligence

Collector auto insurance in 2026 sits at the intersection of hobbyist passion and sophisticated risk management. The market’s mid-single-digit CAGR and observed concentration ratios create an environment in which focused specialists and agile incumbents can both thrive—provided they move decisively on distribution, underwriting process modernization, and data governance.

PW Consulting’s full Collector Auto Insurance Market report delivers the granular models, scenario analyses, underwriting scorecards, and commercial templates necessary to translate strategy into execution. To access the complete dataset, proprietary segment matrices, and customizable playbooks referenced in this release, please visit PW Consulting’s insights portal or contact our industry practice leads for a briefing.

For detailed analysis of this topic, please visit the official page:Collector Auto Insurance Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com