US Portable Respiratory Monitor Market Size and Demand Forecast 2026–2034

Health |

2026-06-17 11:00:44

As companies across industrial sectors recalibrate capital and operational priorities for 2026, understanding the trajectory of commercial and industrial reverse osmosis (RO) markets is mission-critical. PW Consulting’s latest market research — a data-driven, practitioner-focused analysis covering 2020–2025 historicals and a 2026–2032 forecast horizon — equips executives with the strategic context needed to make high-confidence decisions. This preview outlines the headline macro trajectory, the structural forces that will shape supplier and buyer strategy in 2026, and the analytical tools contained in the full report (available on our site) that translate insight into action.

Commercial And Industrial Ro Water Treatment Equipment Market

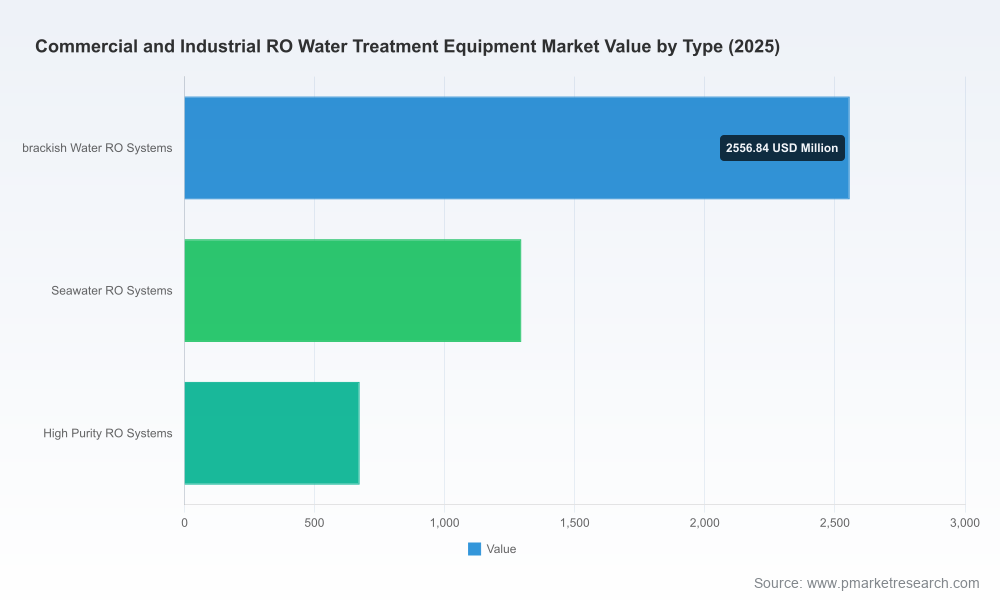

Key macro indicators underline a sustained growth phase for the commercial and industrial RO equipment market. After consistent expansion through the historical window, global market revenue reached approximately USD 4.53 billion in 2025 and is projected to rise to about USD 5.12 billion in 2026. PW Consulting’s forecast applies a compound annual growth rate (CAGR) of 7.85% across the 2026–2032 period, which projects steady near- to mid-term expansion and culminates in a multimillion-dollar market value by 2032.

Commercial And Industrial Ro Water Treatment Equipment Market

Two implications flow directly from this trajectory. First, demand is not a short-term spike driven by a single commodity cycle or regulatory change — it is structural and multi-year. Second, the growth profile justifies both near-term tactical investments (e.g., expanding product offerings, targeted capex for energy efficiency) and longer-horizon strategic moves (e.g., M&A to build scale, platform services for aftermarket revenues).

Commercial And Industrial Ro Water Treatment Equipment Market

The market shows moderate concentration. The combined revenue share of the top three and top five suppliers indicates a marketplace where established engineering-led OEMs coexist with nimble specialist providers. This configuration favors diversified strategies: incumbents can leverage scale and global servicing networks, while agile players can win by focusing on niche solutions, customization, and speed-to-deployment.

In our vendor analysis we profile established players known for specific capabilities: custom skid-mounted systems and high-purity solutions from technology-focused fabricators; global pre-engineered and custom portfolio providers with capacity ranges spanning thousands to millions of GPD; manufacturers that tailor designs for harsh environments such as oil & gas and desalination; suppliers integrating advanced membrane monitoring and rental programs; and specialists pushing high-recovery, CCRO-based systems. Recent product activity underscores this dynamic: for example, expanded modular commercial RO portfolios introduced in late 2025 and early 2026 signal supplier emphasis on scalable, site-flexible offerings that accelerate deployment in commercial and industrial applications.

For buyers and operators, the economics of RO are dominated by two levers: capital intensity at the point of purchase and ongoing energy and maintenance costs. Industrial RO systems span a wide capital cost spectrum — from smaller commercial units in the low tens of thousands of USD to large-scale systems that can exceed USD 1 million — making procurement strategy highly dependent on scale, duty cycle, and desired service level.

Energy is a decisive operating cost. For seawater RO plants, energy can account for roughly 35–45% of operating expenses, and treatment costs per cubic meter typically fall within an industry range that reflects plant size, recovery targets, and feedwater characteristics. These dynamics create powerful incentives for buyers to prioritize energy-efficient membranes, high-recovery architectures (including closed-circuit RO), and integrated energy-management strategies (variable-speed drives, energy recovery devices, and intelligent process control).

Regulatory tightening on discharge limits and water quality — especially in sectors such as power generation, pharmaceuticals, food processing, and oil & gas — is a near-universal market input. Stricter effluent criteria accelerate replacement cycles for legacy systems and increase demand for advanced membrane technology capable of higher rejection and predictable long-term performance.

At the same time, buyers face intense pressure to optimize total cost of ownership (TCO). Procurement teams now evaluate offers across a broader set of criteria: energy intensity, footprint and modularity, lifecycle maintenance spend, credit and rental options, and the supplier’s digital monitoring and service capabilities. PW Consulting’s interviews and vendor benchmarking show that procurement decisions increasingly hinge on demonstrable lifecycle cost savings, not just upfront capital outlay.

This release is a “strategic preview” — it highlights core insights while reserving detailed segment-level numbers and granular regional and application splits for the full report. The comprehensive report provides the following practitioner-oriented deliverables:

The preview intentionally omits core segment-level revenue splits and region-by-region allocations to protect the analytic utility of the full dataset. These withheld metrics are, however, essential to validate site-level investment decisions and to underpin M&A valuation models — they are included in the full subscription report available via our website.

Based on our synthesis of market growth, cost structure, regulation, and vendor dynamics, PW Consulting recommends that executives align 2026 plans around three priorities:

Given the market’s moderate concentration, acquisitive moves remain a credible way to accelerate capability buildout. Targets with two attributes will command premium valuations in 2026: (1) proven modular/skid-mounted manufacturing expertise, and (2) digital service platforms that enable predictive maintenance. Strategic alliances — for energy recovery suppliers, membrane manufacturers, and digital analytics providers — can also create differentiated, low-capex pathways to compete with larger incumbents.

Recent vendor activity validates these priorities. Product portfolio expansions that emphasize modular formats and higher flow-capacity commercial systems reflect supplier efforts to serve larger commercial and industrial footprints while shortening lead times for customers.

PW Consulting’s full report is designed to be directly actionable for procurement heads, plant managers, investor teams, and corporate development executives. Beyond the market model and vendor profiles, clients receive scenario-driven capital planning templates, an ROI calculator for energy-efficiency upgrades, and an M&A diligence checklist keyed to technology and service risks.

If your 2026 capital and procurement cycle includes water treatment investments, the intelligence in the full report will materially improve the precision of your decisions — from sizing systems to structuring supplier contracts and identifying high-priority retrofit candidates.

This article functions as a strategic primer. For the complete dataset, granular segment breakouts, and the full suite of decision tools referenced above, please consult the PW Consulting report page. Subscribers and corporate clients can also request a tailored briefing and a 60-minute workshop to run through the report implications for specific portfolios or sites.

PW Consulting’s market analysis delivers the combination of quantitative rigor and practical playbooks necessary to convert market growth into sustainable value — whether you are optimizing plant-level operations, structuring procurement for a portfolio of sites, or evaluating strategic acquisitions in the RO equipment space.

For detailed analysis of this topic, please visit the official page:Commercial And Industrial Ro Water Treatment Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com