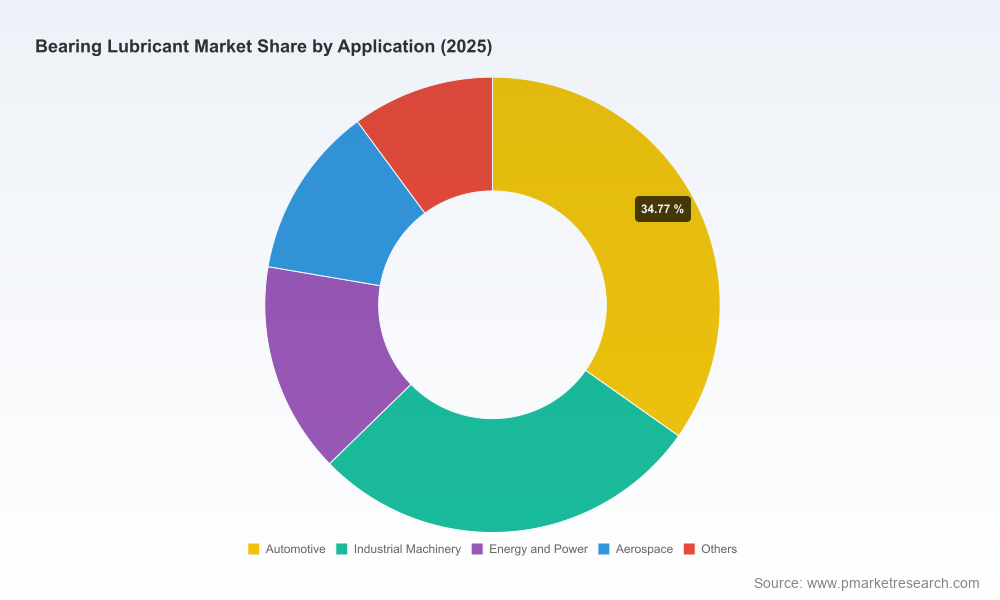

Bearing Lubricant Market — Strategic Imperatives for 2026

PW Consulting’s latest Bearing Lubricant Market study (base year: 2025; forecast 2026–2032) synthesizes proprietary modeling, supply-chain overlays and competitive forensics to arm executives with the evidence they need to make high‑stakes decisions in 2026. Our top‑line projection: the global bearing lubricant market — expressed in USD Million — is set to continue its steady trajectory from the 2025 baseline, expanding at a compound annual growth rate (CAGR) of 4.12% through the 2026–2032 forecast window. By 2032 the market reaches a materially larger scale than today, driven by premiumization, electrification of transport, renewables deployment and tightening regulatory requirements.

Bearing Lubricant Market

Why this report is decision‑critical for 2026

Several structurally transformative forces converge in 2026. Material cost volatility, regulatory tightening, tariff re‑shaping of trade flows and an increasingly concentrated supplier landscape are creating both risk and strategic opportunity. Our study identifies how these forces interact across product lines, customer segments and channels so that commercial, procurement and R&D leaders can prioritize investments with conviction rather than by instinct.

Bearing Lubricant Market

- Concentration and competitive dynamics: The market displays moderate concentration at the top, creating both the competitive pressure of global incumbents and openings for focused specialists. The CR3 and CR5 concentration metrics in our analysis illuminate where scale matters most and where niche plays can deliver outsized returns.

- Cost and supply shocks: Base oil feedstock moves are no longer transitory — for example, base oil price volatility contributed to an 8% YoY rise to approximately $850/MT in Q1 2026. PAO synthetic base stock pricing and availability are uneven across regions, elevating procurement risk for premium formulations.

- Regulatory and standards uplift: New and updated standards — notably ISO 12925-1:2023 and renewed EU REACH restrictions around PFAS compounds — are accelerating reformulation timelines for high‑performance greases and oils, and shifting long‑term supplier advantage toward firms with stronger chemistry and compliance capabilities.

What’s inside the PW Consulting report (practical, not promotional)

- Macro-to-micro financial model (USD Million): forward-looking market sizing, scenario runs and sensitivity analyses spanning 2026–2032, plus margin and pricing models that incorporate base oil and synthetic feedstock dynamics.

- Regulatory risk matrix: quantifies operational and reformulation impact across geographies and product types, with action timelines keyed to EU and global standard updates.

- Supply-chain heatmap: visibility to critical nodes, single‑source vulnerabilities and inventory strategies that are consistent with just-in-time and just‑in‑case hybrid models.

- Competitive playbooks: strategic profiles and capability maps for the industry’s leading suppliers, with go‑to‑market and product-innovation archetypes (examples below).

- Execution toolkits: procurement hedging templates, R&D roadmaps for PFAS‑free alternatives, and an ROI calculator for localized manufacturing investments aimed at tariff mitigation.

Data‑driven insights without the spoiler (the trailer approach)

Our analysis reveals repeatable, actionable patterns without disclosing the full granular splits that we reserve for subscribers. Key patterns you can act on now:

Bearing Lubricant Market

- Premiumization persists. Across end‑use sectors there is a clear tilt toward synthetic and specialty chemistries that extend bearing life, reduce downtime and support electrified systems. Recent product activity underscores this — e.g., Klüber’s June 2025 launch of a food‑grade, NSF‑H1 certified high‑speed grease and Shell’s early‑2025 expansion of EV‑focused grease availability.

- Regulatory compliance is becoming a market differentiator. SKF’s April 2025 update to their LGHP grease to meet the latest REACH requirements signals that compliance investments are no longer a back‑office checkbox; they are a commercial moat for suppliers to large OEMs (wind, automotive, industrial).

- Electrification and renewables drive distinct demand profiles. Electric motors and wind turbines impose thermal, electrical and long‑life requirements that favor certain chemistries and supplier relationships. Those suppliers who can align formulation, testing and field validation will secure premium aftermarket share.

- Raw material availability will be a gating factor. PAO and other synthetic stocks show regional price dispersion — ICIS reported PAO at about $2.2/kg in Asia‑Pacific late‑2025 — making sourcing strategy central to margin planning.

Strategic recommendations for 2026 (practical, prioritized)

We advise senior executives to translate the report’s scenarios into a 12‑month “no regret” plan and a 36‑month investment roadmap. Priorities for 2026 include:

- Prioritize product tiers: Reallocate R&D and commercial focus toward premium and compliance‑aligned formulations where price elasticity is lower and margins are higher. Pilot PFAS‑free alternatives now to avoid 2026/2027 compliance cliffs.

- Lock in feedstock through blended procurement: Move from spot exposure to a mix of term contracts, index‑linked price collars and strategic inventory buffers for base oils and PAOs.

- Localize selectively to avoid tariff shocks: In markets affected by trade measures, near‑market manufacturing or toll‑blending partnerships will protect commercial competitiveness while preserving global scale.

- Embed product‑as‑service capabilities: Offer condition‑based lubrication services (sensors, analytics, predictive replenishment) to capture aftermarket recurring revenue and strengthen OEM ties.

- Use M&A and partnerships to fill capability gaps: Target bolt‑on acquisitions that deliver regulatory chemistry expertise, niche industry relationships (e.g., food, aerospace) or advanced testing facilities.

- Operationalize standards readiness: Accelerate internal testing programs aligned to ISO 12925-1:2023 and ensure documentation and change management processes are audit‑ready.

Competitive landscape — what incumbents and challengers are signaling

The market is shaped by a mix of global majors and specialized regional players. Our report dissects the strategic intents and capability differentials of the leading companies so decision‑makers can benchmark partner, supplier and acquisition targets.

- Klüber Lubrication (Germany): Focused on high‑performance greases and specialty food‑grade chemistries; recent product launches demonstrate a deliberate play for speed‑sensitive and hygienic applications.

- Shell Lubricants (Netherlands): Leveraging scale and brand to accelerate EV-relevant greases; product expansions into electric‑vehicle bearings highlight a platform approach to new mobility demands.

- Mobil / ExxonMobil (USA): Portfolio breadth across industrial and food‑grade lines makes them a go‑to for large OEMs; investment in electric motor solutions is a defensive and offensive move.

- SKF (Sweden) and Timken (USA): Bearing OEMs with integrated lubricant offerings — SKF’s compliance upgrades are a signal that OEM‑aligned lubricants will be preferential in warranty and performance contracts.

- Specialists (Fuchs, Molykote/DuPont, TotalEnergies, Castrol, Chevron): These players compete on chemistry depth, industry specialization (steel, mining, aerospace), and distribution reach; expect continued product differentiation and channel investments.

For mid‑market players, the competitive reality is clear: partner with chemistry specialists, invest selectively in compliance capability, and use service models to defend margins against scale players.

Scenario planning and the PW Consulting watchlist

Our scenario suite models upside and downside outcomes across three axes: material cost shocks, regulatory stringency and trade‑policy shifts. Each scenario triggers a set of recommended actions — from immediate hedges to 18‑month R&D accelerators. Key items on the operational watchlist include:

- Base oil price bands and PAO supply indicators

- REACH and analogous jurisdiction deadlines for PFAS and other restricted substances

- Tariff and trade policy developments affecting import cost and localization ROI

- Adoption rates for condition‑based lubrication services among key OEMs

How PW Consulting helps — practical deliverables

Clients engage us to convert the report’s intelligence into executable programs. Typical deliverables include:

- Customized market segmentation and country‑level demand models (granular datasets withheld in this public summary)

- Commercial playbooks and pricing frameworks calibrated to your product mix and channel strategy

- Procurement and hedging plans for base oil and synthetic stocks

- M&A screening and diligence support focused on chemistry capability and compliance assets

- Pilot designs for field validation of PFAS‑free and long‑life lubricants with KPI measurement

Next steps — get the full picture

This article is intentionally a strategic preview: it surfaces the high‑impact findings and tactical imperatives without disclosing the full, proprietary segmentation and country‑level datasets that senior teams need to operationalize plans in 2026. The complete PW Consulting Bearing Lubricant Market report contains the granular splits, financial models (USD Million), company scorecards, and implementation tools that procurement, product and corporate development teams should use as the basis for 2026 budgeting and multiyear roadmaps.

Contact PW Consulting to request the full report, schedule a briefing workshop, or commission a tailored scenario and readiness assessment for your portfolio. In a market where chemistry, compliance and supply assurance determine competitive position, the right information — and the right playbook — will decide winners in 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Bearing Lubricant Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com