Exterior car wash

Other |

2026-07-02 07:28:05

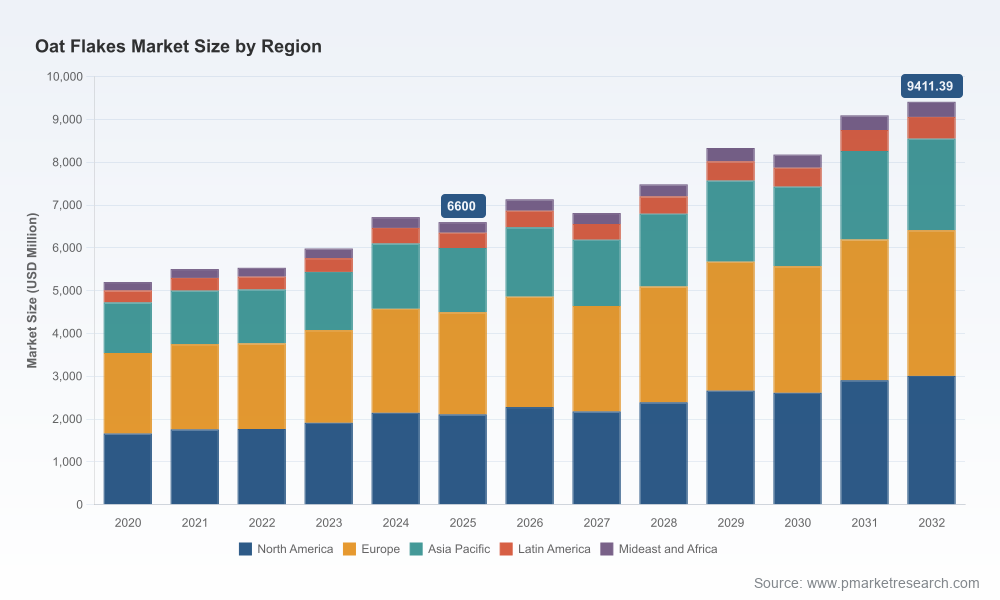

PW Consulting’s latest market intelligence on the global oat flakes sector is designed as an executive-grade toolkit for 2026 decision-makers. Built on a 2020–2025 historical foundation and forward-looking projections through 2032, the study synthesizes macro demand trajectories, raw-material dynamics, facility investments, and competitive maneuvering into a compact set of strategic imperatives. At the top line: the oat flakes market stood at approximately USD 6.6 billion in 2025 and is projected to grow at a compound annual growth rate (CAGR) of 5.2% across the 2026–2032 forecast window, reaching roughly USD 9.4 billion by 2032. This press release presents high-level, actionable insights while intentionally omitting proprietary sub-segmentation tables to direct executives to the full report for the granular inputs required for operational planning.

Oat Flakes Market

Macro resilience with tactical inflection points: A steady mid-single-digit CAGR masks volatility in input costs, regional supply availability, and shifting consumer preferences. Companies that adopt scenario-driven procurement and flexible manufacturing will convert structural growth into margin expansion.

Oat Flakes Market

Value creation increasingly arises beyond commodity flakes: ingredientization (beta-glucan concentrates, oat protein fractions), clean-label positioning, and convenience-format innovation are lucrative adjacencies for brands and ingredient suppliers alike.

Oat Flakes Market

Supply-chain and quality governance are non-negotiable: recent recalls and increasing purity-protocol demand underscore the commercial risk of weak traceability and the premium available to certified supply chains.

This study is organized as a working reference for commercial, procurement, innovation, and M&A teams. It includes:

Top-line market sizing and seven-year forecasts (2026–2032) by macro use-case and product typology, underpinned by scenario sensitivity to commodity pricing and production shifts.

Actionable demand-driver analysis covering health & wellness consumption patterns, retail channel evolution, and industrial formulation opportunities in food, personal care, and feed.

Supply-side diagnostics: crop production trends, processing capacity developments, raw-material price modelling, and structural constraints that influence regional availability.

Competitive and strategic playbooks: detailed company profiles, technology and capacity mapping, go-to-market options, and a matrix of partnership and M&A opportunities.

Operational toolkits: procurement hedging worksheets, capex prioritization templates for new processing lines, and contamination-risk mitigation protocols.

Regulatory and quality track: line items on purity protocols, organic certification drivers, and likely enforcement trends that will affect labeling and export flows.

Note: This press release intentionally refrains from reproducing the report’s proprietary sub-segment tables (regional/application splits and unit-price ladders). Those detailed outputs drive commercial negotiations and are accessible through the report landing page.

Production and availability. Global oat production for the 2025/26 crop year is projected to be materially higher year-on-year, driven by increased acreage and favorable yields in key producing regions. This expands the raw-material envelope for processors but also reintroduces regional imbalances as exporters and processors compete to capture value.

Price volatility and hedging implications. Oat futures demonstrated elevated volatility in 2026, with price levels that demand disciplined procurement and dynamic hedge strategies. For manufacturing and private-label players, even short-term price shocks can compress margins; for branded players, strategic mix-shifting and packaging innovations can preserve retail price positioning.

Processing capacity build-out. New facilities announced globally signal a step-up in installed processing capacity. These investments shorten lead times and reduce logistics costs for localized supply chains but also intensify competition for contracted grain and certified supply, influencing long-term sourcing strategies.

The oat flakes sector remains moderately fragmented: the combined market share of the top three players reflects a substantial role for large millers and branded processors, while the top five firms increase concentration further. This structure creates dual pathways for growth—scale-led cost and distribution advantages on the one hand, and differentiated, premium or certified niches on the other.

Grain Millers Inc. (Eden Prairie, MN, USA) — https://www.grainmillers.com/ Strategy notes: A large ingredient-focused miller with controlled-supply positioning. Recent product-safety incidents highlight the firm importance of end-to-end contamination controls; their scale provides rapid remediation capability but also places reputational risk front-and-center.

Quaker Oats (PepsiCo) (Chicago, IL, USA) — https://www.quakeroats.com/ Strategy notes: A global brand and manufacturing footprint with innovation capacity in convenience formats. Cross-border facility investments underscore an offensive posture to capture growing demand in Asia and to integrate upstream supply via partnerships.

Morning Foods / Mornflake (Crewe, UK) — https://www.morningfoods.com/ Strategy notes: Premium positioning and strong sustainability credentials provide defensive barriers in European retail and specialty channels; premiumization remains a durable route to margin protection.

Avena Foods Limited (Regina, SK, Canada) — https://www.avenafoods.com/ Strategy notes: Niche leadership in certified gluten-free and purity-protocol oats with direct implications for allergy-friendly and clean-label demand—segments exhibiting above-market growth rates in many mature markets.

Richardson Milling (Richardson International) (Winnipeg, MB, Canada) — https://www.richardson.ca/ Strategy notes: Large-scale North American capacity with customization capabilities; an attractive partner for brands seeking co-manufacturing or scale supply chains in the region.

Lantmännen (Stockholm, Sweden) — https://www.lantmannen.com/ Strategy notes: Stronghold in functional oat ingredients (e.g., beta-glucan, protein) with R&D anchoring on ingredientization—an important model for capturing incremental value beyond commodity flakes.

Recent corporate events—new facility construction by major brands, targeted product launches featuring oat-flake formulations, and portfolio expansions around purity-protocol oats—signal an evolving boundary between commodity suppliers and branded innovators. These developments create a playbook for both defensive (operational resilience, quality control) and offensive (premium ingredientization, channel expansion) moves.

Adopt scenario-based procurement: build flexible contracts with tiered pricing triggers tied to futures and physical-market benchmarks; combine short-term hedges with multi-year offtake agreements for key accounts.

Invest selectively in traceability and certification: pursue purity protocols or equivalent supply-chain transparency measures for higher-margin segments (e.g., allergy-friendly, organic), which reduces price elasticity and supports premium pricing.

Pursue ingredientization partnerships: co-develop beta-glucan, protein isolates, and other value-added oat ingredients with processors or co-packers to capture higher per-unit margins.

Prioritize modular capex: favor scalable processing investments (e.g., flexible flaking lines) that allow rapid SKU-switching to meet seasonal demand or formulation trends without expensive retooling.

Optimize quality incident playbooks: implement third-party auditing, rapid lot-tracing, and consumer-communication templates to limit reputational damage and reduce recall costs.

Explore regional partnerships for market entry: use joint ventures or strategic supply agreements to accelerate presence in growth regions while minimizing capex risk.

The report’s forecasting framework uses a base-case CAGR of 5.2% while stress-testing outcomes under alternative supply and demand shocks. Models factor in: prospective increases in global oat production; short-term futures volatility; regional processing capacity ramps; and consumer-adoption rates for premium and convenience formats. For procurement and finance teams, the report includes probabilistic P&L impacts and a set of KPI thresholds that trigger tactical responses (e.g., drawdown of safety stocks, pricing adjustments, or operational scale-ups).

Procurement leads: request the report’s raw-price sensitivity appendix and the hedging playbook to set 2026 purchasing policy.

R&D and product teams: review the functional-ingredient opportunity matrix and partner short-list to accelerate development sprints.

Corporate development teams: use the competitive-scorecard and M&A heat maps to prioritize bolt-on targets and partnership prospects before capital becomes scarce.

PW Consulting’s Oat Flakes Market report is intentionally structured as an operational resource rather than a descriptive overview. The document provides the datasets, modeled scenarios, and tactical templates necessary to translate a projected USD 6.6 billion market in 2025 and a 5.2% CAGR into concrete 2026 action plans. To obtain the full sub-segment tables, company scorecards, and the proprietary forecasting workbook that inform contractual and capex decisions, please visit the report landing page for purchase and licensing options.

For detailed analysis of this topic, please visit the official page:Oat Flakes Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com