Why Investors Are Focusing on the Rapidly Expanding US Genetic Engineering Drug Market

Health |

2026-07-02 09:35:02

As organizations across semiconductor fabrication, electric vehicle manufacturing, aerospace, refrigeration, and industrial power systems recalibrate testing and quality workflows, rental models for helium leak detection are emerging as a tactical lever for reducing capital intensity, accelerating time-to-test, and managing supply-chain exposure to scarce helium. PW Consulting’s latest market study — the Helium Leak Detector Rental Services Market (base year 2025, forecast 2026–2032) — synthesizes historical performance (2020–2025) and forward-looking scenarios to equip procurement, operations, and engineering leaders with actionable intelligence for 2026 planning cycles.

Helium Leak Detector Rental Services Market

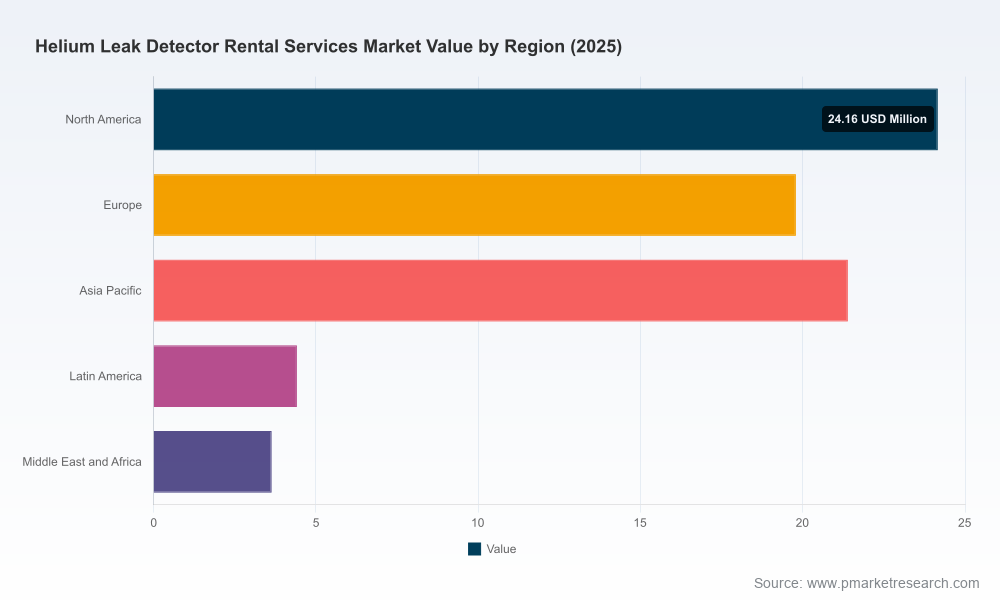

Helium-dependent leak testing remains mission-critical across high-value industries, yet the economics of ownership versus rental are changing rapidly. Our analysis quantifies that the global rental market reached USD 73.4 Million in 2025 and is poised to expand to roughly USD 80.4 Million in 2026, continuing at a compounded annual growth rate (CAGR) of approximately 7.79% through the forecast window. By 2032 the market is projected to approach the low-to-mid triple‑digit USD Million range, underscoring sustained demand for flexible test capacity.

Helium Leak Detector Rental Services Market

For 2026 budgeting and capital allocation decisions, the report supplies scenario-based models that compare CapEx acquisition, short-term rental, and hybrid fleet strategies under different helium-price and supply-shock assumptions — a practical necessity given ongoing helium availability constraints and regulatory shifts that broaden helium’s permitted use in certain hydrogen-system tests.

Helium Leak Detector Rental Services Market

Procurement and operations teams will find tools to translate top-line market direction into bottom-line actions: vendor selection heuristics, rental-duration optimization, technician staffing guidelines, and ensured service levels for critical production windows.

Flexibility over ownership: With rental market growth outpacing many adjacent NDT and vacuum-equipment segments, rental arrangements increasingly deliver faster access to model diversity (portable sniffers, bench mass spectrometers, and wet-model capability) and provide insurance against downtime during peak validation cycles.

Supply-risk mitigation: Helium scarcity and pricing volatility are tangible operational exposures. Our stress-tested forecasting shows that integrating rental options with on-site helium recovery and diluted‑helium protocols materially reduces both testing cost volatility and throughput risk under supply disruption scenarios.

Regulatory opportunity: Recent U.S. regulatory updates authorizing inert gas (including helium) for certain closure and leak tests in hydrogen vehicle systems, plus specified volumetric limits for CHSS post-crash testing, expand addressable demand for qualified rental fleets — especially for firms moving from prototype to small-scale production in 2026.

Service and skills are the differentiators: The cost of skilled field technicians to operate mass spectrometers and manage on-site recovery systems remains a primary operational expense. Providers emphasizing rapid-response field teams and turnkey testing protocols capture higher margins and deliver superior uptime for OEMs and system integrators.

Market sizing and trajectory: Historical data (2020–2025), a 2025 base-year snapshot, and a detailed 2026–2032 forecast with sensitivity bands tied to helium price and supply scenarios.

Procurement playbook: Decision trees and TCO templates that allow procurement teams to simulate rental term lengths, response-time SLAs, insured liability options, and insurance/maintenance clauses against production-critical use cases.

Operational playbooks: Field-testing checklists, technician competency matrices, on-site helium recovery and dilution approaches, and downtime-avoidance protocols tailored to production, R&D, and lab-validation workflows.

Vendor scorecards and RFP templates: A comparative evaluation framework covering fleet breadth, brand access (third-party OEM models), global travel capability, repair turnaround, and after-hours support—designed to speed vendor selection without sacrificing technical fit.

Scenario analyses: Portfolio-optimization models for mixed rental/ownership strategies under four discrete futures: stable helium supply, chronic supply constraint, rapid EV/semiconductor demand surge, and accelerated regulatory adoption in hydrogen safety testing.

Risk register and mitigation map: Helium procurement, logistics, technician attrition, and compliance risks together with mapped mitigations and estimated 12–36 month impacts on test capacity and unit cost.

The rental market exhibits moderate fragmentation, with a small set of entrenched specialists and several OEMs and rental integrators offering complementary capabilities. The top-three players account for a meaningful, but not dominating, share of market revenue—leaving room for regional specialists, niche service providers, and OEM-backed rental programs to win project-level business.

UTE/Distributor‑led rental and multi-brand inventory providers: Companies like ATEC (Advanced Test Equipment Corp) maintain broad catalogs, enabling short‑term access to leading OEM models without long delivery lead times.

Field-service specialists and rapid-response networks: HVS Leak Detection and similar operators compete on turnkey field services, worldwide travel, and on-site mass spectrometer expertise—critical where operational continuity outweighs lowest unit rental cost.

OEMs and authorized service partners: INFICON, Leybold, and Edwards Vacuum offer rental units as part of wider after‑sales portfolios, which can be attractive for buyers prioritizing OEM-certified maintenance and integrated spare support.

Regional NDT and equipment rental firms: Firms such as EQUIPCO Services, High Vac Depot, LACO Technologies, Vacuum Instrument Corp (VIC), Pine Environmental Services, UHV Tech Services, and High Vac Depot balance localized logistics, targeted model sets, and project-oriented pricing for short-run or geographically constrained needs.

We profile each major provider across service attributes: fleet diversity, response time, global reach, repair and calibration turnaround, and capability to support specialized protocols (e.g., wet models, sniffer vs. vacuum testing, and closed-loop recovery). Recent provider activity — including VIC’s updated flexible weekly/monthly rental program and HVS’s field service refresh — highlights an emphasis on rental-tenor flexibility and expanded field capability, signaling competitive focus areas through 2026.

Compliance expansion: Regulatory changes permitting helium use in certain hydrogen vehicle tests and defining volumetric ceilings for CHSS post-crash testing create upwards pressure on short-term rental demand as OEMs validate new designs against updated standards.

Helium supply constraints: Ongoing supply and logistics constraints are accelerating buyer interest in diluted‑helium methods, helium recovery systems, and rental-linked recovery options. The report models cost and throughput implications for each approach across typical production scenarios.

Human capital premium: Skilled technicians remain the rate-limiting resource for mass-spectrometer‑based field testing; organizations relying on rental providers benefit from bundled expertise, while those building internal teams face recruiting, training, and retention investments that should be quantified as part of any make-vs-rent decision.

Procurement leaders: Use the vendor scorecards and RFP templates to compress vendor onboarding timelines and to negotiate rental terms that align with production cadence and indemnity requirements.

Operations and engineering: Apply the scenario models to set contingency buffers (spare fleet hours, on-call field service) and to determine where in-house capability is justified by frequency of testing, test complexity, or confidentiality constraints.

Finance and strategy: Integrate the TCO and sensitivity analyses into capital planning — especially for companies weighing permanent fleet additions for high-throughput test lines versus rental strategies that decouple equipment CapEx from production scaling.

To maintain the value of our primary research and preserve commercial sensitivities, this executive briefing omits granular, segment-level revenue splits and region-by-region percentage breakdowns. The full report contains detailed segmentation tables, model inputs, and downloadable financial models that buyers can use to run bespoke scenarios. This “preview” approach allows us to demonstrate methodological rigor while directing practitioners to the comprehensive dataset and tactical tools required for procurement contracts and implementation planning.

Conduct a rapid inventory of upcoming validation workstreams in 2026 and tag tests by helium intensity, regulatory risk, and confidentiality needs.

RFP shortlist formation: Use our vendor evaluation checklist to identify 3–5 providers that match your geographic footprint, response-time requirements, and technical model needs.

Pilot a hybrid approach: Run a 3–6 month pilot combining short-term rentals with leased recovery systems to validate throughput assumptions and helium consumption profiles under production-like conditions.

Embed contractual flex: Negotiate rental agreements with scale-up/scale-down provisions, defined uptime SLAs, and clear responsibilities for calibration and helium recovery to avoid ambiguous service gaps during validation surges.

PW Consulting’s Helium Leak Detector Rental Services Market report is designed to be directly actionable for 2026 capital and operational decisions. The study pairs market-level forecasting (base year 2025, forecast 2026–2032, CAGR ~7.79%) with procurement and operations toolkits intended to shorten the path from insight to execution. For access to the full dataset, segment-level tables, and downloadable models, please visit our report page or contact our industry practice team to schedule a briefing tailored to your program needs.

For detailed analysis of this topic, please visit the official page:Helium Leak Detector Rental Services Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com