Experts Predict Electric Personal Mobility Devices Will Redefine Transportation by 2035

Other |

2026-06-08 09:37:57

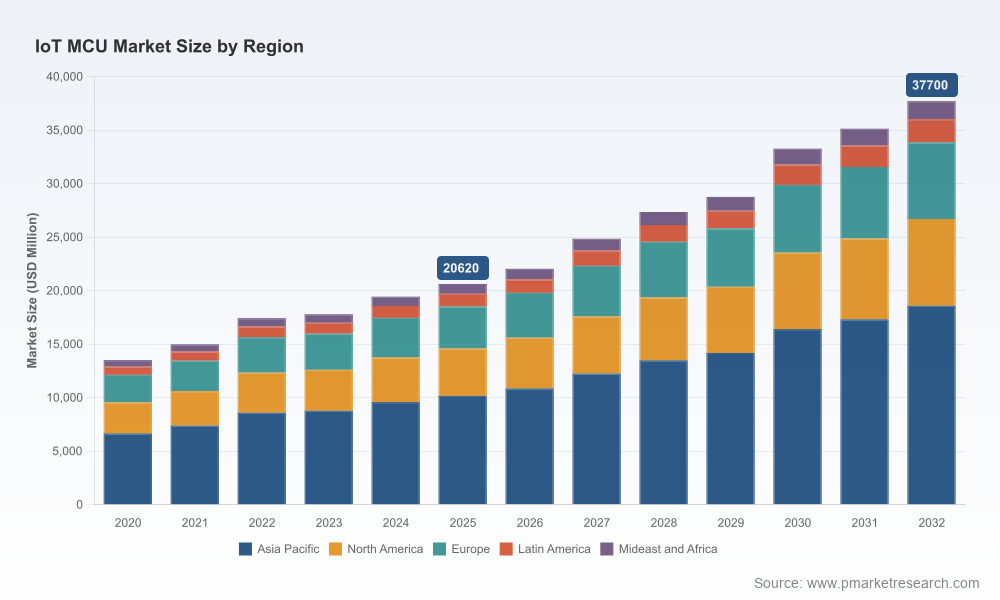

As global device architectures accelerate toward distributed intelligence, PW Consulting’s latest IoT MCU Market report identifies a clear growth runway for microcontroller units that combine compute, connectivity and security. The market reached approximately USD 20.62 billion in our 2025 base year and is modeled to expand at a compound annual growth rate (CAGR) of 9.0% over the 2026–2032 forecast window, approaching roughly USD 37.7 billion by 2032. For corporate leaders planning 2026 investment cycles — from product roadmaps and sourcing to M&A and standards engagement — the report translates these macro dynamics into actionable decision frameworks without surrendering the competitive playbook to public disclosure.

Iot Mcu Market

Timing for platform bets: The 9.0% CAGR and the acceleration in connected-device use cases mean that firms must re-evaluate platform longevity and modularity earlier in their product life cycles. Choosing an MCU family today is a multi-year architecture decision impacting software investment, certification effort and service economics.

Iot Mcu Market

Security & compliance as procurement drivers: New regulatory programs and voluntary labeling schemes have turned security from a checkbox into a market differentiator. Compliance timelines (regional and international) will materially affect vendor selection and certification roadmaps in 2026 procurement cycles.

Iot Mcu Market

Cost-to-performance re-weighting: With MCUs converging on higher compute while preserving ultra-low-power profiles, engineering and sourcing teams need a more granular TCO lens that includes lifecycle update costs, SDK/toolchain stability and certification expenses, not just per-unit BOM cost.

Channel and supply resilience: The increasing share of higher-performance, wireless-enabled MCUs shifts supply risk concentration to a smaller set of advanced foundry-and-package supply chains. Buyers must incorporate supply-availability and lead-time scenarios into SKU rationalization and safety stock policies.

PW Consulting’s IoT MCU Market report is designed as an operational playbook for executives and product leaders. Key elements include:

Macro market sizing and scenario modeling: Base-year calibration and a seven-year forecast with upside/downside scenarios to stress-test investment timelines.

Vendor scorecards: Multi-criteria assessments covering connectivity breadth, security features (secure boot, hardware root-of-trust, over-the-air update support), power-efficiency profiles, ecosystem/toolchain maturity and long-term availability guarantees. These are presented to support shortlisting and negotiation strategies without exposing competitor revenue splits.

Go-to-market decision matrices: Guidance on choosing MCU classes by product horizon (next-gen refresh vs. long-tail maintenance), including recommended criteria thresholds and trade-offs for sensor nodes, consumer gateways, industrial endpoints and medical/regulated devices.

Supply-chain & sourcing playbook: Risk heatmaps, contract levers, dual-sourcing templates and inventory hedges tailored for semiconductor glidepaths and lead-time volatility in 2026–2027.

Regulatory compliance checklist: Practical steps and timelines to align MCU-based designs with emerging regional and international security standards and certification programs.

Investment & M&A signals: Criteria for target screening and integration playbooks for technology tuck-ins versus capability-accretive acquisitions.

The IoT MCU ecosystem blends long-established silicon houses with fast-moving, software-centric entrants. Our analysis highlights three structural realities companies must factor into 2026 plans.

Consolidation of capability sets: Leading semiconductor vendors are offering integrated wireless MCUs, expanded security subsystems, and richer SDKs. These “one-stop” platform propositions lower time-to-market but can create higher switching costs later. Procurement policies should balance platform richness against lock‑in risk.

Specialization persists: Several firms continue to differentiate via ultra-low-power leadership, high-precision analog integration, or multi-protocol wireless stacks. Product teams should match these specializations to end-use constraints (battery life, measurement fidelity, or protocol interoperability).

Software and standards ecosystems now shape hardware adoption: Vendors that offer robust, certified middleware, Matter-compliant SDKs, or secure update infrastructures are seeing faster adoption among OEMs focused on interoperability and service continuity.

Representative vendor implications drawn from our vendor-level review:

NXP Semiconductors (Eindhoven): Strength in crossover MCUs and Matter/MCS-aligned SDKs supports OEMs targeting smart-home gateways and industrial edge devices with integrated connectivity and hardware security.

STMicroelectronics (Geneva): The STM32 family’s breadth and low-power variants remain attractive for companies needing wide software ecosystem support and long-term product availability.

Infineon Technologies (Neubiberg): Power-management and secure-element integration make its offerings appealing where functional safety and secure firmware life-cycle management are prioritized.

Microchip Technology (Chandler): The PIC/SAM families — and recent high-performance introductions — are positioned for math-intensive edge analytics and industrial control where mixed-signal performance matters.

Renesas Electronics (Tokyo): Recent dual-band Wi‑Fi 6/Wi‑Fi/BLE MCU launches underscore a push into higher-throughput, connected-home and IoT gateway applications that demand simultaneous radio stacks.

Texas Instruments (Dallas), Silicon Labs (Austin), Espressif (Shanghai), Nordic Semiconductor (Trondheim), Nuvoton (Hsinchu), Holtek (Taipei), Broadcom (San Jose) and Analog Devices (Wilmington): each brings differentiated value — from ultra-low-power sensors to high-integration wireless SoCs and precision analog MCUs — that should be matched to specific product and regulatory constraints.

The regulatory environment is reshaping MCU selection criteria. Key developments tracked in the report include:

Interoperability programs such as Matter certification are influencing silicon roadmaps and providing pathways for ecosystem lock-in and reduced integration risk for OEMs.

Regional security guidance and labeling schemes (including voluntary federal marks and detailed IoT security standards) are lifting baseline expectations for secure boot, secure updates and vulnerability handling, shifting certification cost into product TCO rather than optional overhead.

Radio equipment directives and regional standardization roadmaps increasingly require vendors and OEMs to demonstrate privacy and security by design for wireless-enabled MCUs, accelerating demand for silicon with hardware roots of trust and on-chip crypto acceleration.

PW Consulting’s report is structured as a playbook for cross-functional teams. Recommended use cases for 2026:

Product strategy workshops — use the vendor scorecards and go-to-market matrices to align hardware choices with three-year service and certification plans.

Procurement and supply planning — apply the supply heatmaps and scenario models to set dual-source thresholds and buffer policies for critical MCUs.

Security & compliance roadmaps — prioritize MCU features and vendor commitments that reduce certification timelines and ongoing update liability.

M&A screening — leverage our investment signals to short-list targets that accelerate software, radio or security capabilities rather than solely chasing unit-volume synergies.

The report synthesizes five years of historical market activity (2020–2025), primary interviews with OEMs and silicon vendors, proprietary shipment and ASP models, and regulatory-trend overlays. We triangulate market-size estimates using component revenue flows, foundry and packaging capacity, and channel inventory modeling. Scenario ranges reflect sensitivities to radio-standard adoption, edge AI acceleration, and regional compliance timelines.

This release is a strategic preview designed to help executives frame 2026 decisions. The full report contains the detailed segment-level analysis, vendor scorecards, and downloadable datasets that operational teams need to execute hardware selection, sourcing and compliance plans. To access the complete intelligence suite, including the segmented market models and supplier-level matrices, visit our report landing page and request the full dossier.

MCUs are no longer just low-level controllers; they are strategic levers that determine product flexibility, security posture and long-term service economics. With the market growing at a solid mid-single-digit-to-double-digit pace and regulatory landscapes tightening, 2026 will be the year many companies either lock into higher-value, software-backed MCU platforms or reconsider their hardware-software boundary. PW Consulting’s IoT MCU Market report gives executives the scenario-tested frameworks and operational tools to make those choices with confidence — and the granular datasets behind those recommendations are available through our full report.

For detailed analysis of this topic, please visit the official page:Iot Mcu Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com