Antifibrinolytic Market Trends, Challenges, and Forecast 2025 –2032

Home |

2026-06-22 10:02:45

As enterprises recalibrate product roadmaps and procurement strategies for 2026, embedded Wi‑Fi modules have moved from a commoditized component to a strategic design decision that materially impacts product differentiation, time‑to‑market, and long‑term total cost of ownership. Our latest market model captures the evolution of the embedded Wi‑Fi modules market through 2032, quantifying a clear structural upshift: from a mid‑market industry in 2020 to a multi‑billion dollar market by the end of the decade. Between 2020 and 2025 the sector demonstrated resilient expansion, and our forecast projects a compound annual growth rate (CAGR) of 13.59% across the 2026–2032 horizon. This growth trajectory creates both enlarged opportunity and heightened complexity for OEMs, module suppliers, and ecosystem partners.

Embedded Wi Fi Modules Market

Standards and spectrum are aligning. Wi‑Fi 7 (IEEE 802.11be) has catalyzed roadmap re‑engineering across chipset and module suppliers, driving demand for support of wider channels and higher throughput in embedded form‑factors. At the same time, regulatory shifts on 6 GHz access — notably recent FCC authorizations that enable geofenced variable power and expanded very‑low‑power paradigms — materially change technical tradeoffs for embedded devices that must balance range, power, and coexistence with incumbents.

Embedded Wi Fi Modules Market

Supply chain and component constraints remain a gating factor. While chipset innovation accelerates, the semiconductor supply chain continues to present capacity and bill‑of‑materials challenges that particularly affect high‑bandwidth Wi‑Fi 7 and Wi‑Fi 6E solutions. Organizations that integrate realistic lead‑time assumptions and alternative sourcing mechanisms into their 2026 plans will materially reduce product launch risk.

Embedded Wi Fi Modules Market

Product differentiation is moving into software and system integration. As basic Wi‑Fi connectivity settles into design templates, the competitive edge shifts to secure provisioning, OTA update frameworks, edge compute capabilities, and Matter/Thread/other ecosystem integrations. Manufacturers that treat embedded Wi‑Fi modules as the foundation for a broader connectivity stack capture a premium in value and durability.

Our topline model shows the embedded Wi‑Fi modules market expanding from the low‑thousands of USD (millions) in 2020 to a substantially larger industry by 2032. The 2025 base year anchors a clear acceleration into the forecast window; by 2032 the market reaches a scale that justifies strategic investments in firmware ecosystems, certification infrastructure, and multi‑source supply strategies. The projected CAGR of 13.59% for 2026–2032 highlights that the market is not merely recovering but structurally growing as Wi‑Fi functionality becomes embedded across a growing set of device classes and use cases.

PW Consulting’s Embedded Wi‑Fi Modules Market report is built for executives and product teams who need actionable guidance, not just descriptive statistics. The report synthesizes macro trends with tactical playbooks and includes:

Demand scenarios and sensitivity analyses that translate standards and regulatory outcomes into revenue implications and BOM impacts under multiple adoption curves.

Supplier scorecards and procurement playbooks that evaluate vendors on eight dimensions (technology roadmap, certification readiness, supply resilience, pricing models, software ecosystem, security posture, regional support, and reference designs).

Integration checklists and RF‑level validation plans tailored for embedded product lines (consumer, industrial IoT, automotive, and medical) to accelerate time‑to‑approval and reduce rework.

Comprehensive risk matrices covering regulatory shifts, raw material volatility, and interoperability failure modes, with mitigation playbooks for rapid incident response.

Commercial models and pricing decks that help procurement teams negotiate multi‑year supply agreements and volume discounts while preserving design flexibility.

A compact executive dashboard: interactive forecasts, market concentration dynamics, and forward‑looking KPIs for board‑level reporting.

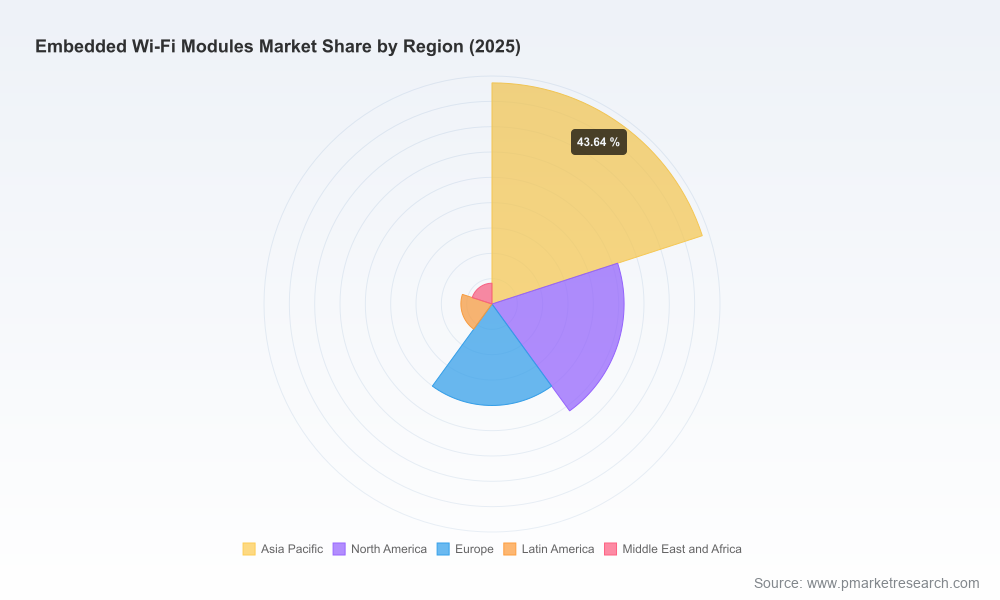

To respect the “trailer” nature of this brief, granular segment breakdowns, regional stacks, and product‑level revenue line items are available exclusively in the full report and interactive dataset.

The market exhibits moderate concentration with the top three players capturing a meaningful portion of industry revenue and the top five representing nearly two‑thirds of the market by revenue concentration metrics. This structure creates distinct strategic choices for OEMs: align closely with a dominant supplier for fast integration and scale, or hedge across specialized vendors to reduce supply risk and lock in differentiated features.

Espressif Systems — Known for highly integrated SoCs and price‑performance leadership in developer ecosystems. Espressif’s broad software community and modular reference designs make it a go‑to partner for rapid prototyping and cost‑sensitive consumer IoT products.

Murata Manufacturing — Specializes in compact, certified modules and excels at miniaturization and automotive/industrial certifications. Their focus on power efficiency and form‑factor reduction appeals to constrained designs requiring pre‑approved, SMT‑ready components.

Silicon Labs, Texas Instruments, Microchip — These suppliers compete on low‑power SoCs, industrial grade features, and long lifecycle commitments typical of industrial and metering applications. Their value proposition centers on predictable roadmaps and extensive reference firmware.

Qualcomm, Broadcom, Infineon, NXP — Chipset incumbents that underpin high‑performance and automotive modules. Their strength is in advanced PHY capabilities, integrated security, and access to tier‑one automotive qualification processes.

Realtek, AzureWave, Quectel, Telit — Aggressive on cost and global distribution, these players often compete on turnkey module availability and rapid certification support for multi‑region launches.

Recent product launches and ecosystem moves underscore the competitive momentum: Synaptics and Qualcomm have introduced micro‑powered Wi‑Fi 7 solutions oriented toward embedded IoT, Murata has expanded ultra‑low‑power long‑range offerings, and several smaller module vendors are shipping Wi‑Fi 7 form factors optimized for M.2 and industrial motherboards. These developments compress feature parity timelines and put a premium on integration skills and firmware flexibility.

Regulatory decisions around 6 GHz access — including expanded allowances for geofenced higher‑power operation and long‑standing frameworks for very‑low‑power devices — materially change RF design constraints and market opportunities. Systems designed for global deployment must accommodate divergent regional regimes and certification paths.

Wi‑Fi 7 enablement at the module level (support for 320 MHz channels and advanced multi‑link operation) is not a simple drop‑in upgrade. It requires rethinking thermal budgets, memory footprints, and antenna systems. Chipset lead times and DDR/DRAM availability remain sources of execution risk through 2026.

Security expectations have hardened: regulators and enterprise customers increasingly demand secure boot, hardware root‑of‑trust, and supply‑chain attestations as baseline requirements for modules embedded in regulated industries.

Prioritize modularity in architecture. Abstract the connectivity layer to enable late‑stage supplier substitution and firmware updates without expensive PCB redesigns.

Lock in diversified supply agreements. Negotiate multi‑source clauses, dual‑sourcing milestones, and capacity guarantees to mitigate chipset shortages and long lead times for high‑bandwidth modules.

Embed certification timelines into product plans. Plan for parallel regulatory testing (regional variations across 6 GHz access) rather than sequential approvals to avoid launch delays.

Invest in firmware lifecycle management. Establish secure OTA pipelines, a vulnerability response playbook, and continuous compatibility testing across Wi‑Fi generations and Bluetooth coexistence scenarios.

Use supplier scorecards as living documents. Track not only price and lead time, but also roadmap alignment, IP restrictions, and ecosystem partnerships that influence long‑term support costs.

The embedded Wi‑Fi modules market presents an attractive growth profile and a complex set of strategic tradeoffs that will define winners and losers in 2026 and beyond. Companies that combine rigorous scenario planning, disciplined supplier engagement, and investment in software and certification capabilities will convert market growth into sustainable competitive advantage. PW Consulting’s full report provides the granular segment forecasts, vendor benchmark data, procurement templates, and interactive models you need to convert these insights into executable plans.

For procurement teams, product leaders, and strategy executives preparing 2026 budgets, the decision levers are now clear — but the execution detail matters. Access the full report to view detailed segment‑level forecasts, vendor heatmaps, and our proprietary risk‑adjusted financial models that underpin these strategic recommendations.

For detailed analysis of this topic, please visit the official page:Embedded Wi Fi Modules Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com