Anti-Oral Mucositis Drug Market Development Through Advanced Drug Delivery Technologies

Health |

2026-05-21 09:57:01

As companies plan their 2026 strategies in specialty chemicals and chiral chemistry, the DL-10-Camphorsulfonic Acid (CSA) market is emerging as a focused battleground for quality, supply resilience, and application-led differentiation. PW Consulting’s forthcoming DL-10-Camphorsulfonic Acid Market report equips executives with the market context and pragmatic tools required to make high-consequence decisions in 2026 — from procurement re-engineering to portfolio prioritization and M&A screening.

DL-10-Camphorsulfonic Acid Market

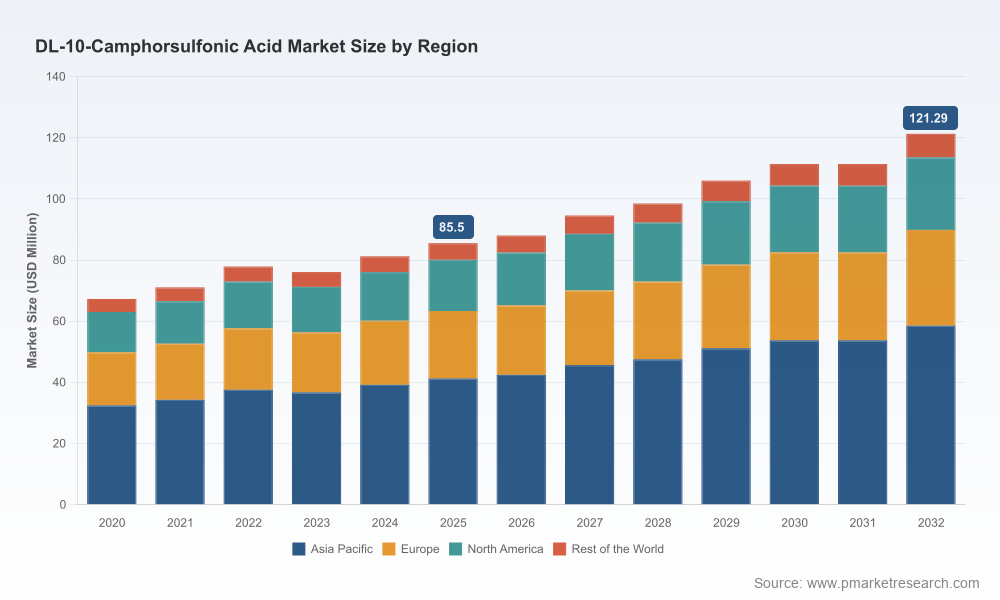

The market for DL-10-Camphorsulfonic Acid has displayed steady recovery and structural growth during the first half of the decade, reaching an estimated market value of USD 85.5 Million in the 2025 base year. Our projection indicates the market will expand at a compound annual growth rate (CAGR) of approximately 5.12% across the 2026–2032 forecast window. By 2026, the market is positioned at roughly USD 88.01 Million, setting a new operating baseline for the next phase of strategic moves.

DL-10-Camphorsulfonic Acid Market

For executives, these headline figures matter for two reasons: first, they confirm an environment of steady demand (not speculative boom-and-bust) that favors disciplined, long-term investments; second, the growth rate implies that incremental advantages in sourcing, quality differentiation, or authorization for pharmaceutical supply chains can translate to outsized returns over a multi-year horizon.

DL-10-Camphorsulfonic Acid Market

PW Consulting’s analysis is designed around the needs of corporate strategists, procurement heads, R&D leaders, and BD teams who must make 2026 commitments with incomplete information. The report combines rigorous market sizing and scenario modeling with actionable playbooks and decision frameworks.

The market is segmented across regional markets, product purity grades, and end-use applications. Key commercial distinctions include pharmaceutical-grade vs. industrial-grade products, and application categories such as pharmaceutical intermediates, resolution of racemates, and catalyst/organic synthesis uses. Our report describes the dynamics and demand drivers within each segment while deliberately withholding segment-level percentages in this summary to preserve the premium value of the full dataset.

Strategically, buyers and producers must recognize that purity and regulatory readiness are the principal differentiators in this market. Firms targeting pharmaceutical supply chains will require investments in documentation, stability data, and validated manufacturing processes; producers focused on industrial or research reagent channels can compete more on price and availability.

The DL-10-CSA market displays a moderate concentration among established specialty chemical suppliers and distributors. The competitive field includes global life-science and reagent players, regional producers, and specialized distributors. This structure creates clear levers for buyers and incumbent suppliers alike: buyers can pursue aggregation and strategic long-term contracts, while suppliers can solidify premium positions through quality certification, secure distribution networks, and value-added services such as custom packaging and technical support.

Highlighted competitive profiles in our analysis include:

Our competitive assessment examines product portfolios, channel strategies, pricing transparency, and service differentiation. The report also includes vendor scorecards and a decision framework for supplier rationalization or diversification moves in 2026.

Resilience is a central theme for 2026 planning. Although the DL-10-CSA market has proven relatively stable, the report identifies critical single-point risks — including reliance on specific precursor chemistries, export controls in regional manufacturing hubs, and potential quality incidents that can create rapid downstream disruptions. The recommended mitigation playbook includes multi-sourcing strategies, dual-certified suppliers, and inventory buffers sized to preserve critical production lines while minimizing working capital impact.

Producers can protect and grow margins by investing in documentation packages and technical services that shorten qualification lead times for pharmaceutical customers. Distributors and catalog suppliers have the opportunity to expand value by bundling technical support, sample programs, and expedited logistics for R&D clients. Buyers should prioritize supplier consolidation where quality and certification matter, and selective diversification where availability and price are primary concerns.

PW Consulting’s DL-10-Camphorsulfonic Acid Market report is not simply a repository of numbers. It converts market sizing into boardroom-ready choices: tactical procurement actions, capital allocation trade-offs, and competitive responses. The combination of a validated market model (covering 2020–2025 historicals and a detailed 2026–2032 forecast) and a library of operational tools (RFP templates, supplier scorecards, scenario playbooks) makes the report uniquely useful for near-term decisions that have multi-year consequences.

Executives who use this intelligence in 2026 will be able to:

This briefing is a strategic preview designed to demonstrate the report’s depth and practical value. The full PW Consulting DL-10-Camphorsulfonic Acid Market report contains the complete dataset, segment-level modeling, and proprietary tools referenced above. For teams preparing their 2026 budgets, supply strategies, or deal pipelines, accessing the full dataset is essential to execute with confidence.

Contact PW Consulting or visit our report page to obtain the detailed market model, segment-level analysis, and bespoke advisory options that will translate this market intelligence into executable plans for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:DL-10-Camphorsulfonic Acid Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com