Medical Aesthetic Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-08 10:07:09

PW Consulting’s latest market research on the Intellectual Property Rights Royalty Management market provides a forward-looking strategic playbook for enterprise leaders, in-house IP teams, law firms, and technology investors making decisions in 2026. Grounded in multi-source market triangulation and validated vendor intelligence, the report quantifies a market that has expanded from a mid-single‑billion base in 2020 to an estimated USD 7,250 Million in the 2025 base year, and projects continued acceleration through the 2026–2032 forecast window at a compound annual growth rate (CAGR) of 9.22%, reaching an estimated USD 13,424 Million by 2032 (USD, Million).

Intellectual Property Rights Royalty Management Market

Timing matters: 2026 is the inflection point where scalable IP monetization moves from tactical to strategic. The report identifies where organizations must invest to capture outsized returns on IP portfolios amid accelerating filing volumes and cross‑border licensing complexity.

Intellectual Property Rights Royalty Management Market

Risk and compliance are now board‑level concerns: New and expanding data privacy regimes, DOJ restrictions on sensitive bulk data transfers, and the EU AI Act create material compliance obligations that affect platform selection, architecture, and contracting.

Intellectual Property Rights Royalty Management Market

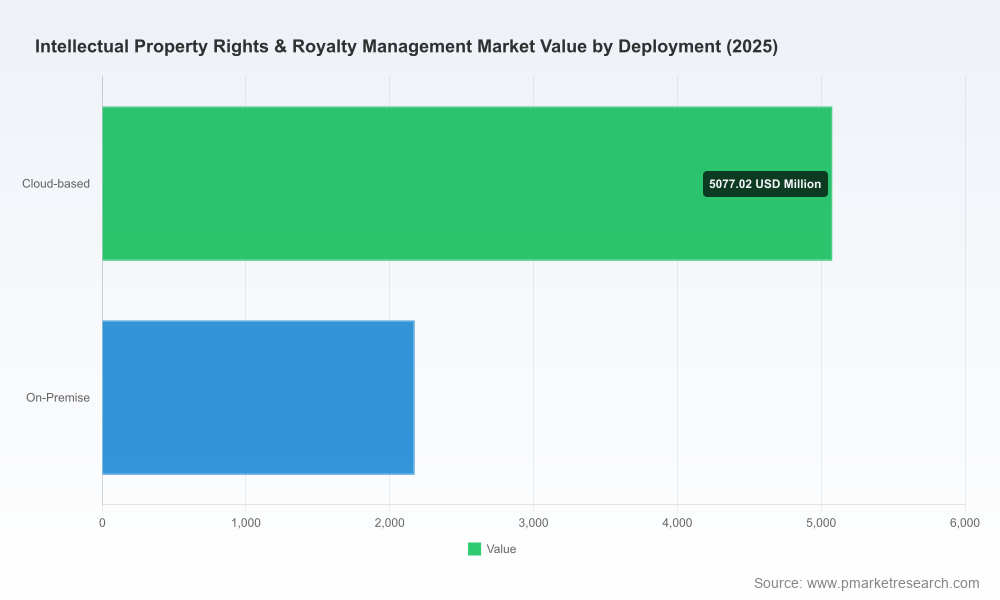

Technology choices determine optionality: Decisions about cloud vs on‑premise deployment, AI-enabled analytics, and integration with finance and ERP systems will lock in capabilities and costs for years—our modelling shows material differences in TCO and time‑to‑value depending on these choices.

Over the historical window (2020–2025) the market grew steadily as organizations expanded portfolio governance and commercialized IP at scale. The 2026–2032 forecast period captures an acceleration driven by three structural forces: rising volumes of patent and trademark filings, broader adoption of AI for valuation and discovery, and increasing demand for cloud‑native rights and royalty workflows that support subscription and usage‑based monetization. The market concentration remains moderate: the top three vendors account for just under one third of market revenues (CR3 ~28.5%), with the top five approaching roughly 38.2%—a landscape that supports both specialist competition and strategic consolidation.

Proprietary market sizing and forecast model (2020–2032), with scenario analysis reflecting regulatory shocks and AI adoption ramps.

Vendor benchmark matrix: functionality, deployment options, integration readiness, AI maturity, professional services footprint, and reference client types—designed for RFP short‑listing.

Total cost of ownership (TCO) and time‑to‑value calculators for cloud and on‑premise paths, including sensitivity to labor costs for AI oversight and compliance roles.

Contract and procurement playbook: recommended contract clauses for data residency, audit rights, liability allocation for AI outputs, and SLA structures aligned to royalty/payment cycles.

Operational blueprint for IP commercialization and royalty operations: process redesign, role definitions (including AI governance and data stewardship), KPIs, and change management milestones.

Regulatory risk matrix and mitigation templates that translate the EU AI Act, emerging US state privacy laws, and DOJ restrictions into procurement and implementation controls.

Investor and M&A companion guide: valuation levers, integration risks, and sprint checklists for bolt‑on acquisitions in the rights/royalty space.

Case studies and vendor negotiation playbooks based on anonymized client engagements covering negotiation tactics, pricing models, and proof‑of‑value deployment patterns.

The market is populated by a mix of IP‑centric platform providers, IP intelligence vendors, enterprise rights/royalty specialists, and media‑focused players. Understanding vendor DNA—whether built for patent portfolio management, technology transfer, or media royalties—is critical to aligning capabilities with organizational objectives.

Anaqua Inc. (US) continues to push AI and commercial pricing innovation. Recent releases introduced an AI‑enhanced platform generation and a consumption‑based pricing model. For buyers, Anaqua represents a high‑function IP management stack with evolving commercial flexibility—best suited for organizations prioritizing automated valuation and decisioning workflows.

Clarivate PLC (UK/US operations) blends deep IP analytics with platform capabilities. Strategic partnerships to embed AI invention generation and computer‑vision for design infringement indicate an ambition to close the gap between discovery, enforcement, and monetization.

Questel (France) and PatSnap (Singapore) emphasize AI‑assisted discovery and analytics. Their roadmaps illustrate an important vendor trend: embedding AI across the lifecycle—from search and landscape to valuation and royalty scheduling—while buyers must weigh explainability and auditability of automated outputs.

Dennemeyer and LexisNexis (RELX) provide broad services and analytics; their strengths lie in global operations and compliance support—valuable for multi‑jurisdictional portfolios where renewal and regulatory complexity dominate operating costs.

Wellspring Worldwide targets technology transfer and licensing workflows, offering specialized royalty accounting and commercialization toolsets for research institutions and corporates seeking structured licensing funnels.

Media and entertainment specialists—Rightsline, FilmTrack, FADEL, Vistex, and Klopotek AG—bring deep functionality for content and publishing royalties. Their templates and payment engines are directly portable to enterprise licensing in sectors with complex revenue share models.

AI platform releases and partnerships are accelerating: expect vendors to push higher‑value modules (valuation, automated dispute detection, infringement monitoring) and to experiment with alternative pricing (consumption and outcome‑based models).

Cross‑industry diffusion: media royalty engines are being adapted to corporate licensing use cases, and IP intelligence companies are embedding rights/royalty workflow modules—raising the bar for incumbents and increasing integration risk for buyers.

Regulatory signals are reshaping vendor contracts and deployment choices: data residency, AI transparency, and restrictions on cross‑border bulk transfers are influencing where and how vendors host and process data.

Adopt a modular procurement strategy: separate core rights accounting from analytics/AI modules so you can replace components without replatforming the entire stack.

Negotiate AI governance provisions: require model documentation, audit trails, and vendor support for explainability where valuations feed financial reporting or licensing decisions.

Plan for regulated data flows: embed data residency and transfer controls in SLAs, and assess the vendor’s exposure to DOJ and state privacy restrictions.

Budget for specialized labor: our analysis finds that human costs for compliance, data governance, and AI oversight remain primary operational drivers—factor this into multi‑year TCO.

Leverage proof‑of‑value pilots: insist on short, targeted pilots tied to commercialization KPIs (e.g., time to licensing decision, royalty leakage reduction) before committing to enterprise licenses.

Monitor consolidation and partnership signals for M&A: vendors extending into adjacent domains (e.g., analytics providers adding rights engines) may become strategic acquisition targets.

Not all buyers need the same platform. Corporates focused on internal product‑centric licensing should prioritize valuation accuracy, ERP integration, and auditability. Law firms need docketing excellence and analytics integration. Research institutions emphasize technology transfer workflows and royalty accounting. Our report includes buyer‑type scorecards and migration roadmaps customized for each profile.

PW Consulting’s market model synthesizes vendor disclosure, proprietary client spend surveys, public filings, and macro drivers (filing trends, licensing activity, and regulatory changes). Scenario testing captures upside from accelerated AI adoption and downside from stringent cross‑border data constraints. Confidence in the headline market trajectory is high—supported by consistent vendor investment and observable shifts in procurement patterns—while subsegment sizing and pricing dynamics remain sensitive to vendor commercial experimentation.

This press release highlights the strategic contours and practical implications of the Intellectual Property Rights Royalty Management market for 2026 decision‑making. The full PW Consulting report contains the detailed segmentation, vendor scorecards, TCO models, and contract language examples that enterprises and investors require to act decisively. To access the complete datasets, benchmarking tools, and implementation templates, please visit the PW Consulting report portal for the full package.

For detailed analysis of this topic, please visit the official page:Intellectual Property Rights Royalty Management Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com