Unlock Your Destiny: Why Vedic Astrology is the GPS for Your Life

Other |

2026-02-16 04:53:32

PW Consulting today publishes an executive briefing of our Ai Speech Generation System Market research, a forward-looking resource designed to guide enterprise decision-making throughout 2026. Anchored on a 2025 base year and built from a five-year historical series (2020–2025), the full report projects the market through 2032. Our core finding: the addressable market is expanding rapidly (compound annual growth of 18.5% across the forecast window), underscoring an inflection point for procurement, product strategy, and risk management in voice AI.

Ai Speech Generation System Market

Timing and scale: With the market scale increasing more than threefold from mid‑decade baselines by the end of this forecast, organizations face a narrowing window to lock in strategic voice capabilities before adoption becomes table stakes for experience-driven use cases.

Ai Speech Generation System Market

Regulatory transition: Policy milestones—most notably EU AI Act provisions becoming operational in 2026—will materially influence vendor selection, deployment architecture, and compliance overhead for voice systems deemed high‑risk.

Ai Speech Generation System Market

Technology acceleration: Recent model releases and cloud vendor updates have compressed capability gaps between specialist startups and hyperscalers. That dynamic raises new questions about performance differentiation, integration risk, and where to invest for long-term competitive advantage.

Robust growth trajectory: Our bottom-up model shows a sustained CAGR of 18.5% for Ai speech generation systems over the 2026–2032 forecast period.

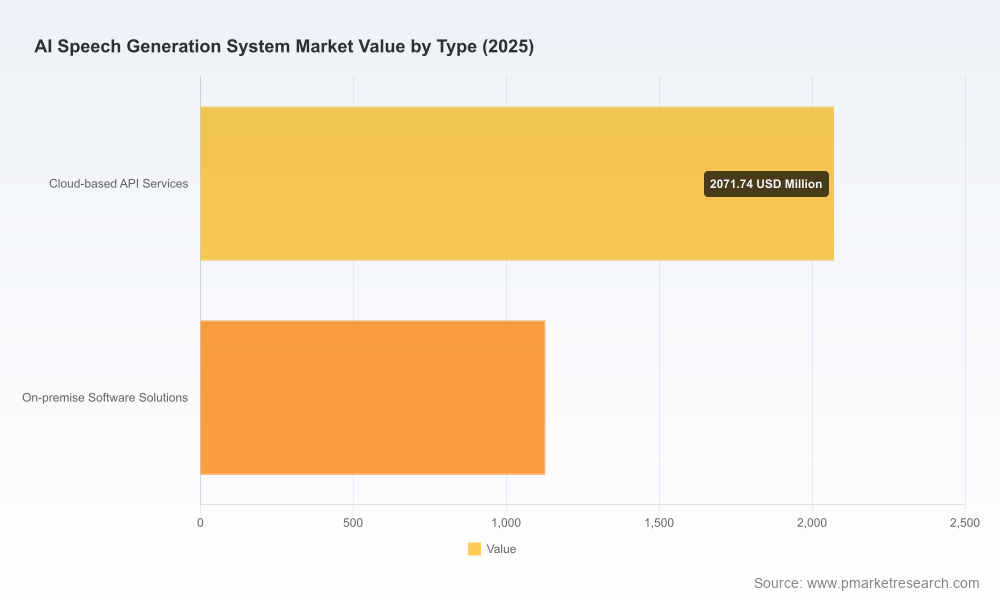

Market magnitude: Based on the 2025 baseline, the market reaches a substantially larger scale by 2032, reflecting broad adoption across enterprise functions—from customer engagement to content production and accessibility solutions.

Concentration and competitive dynamics: The market exhibits moderate concentration (CR3 ≈ 34.5%; CR5 ≈ 48.2%), indicating leading vendors have meaningful share while substantive opportunity remains for niche and regional specialists.

We built this report to be directly actionable for strategy, procurement, and product teams. The deliverables include:

Top-down and bottom-up market sizing models (historical 2020–2025 and forecast 2026–2032) with scenario toggles for adoption speed, price erosion, and horizontal platform consolidation.

Use-case prioritization framework mapping value pools to buyer personas (customer service, e‑learning, accessibility, media/localization, and others), paired with a phased adoption road map.

Detailed vendor scorecards and vendor selection matrix covering technical capability (voice naturalness, expressivity controls, multilingual coverage), operational factors (latency, SLAs, TCO), and compliance posture (SOC 2, GDPR, data residency options).

TCO and ROI tools: downloadable spreadsheet models to estimate per-minute costs, production savings, and multi-year payback under multiple pricing models and quality tiers.

Procurement assets: RFP templates, evaluation checklists, and contract clause libraries for IP, voice consent, watermarking/SynthID, and model governance.

Implementation playbooks: pilot design templates, MLOps integration patterns, data security baselines, and migration guides for cloud, on‑premises, and hybrid deployments.

Scenario-driven risk assessments: regulatory readiness mapping (including EU AI Act implications), reputational-risk mitigation, and contingency plans for model misuse or rights disputes.

To maintain the “trailer” approach for this release, the report overview emphasizes structure and capability without publishing the full segment-level breakdowns and proprietary vendor scores—that detailed intelligence is available in the licensed report and online dataset.

Our analysis identifies three archetypes shaping the competitive map: hyperscale platform providers, specialist voice AI vendors, and API-first startups focused on rapid integration. Each class brings trade-offs between scale, customization, and compliance controls.

Hyperscalers (Google, AWS, Microsoft, OpenAI): Deliver high scalability, broad language coverage, and enterprise-grade integrations. Their strengths are ecosystem synergies and rapid product innovation (e.g., expressive controls, watermarking). Enterprises choosing hyperscalers should assess lock‑in risk against integration and data‑governance needs.

Specialists and platform vendors (ElevenLabs, WellSaid Labs, Resemble AI): Differentiate through ultra-realistic voice models, custom voice cloning, or enterprise security features. These vendors often lead on product features prized by content and media teams—voice quality, emotion modeling, and secure on‑prem/cloud hybrid options.

API-first and creator-focused players (Murf.ai, PlayAI/Play.ht): Prioritize ease of use, developer ergonomics, and cost-effective voiceover workflows for marketing, SMB content creation, and tooling for creators. Their agility makes them attractive for rapid pilots and content-heavy organizations.

Recent ecosystem moves reinforce this interplay. Examples covered in our market chronology include Mistral AI’s frontier-quality open model launch (spring 2026), a strategic integration partnership between ElevenLabs and IBM to bring advanced TTS/STT into an enterprise orchestration platform, and an expressive TTS update from a major hyperscaler (spring 2026) that introduced granular audio tags and watermarking. These events accelerate capability parity and create fresh procurement considerations for buyers in 2026.

Cost economics: Adopters can reduce traditional audio production costs by up to ~70% when adopting synthetic voice workflows for many content workflows. However, meaningful cost variance remains: TTS component pricing in voice stacks typically ranges across an order of magnitude (industry benchmarks place per-minute TTS costs from roughly $0.01 to $0.25 depending on voice quality and provider), and integration, quality assurance, and governance overhead drive overall TCO.

Compliance and security: Enterprise deployments prioritize SOC 2, GDPR, and data residency controls—particularly where voice data is personal or sensitive. The EU AI Act’s provisions (effective around mid‑2026) add disclosure and risk‑assessment obligations for high‑risk voice systems, increasing compliance lift for vendors and buyers alike.

Market concentration: With a CR3 of approximately 34.5% and a CR5 near 48.2%, procurement teams must plan for both vendor risk (concentration and supply continuity) and competitive opportunity (specialists with unique capabilities).

Adopt a use-case-first procurement stance: prioritize pilots for high-value, measurable workflows (e.g., voice agents for after-hours support, automated dubbing pipelines) rather than broad platform bets.

Design hybrid architectures: combine cloud APIs for scale with on‑prem or private cloud options where regulation, latency, or IP ownership demands it.

Insist on measurable quality metrics: evaluate vendors on naturalness, latency, and expressive control using scenario test sets and blind listening panels included in our vendor scorecards.

Negotiate governance and safety SLAs: require model watermarking/SynthID support, logging for traceability, and contractual rights around custom voice models and data retention.

Model financial sensitivity: use multi-price TCO scenarios (low-cost basic voices vs high-fidelity, custom-cloned voices) and build a three-year rollout plan tied to the market growth trajectory.

Prepare regulatory playbooks: map each planned deployment to EU AI Act and local privacy obligations, and stage independent risk assessments as part of procurement acceptance criteria.

PW Consulting’s full Ai Speech Generation System Market report is structured to be directly integrated into boardroom briefings, vendor RFPs, and product roadmaps. Enterprise buyers will find the downloadable models, vendor scorecards, and RFP assets particularly helpful for moving from pilot to production in 2026 without taking unnecessary operational or compliance risk.

For organizations seeking to quantify the impact of the 18.5% CAGR environment on spend, staffing, and capability sourcing, the full dataset and licensing options include manipulable spreadsheets, scenario toggles, and bespoke benchmarking support from PW Consulting analysts.

To secure the comprehensive dataset, detailed segmentation, vendor scoring, and the practical procurement assets described above, visit the PW Consulting report page or contact our industry desk. The preview provided here highlights the structure and strategic value; the licensed report contains the complete modeling, segment-level forecasts, and vendor performance matrices needed to operationalize a 2026 voice AI strategy.

For detailed analysis of this topic, please visit the official page:Ai Speech Generation System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com