Evaluating the Efficacy of Neonatal Intensive Care for Complex Congenital Anomalies in Riyadh.

Health |

2026-06-06 15:52:52

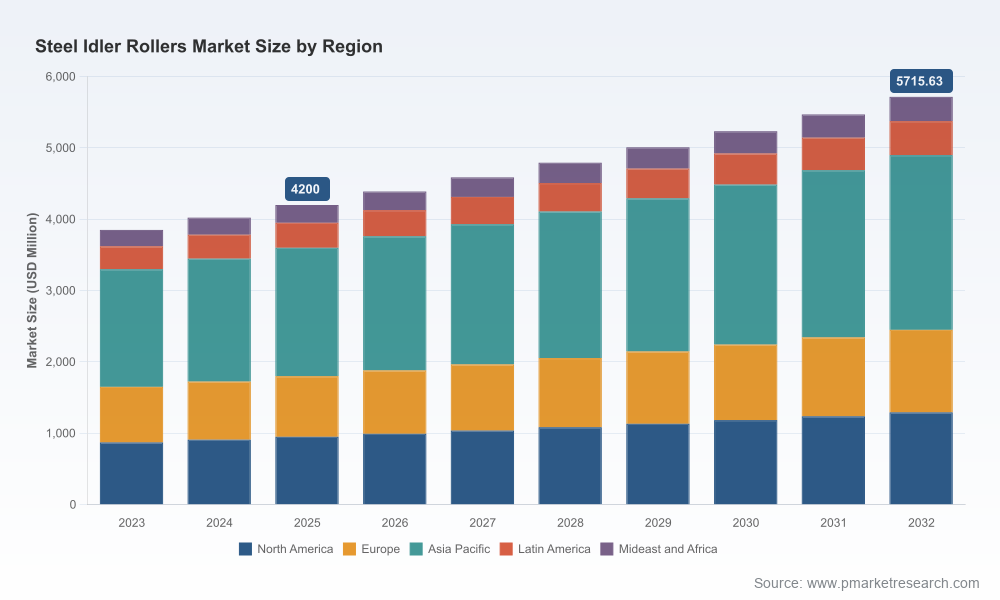

PW Consulting today publishes an executive preview of its forthcoming Steel Idler Rollers Market report, providing decision-makers with a high‑fidelity view of market momentum, competitive dynamics, and practical strategic options to act on in 2026. Anchored on a 2025 base year and a historical series covering 2020–2025, the study projects the market through 2032 using a 2026–2032 forecast horizon. Our core forecast indicates the global market expanding at a steady compound annual growth rate (CAGR) of 4.5% over the 2026–2032 period — a trajectory that translates into an addressable market moving from the low‑billions in mid‑2020s to a materially larger market by the end of the decade.

Steel Idler Rollers Market

Precision timing: 2026 is a hinge year for infrastructure-driven demand and for capital investment cycles across mining, ports, cement and bulk handling — areas where steel idler rollers remain fundamental. Our preview synthesizes the forward momentum and near‑term risks that will shape procurement, product development and M&A decisions in the coming 12–18 months.

Steel Idler Rollers Market

Cost and supply stressors: Volatility in steel and alloy markets has become a recurring margin pressure for roller manufacturers. Our analysis integrates observed swings in high‑grade alloy prices and manufacturing input indices to quantify realistic upside and downside scenarios for OEMs and aftermarket providers.

Steel Idler Rollers Market

Technology and service adjacencies: Advances in coatings, bearing systems and remote monitoring are converting idlers from commodity components into engineered system elements. The report translates these technology shifts into practical commercialization paths and service monetization archetypes.

Historical momentum: Our historical series through 2025 documents the market’s recovery and structural expansion following 2020–2021 disruptions, with year‑on‑year improvements reflected in our 2023–2025 sizing.

Near‑term outlook: Based on our base‑year calibration (2025) and scenario testing, we estimate continued expansion into 2026 and beyond, driven by sustained investment in ports, mining and heavy industry.

Medium‑term growth: The modeled CAGR of 4.5% for 2026–2032 underpins the strategic pathways we recommend — a rate that supports selective capacity additions, targeted product innovation, and incremental consolidation without presuming explosive market re‑segmentation.

Executive decision playbook — concise recommendations tied to buyer profiles (OEM, EPC, end‑user maintenance) and supplier archetypes (global integrator, regional specialist, contract manufacturer).

Market sizing & forecast — a transparent model calibrated to 2025 base year and historical 2020–2025 performance, with scenario variants capturing commodity price shocks, capex cadence changes, and accelerated technology adoption.

Supply chain and cost driver analysis — granular mapping of raw material inputs, processing steps, and labor/CAPEX levers that determine unit economics for steel idler rollers.

Technology and durability deep dive — assessment of coatings, self‑lubricating bearings, and sensorized idlers; practical ROI thresholds for retrofit vs. new‑build strategies.

Commercial benchmark toolkit — supplier scorecards, tender risk matrix, and pricing levers for procurement teams seeking to shorten supplier selection cycles.

M&A and partnership runway — playbook for buyers and investors, including diligence checklists, integration pitfalls, and value‑creation scenarios in a moderately fragmented market.

Regulatory and safety implications — implications of worker safety standards and environmental regulations on product design, warranty exposure and aftermarket liability.

Raw material volatility: Industry sourcing data indicates that prices for high‑grade alloy steels can vary markedly year‑on‑year, with swings that have reached double‑digit percentages in recent cycles. For manufacturers and buyers alike, this elevates the importance of purchasing strategies, forward contracts, and localized sourcing.

Inflation and input cost indices: Producer‑price measures specific to conveyor and bulk material handling manufacturing remain elevated, signaling persistent cost pressure on finished goods unless efficiency or pass‑through mechanisms are enacted.

Investment drivers: Continued capex in ports, cement, and mining — especially in select growth corridors — sustains demand; however, procurement patterns are increasingly influenced by lifecycle cost considerations rather than first‑cost decisions alone.

Technology adoption: Recent product integrations and market intelligence (e.g., sensorized "smart idlers" and advances in corrosion‑resistant coatings) are accelerating a shift where uptime guarantees and predictive maintenance capabilities become differentiators.

The sector remains a mix of well‑established global suppliers and regionally focused manufacturers. Market concentration is moderate — our analysis indicates top three players account for a meaningful but not dominant share of global revenue, and the top five expand that footprint further, leaving room for niche players and acquisition‑driven scale plays. Key companies profiled in the report include global manufacturers and integrators recognized for heavy‑duty rollers and system solutions, as well as regional suppliers that compete on price, lead times and standards compliance.

Global integrators and OEMs — firms with broad conveyor portfolios and international footprints emphasize durability, low‑maintenance designs and systems integration capabilities for mining and port operators.

Regional specialists — manufacturers positioned around domestic supply chains and standards compliance offer competitive lead times and tailored product lines to local markets.

Aftermarket and services players — companies expanding into condition monitoring, predictive maintenance, and retrofit offerings are capturing higher lifetime value per installation.

Advances in self‑lubricating bearing technologies and next‑generation coatings have been reported to materially extend service life in abrasive mining contexts. These technologies change capex vs. opex tradeoffs and create retrofit markets for idler upgrades.

Sensorization and real‑time monitoring solutions are transitioning from pilots to commercial rollouts; smart idler launches and integrated monitoring stacks enable predictive service contracts and new recurring revenue models for OEMs and service providers.

Hedge input risk: establish multi‑layered procurement strategies (forward contracts, diversified suppliers, regional sourcing) and model pass‑through clauses in long‑term contracts to mitigate steel price volatility.

Monetize reliability: pilot premium idler packages (coatings + bearings + monitoring) with selected customers to validate willingness to pay for reduced downtime and lower total cost of ownership.

Expand aftermarket services: invest in condition monitoring capabilities and service logistics to capture higher margins and lengthen customer relationships.

Selective capacity expansion: use the 4.5% CAGR base case to prioritize investments in flexible, modular capacity that can scale with pockets of regional demand rather than broad, fixed expansions.

Pursue tuck‑ins: identify regional specialists and service providers as acquisition targets to accelerate market access and aftermarket capabilities in geographies where lead times and local content matter.

Adopt product modularity: design families of idlers that share components across diameters, bearing types and sealing options to reduce SKU proliferation and improve inventory turns.

Build data monetization pilots: if deploying sensorized idlers, structure pilots to test subscription pricing and predictive maintenance SLAs that can scale beyond single contracts.

Stress‑test contracts: revise warranty and liability language to reflect evolving failure modes driven by salt‑water, abrasive environments and increased throughput demands.

Scenario‑ready models: our downloadable model allows executives to run sensitivity analyses on commodity shocks, capex postponements, and accelerated technology adoption to produce board‑grade forecasts within hours.

Negotiation playbooks: procurement teams receive benchmarked RFP language and a risk scoring matrix for supplier selection in capital procurement exercises.

M&A diligence kits: a condensed checklist and valuation adjustment framework tailored to the idler roller and conveyor components space to speed transaction timelines and reduce integration surprises.

This executive preview is intentionally selective — it surfaces strategic conclusions, headline market sizing, and actionable implications while omitting detailed segment splits, regional percentages and company‑level revenue shares. Those granular datasets, supplier scorecards, and the full suite of appendix materials (including our primary interview transcripts, methodology notes and downloadable forecasting model) are available in the complete PW Consulting Steel Idler Rollers Market report.

For procurement leaders, product strategists and investment teams preparing plans for 2026, this report is designed to convert market intelligence into executable moves. To obtain the full study, proprietary datasets and model access, please contact PW Consulting’s industry research desk or visit our report portal.

PW Consulting continues to track market developments and will issue periodic updates reflecting material changes in raw material pricing, regulatory shifts, and major product rollouts. Our next update cycle will incorporate early 2026 procurement outcomes and any material M&A activity within the sector.

For detailed analysis of this topic, please visit the official page:Steel Idler Rollers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com