Double Base Propellant Market 2026 Strategic Brief — PW Consulting

Executive snapshot

Between 2020 and 2025 the global double base propellant market expanded from approximately USD 485 million to USD 625 million, driven by intensified munitions production, fleet modernisations and targeted capacity investments across Europe and North America. Our base-year (2025) analysis and forward-looking model project the market to reach roughly USD 886 million by 2032, representing a compound annual growth rate (CAGR) of 5.1% over the 2026–2032 forecast window. Market concentration is moderate: the top three firms account for roughly 43% of supply while the top five approach six-in-ten market share — a structure that permits both incumbent scale advantages and opportunities for specialist entrants.

Double Base Propellant Market

Why this report matters for 2026 decision-makers

- Procurement officers need a short‑to‑medium term demand map to time contract awards and buffer inventories against geopolitical surges.

- Manufacturers and investors require a prioritized view of where to deploy capital — expansion, retrofit or green‑field — to capture the next wave of demand with acceptable ROI timelines.

- Policy-makers and defence planners need a supply‑chain risk profile that integrates raw‑material dependencies (notably nitrocellulose and nitroglycerin), compliance obligations and industrial base resilience measures.

Macro drivers and directional trends

- Defence replenishment and ammunition modernisation remain the principal demand engines. Posture shifts and readiness programs sustained elevated output through 2025 and underpin our 2026 baseline assumptions.

- Product technology bifurcation: solventless, high‑caloric formulations optimized for large‑calibre applications are maturing in parallel with extruded and elastomerically modified chemistries tailored for performance and handling. These technology pathways create distinct investment and qualification profiles for manufacturers and users.

- Supply‑chain concentration of critical feedstocks is a strategic vulnerability. Nitrocellulose supply — derived from cotton linters or pulp — and nitroglycerin feedstock logistics are decisive determinants of production continuity and unit economics.

- Regulatory overlay and quality standards (including ISO 9001:2015 and military AQAP certifications) materially affect time‑to‑market for new capacity and create non‑trivial barriers for entrants seeking military qualification.

- Commercial dynamics: a measured wave of capacity expansions and strategic collaborations announced across 2024–2025 will shape regional self‑sufficiency and sourcing options in the next 24 months.

Recent industry moves that shape 2026 strategic choices

- Nitrochemie’s Aschau site expanded production substantially and continued infrastructure build‑out into mid‑2025, improving European supply headroom for key tank and artillery propellant programs.

- Collaborations linking Nitrochemie technology with U.S. systems integrators aim to accelerate domestic energetics capability — an important dynamic for firms evaluating U.S. market entry or partnership strategies.

- New joint ventures in Eastern Europe were launched to establish modular propellant and powder production closer to demand centers — a trend that both reduces transportation exposure and changes regional competitive positioning.

Competitive landscape — what incumbents and challengers mean for buyers

The market is populated by a mix of vertically integrated defence suppliers, specialised energetic manufacturers and turnkey plant providers. Each archetype implies different procurement levers and counterparty risks.

Double Base Propellant Market

- Chemring Energetics UK (UK): a well‑established producer of extruded double base propellants, with a track record in ejection systems and rocket motor propulsive charges. Strengths: defence pedigree and qualification heritage; considerations: capacity scale relative to peak surge demand.

- Nitrochemie (Rheinmetall/RUAG JV footprint in Switzerland and Germany): leading in solventless, high‑caloric double base technologies often specified for large calibre platforms. Strengths: advanced solventless production and integrated nitrocellulose sourcing; considerations: strategic partnerships and export controls influencing international rollout.

- Explosia a.s. (Czech Republic): government‑owned producer with broad product form capability across small and large calibre powders. Strengths: government backing and manufacturing versatility; considerations: market access and commercial pricing models outside core state contracts.

- EURENCO (France): diversified manufacturer producing a wide range of double base forms for multiple applications, including industrial tools. Strengths: product breadth and European footprint; considerations: portfolio optimisation in the face of demand cycles.

- Orbitala and MB Namenska: regional specialists supplying calibres and rocket propellants with strong technical dossiers for specific programmes. Strengths: niche capability and data‑sheeted products; considerations: scaling beyond niche volume contracts.

- D&M Holding Company: turnkey plant supplier for spherical double base manufacture, enabling rapid capacity builds for countries and companies seeking local production. Strengths: technology transfer and EPC delivery; considerations: integration and qualification timelines for military customers.

- General Dynamics Ordnance and Tactical Systems & BAE Systems: larger defence primes with energetic production lines or historical propellant programmes. Strengths: systems integration and procurement relationships with armed forces; considerations: focus may be programme‑driven rather than commodity supply.

What PW Consulting’s Double Base Propellant report delivers (practical, actionable content)

Our research is framed to support procurement, manufacturing and corporate strategy through a combination of data, diagnostics and executable playbooks. The core deliverables include:

Double Base Propellant Market

- Demand scenarios (short, medium and stress paths) calibrated to inventory burn rates, mobilisation timelines and contingency production assumptions.

- Forward revenue and volume model (2026–2032) with sensitivity levers for surge events, qualification lead times and feedstock disruptions — presented at aggregate and product‑class levels.

- Supplier risk matrix and counterparty scoring (capacity, certifications, technological depth, geopolitical exposure).

- CapEx and OpEx benchmarks for expansion, retrofit and green‑field lines (including solventless vs. solvent‑based technology comparisons).

- Regulatory and compliance checklist that maps export control constraints to commercial routing options and certification paths (ISO/AQAP alignment).

- M&A and partnership playbook: target screening criteria, valuation multipliers for strategic assets, integration and qualification timelines.

- Procurement toolkit: recommended contract structures, staged acceptance and qualification milestones, and inventory hedging strategies.

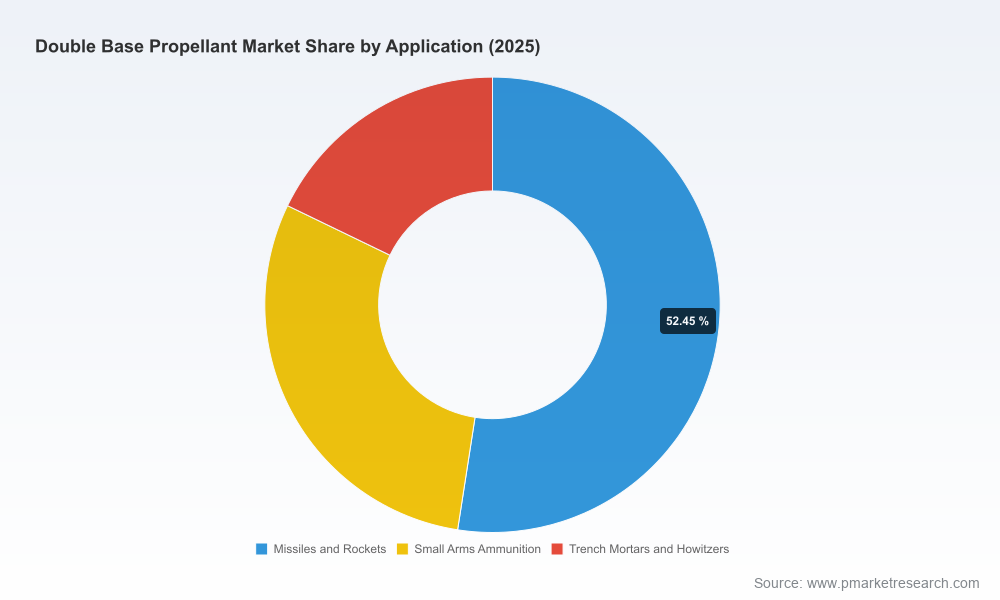

Note: this release intentionally avoids disclosing granular segment‑level tables and split‑out monetary allocations. The detailed breakdowns by region, product type and application — and the underlying spreadsheets used to generate our scenarios — are included in the full report.

Strategic recommendations for 2026

- For sovereign buyers: accelerate supplier qualification pipelines today. Lead times for military‑grade qualification remain the dominant gating factor for near‑term supply resilience.

- For manufacturers: prioritise investments that shorten qualification cycles (e.g., partnering with established test houses, securing feedstock offtakes) rather than pure capacity expansion unless long‑term contracts are secured.

- For investors and private industry: evaluate turnkey EPC providers to capture entry points in regions seeking on‑shore production, but price in the multi‑quarter validation and certification window before commercial revenues.

- For OEMs and prime contractors: hedge technology exposure by maintaining relationships across both solventless and extruded propellant suppliers — product performance demands will vary by platform and mission profile.

- Across the board: embed supply‑chain diversification for nitrocellulose and nitroglycerin sources into five‑year sourcing plans, and incorporate export control scenarios into contract clauses and logistics planning.

Methodology and data integrity

This briefing is built on PW Consulting’s proprietary model: historical baseline 2020–2025, base year 2025, and a 2026–2032 forecast horizon. Our estimates synthesise primary interviews, company disclosures, customs and trade flows, plant capacity statements, and validated open‑source intelligence. We apply scenario stress‑testing for surge demands and feedstock interruptions and reconcile outputs with observed capacity expansions and announced collaborations.

Conclusion — the strategic value proposition

In 2026, decision windows will be narrow. The choices made this year around supplier qualification, capacity partnerships, technology investments and feedstock security will set the operating envelope for much of the next decade. PW Consulting’s Double Base Propellant Market report provides a practical, decision‑ready toolkit: a defensible market size trajectory, scenario‑based risk quantification, and the procurement and M&A playbooks necessary to act with confidence. Our findings show a market that is neither a pure commodity race to the bottom nor an exclusive oligopoly; it is a strategically important, technically demanding industrial space where timing, certification and supply‑chain strategy confer disproportionate advantage.

Accessing the full intelligence

The full report contains the detailed segment tables, supplier scorecards, download‑ready financial models and case studies omitted from this public summary. Organisations seeking the complete analytical package and spreadsheets can access the report and supporting tools via PW Consulting’s market intelligence portal.

For detailed analysis of this topic, please visit the official page:Double Base Propellant Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com