Paper Core Market: Size, Share, and Future Growth

Other |

2026-04-17 03:48:22

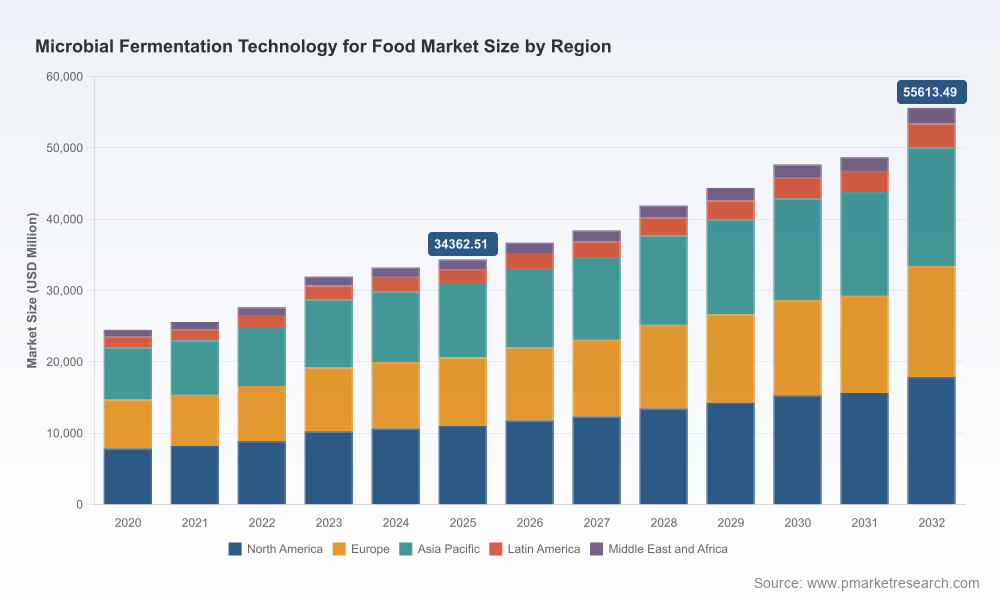

PW Consulting’s latest market research, anchored on a 2025 base year and extending through a 2026–2032 forecast horizon, provides a forward-looking, actionable playbook for senior leaders planning investments, partnerships, and product roadmaps in fermentation-enabled foods. Our modelling shows the total market expanding at a steady compound annual growth rate (CAGR) of 7.12%, rising from roughly USD 24.5 billion in 2020 to about USD 34.4 billion in 2025 and projected to exceed USD 55.6 billion by 2032. These macro dynamics create a distinct inflection window for 2026 strategy: scale or be outflanked.

Microbial Fermentation Technology For Food Market

Actionable timing guidance — we translate demand and technology adoption curves into prioritized windows for capex and partnership moves that align with commercial scale inflection points during 2026–2028.

Microbial Fermentation Technology For Food Market

Risk-calibrated ROI — the research packages techno-economic models with sensitivity runs for feedstock volatility, regulatory timelines and production yields so executives can stress-test business cases before committing to plant builds or licensing deals.

Microbial Fermentation Technology For Food Market

Competitive positioning — beyond top-line growth forecasts, we map differentiated routes-to-market for incumbents, ingredient specialists and precision-fermentation entrants to help executives choose defensible strategic plays.

Regulatory-readiness framework — the report operationalizes GRAS / novel food pathways and health-claim requirements into program-level timelines and regulatory gating criteria to accelerate time-to-shelf.

The headline CAGR of 7.12% masks important structural drivers. Growth is being sustained by three overlapping forces: rising demand for protein diversification and clean-label ingredients; the industrialization of precision fermentation enabling dairy- and egg-protein analogues; and continued ingredientization of probiotics, enzymes and organic acids across processed food categories. For investors and operators this translates into a layered opportunity set — from process equipment and scale-up services to end-market product licensing and branded ingredient plays.

Market concentration remains modestly moderate: our concentration analysis shows that the top three players account for roughly one-third of the market, while the top five account for just under half. This structure creates room for both scale-focused consolidation and targeted niche-positioning by agile entrants.

Precision vs. traditional fermentation — companies engineering microbes to produce single proteins or specialty ingredients are moving from lab to pilot and now selective commercial production. Success depends on integrated capabilities spanning strain engineering, downstream purification and formulation matching to food matrices.

Equipment and automation — suppliers of bioreactors, single-use systems and automated platforms are no longer peripheral vendors; they are strategic enablers. Firms investing in modular, scalable fermenter footprints and digital process control capture superior time-to-market and lower scale-up risk.

Manufacturing playbooks — our report codifies common failure modes observed across pilot-to-commercial transitions and provides templates for fermentation yields, DSP (downstream processing) recovery assumptions, and throughput ramp curves that executives can adopt or adapt.

The ecosystem comprises three broad cohorts: established ingredient suppliers and culture houses, process-equipment and automation vendors, and precision-fermentation platform companies. Each cohort plays distinct but interlocking roles in the value chain.

Ingredient and culture incumbents (examples in our profiles): firms with long histories in yeast, bacterial starters and enzyme portfolios are leveraging scale, distribution networks and formulation know-how to defend shelf-facing customers. Recent sector consolidation has accelerated their move into adjacent capabilities.

Platform and equipment providers: manufacturers of fermenters and single-use bioprocess systems are extending offerings with process validation, digital twins and manufacturing-as-a-service to help food companies de-risk scale-up.

Precision-fermentation pioneers: cell-programming companies and dedicated protein producers are focused on high-value, animal-protein analogues and specialty functional ingredients — their commercial traction will depend on cost curves and regulatory acceptance over the next 12–36 months.

Notable recent strategic moves illustrate the competitive choreography: multi-party mergers have recomposed product portfolios and broadened market reach, while targeted greenfield expansions have increased capacity where demand is accelerating. Our company profiles synthesize these movements into scenario-based competitive maps that executives can use to assess partners, suppliers and acquisition targets.

Regulatory pathways are a gating factor. In the United States, microbial strains intended for food use typically require GRAS notification or equivalent affirmation; in the EU, many precision-fermented products fall under the Novel Foods Regulation and are subject to defined authorization pathways. Health-claim substantiation for probiotic benefits follows stringent regional science standards.

Raw material sensitivity is real: sugar and other fermentable carbon sources remain significant contributors to media cost. Historical volatility — for example, a cyclical uptick that pushed sugar prices to levels averaging 23.5 cents per pound in 2023 — highlights the need for feedstock hedging strategies and media-optimization investments.

Production geography matters. A concentrated yeast-production base in certain countries creates both advantages (cost leadership) and risks (supply-chain exposure) that must be reflected in contingency plans and multi-sourcing strategies.

Designed as a working document for executives planning 12–36 month moves, the full report combines strategic narrative with executable tools. Highlights include:

Market sizing and demand scenarios with three adoption pathways and sensitivity testing for feedstock and yield assumptions (interactive dashboards available in the full deliverable).

Commercialization playbooks that convert lab metrics into plant-specification requirements, capital budgets and ramp timetables.

Vendor and partner assessment frameworks: objective scoring templates for equipment suppliers, CDMOs and ingredient licensors.

Regulatory roadmaps: step-by-step timelines and evidence packages for GRAS/novel-food filings and health-claim substantiation across major markets.

Investment models and valuation multiples for M&A and JV planning, plus an M&A pipeline tracker that surfaces likely consolidation targets based on capability, geography and scale.

Risk heatmaps and contingency plans for supply-chain disruptions, input-cost surges and regulatory delays.

Company dossiers and competitive scenarios covering incumbent culture houses, equipment vendors, and precision-fermentation startups — including merger and expansion impacts and potential strategic responses.

CEOs and corporate strategists: use the report’s scenario outputs to sequence capex decisions and prioritize cross-border manufacturing footprints that balance cost efficiency with regulatory access.

R&D leaders: adopt the pilot-to-commercial templates to set milestone-based gating criteria, reducing technology transfer failures and accelerating product readiness.

Supply chain and procurement heads: implement the supplier risk matrix and feedstock-hedging playbooks to stabilize gross margins under commodity volatility.

Corporate development and investors: leverage the valuation benchmarks and M&A pipeline tracker to identify mispriced assets and execute bolt-on acquisitions or strategic minority investments ahead of expected consolidation waves.

Our competitive review pairs incumbent capability with recent strategic moves to indicate where each player sits on the value curve: culture and starter suppliers have broadened portfolios through M&A and expansions to protect formulation linkages; equipment OEMs are monetizing digital and service layers; and precision-fermentation companies are shifting emphasis from proof-of-concept to cost-parity roadmaps. Recent observable events — completed mergers and facility expansions by leading players — have reinforced market momentum and are synthesized into actionable supplier-selection advice in the full report.

In keeping with PW Consulting’s “preview and power” approach, this release intentionally surfaces strategic findings and practical implications while withholding granular segment-level splits and proprietary interactive dashboards. Those detailed regional, product-type and application breakdowns — alongside the full set of financial models, plant-capex benchmarks and company-specific valuations — are available in the full report and companion data pack.

For executives preparing 2026 budgets and strategic roadmaps, the full deliverable is the difference between speculative planning and precision execution. To access the complete study, interactive dashboards and bespoke consulting options, visit PW Consulting’s Microbial Fermentation Technology for Food Market report landing page or contact our advisory team to schedule a briefing and tailored scenario walkthrough.

For detailed analysis of this topic, please visit the official page:Microbial Fermentation Technology For Food Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com