Magnesia Partially Stabilized Zirconia (Mg-PSZ) Market: Strategic Outlook for 2026 — PW Consulting Intelligence Brief

Executive summary

PW Consulting’s newest market research brief on Magnesia Partially Stabilized Zirconia (Mg-PSZ) distils five years of market observation and a seven-year forecast into an operational guide for 2026 decision-making. The Mg-PSZ market recorded steady expansion through 2025, reaching an estimated USD 219.0 Million (base year 2025). Under our central scenario the market is projected to grow at a CAGR of 5.45% across 2026–2032, reaching roughly USD 317.5 Million by 2032. These headline dynamics frame an industry with resilient end‑use demand, defined technology leadership pockets, and an upstream raw-material environment that requires active management by manufacturers, buyers, and investors.

Magnesia Partially Stabilized Zirconia Market

Why this brief matters for 2026 planning

Mg-PSZ occupies a strategic niche across severe‑service industrial equipment, specialty tooling, and select high‑temperature applications. As supply chains normalize post‑macro disruptions and as regulatory and standards activity reasserts application‑level quality requirements, 2026 will be a year in which product strategy, sourcing resilience, and targeted commercial plays determine leadership. This brief does not merely recount market growth — it translates the trajectory into tactical choices:

Magnesia Partially Stabilized Zirconia Market

- Prioritization frameworks for product portfolios under different demand scenarios;

- Supplier risk matrices driven by upstream zircon feedstock dynamics;

- Commercial playbooks for premiumization versus volume strategies in mature industrial segments;

- CapEx timing guidance tied to manufacturing scale and precision ceramic finishing capabilities.

What the report contains — practical, operational intelligence

The published study goes beyond conventional market sizing. It is built as a working tool for executives and strategy teams, and contains:

Magnesia Partially Stabilized Zirconia Market

- Market architecture and competitive scoring: structured vendor profiles, capability heatmaps, and supplier reliability scoring that inform make‑vs‑buy decisions;

- Demand-by-application scenarios (illustrative and sensitivity-tested) that map to real industrial buying cycles and capital replacement timelines;

- Raw-material and cost pass‑through models, including short- and medium‑term scenarios for zircon feedstock availability and pricing impacts on margins;

- M&A and partnership opportunity map highlighting where scale, specialty capability, or geographic presence buys defensible advantage;

- Regulatory and standards impact analysis, identifying product upgrades and certification pathways necessary for medical and critical industrial uses;

- Actionable KPIs and early-warning indicators designed to be monitored across procurement, sales, and operations dashboards in 2026.

Core market dynamics to monitor in 2026

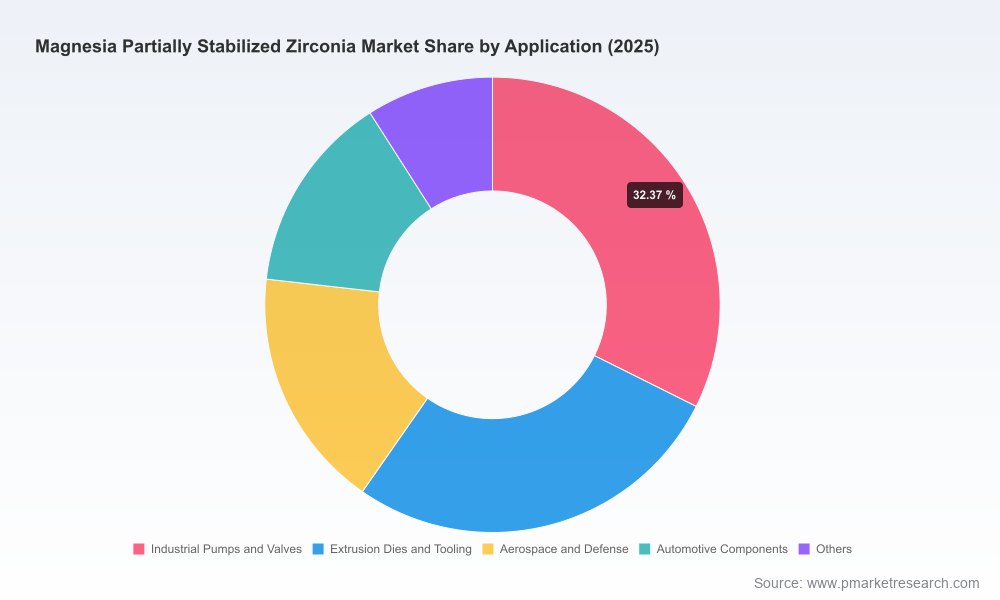

The market’s growth profile is underpinned by demand durability in heavy‑duty pumps, valves, extrusion tooling, and high‑temperature crucibles, paired with incremental adoption in aerospace and specialized automotive components. Key dynamics to track in 2026 include:

- Upstream zircon feedstock posture: premium grade zircon prices stabilized around historical levels through 2025, but industry reporting flags a potential medium‑term supply deficit beyond 2026 driven by maturation and decline of several large mines. Procurement strategies that lock pricing and alternate sources will matter materially;

- Concentration and supply resilience: manufacturing capacity for Mg-PSZ is concentrated among a relatively small group of global producers. This fosters technical leadership but increases vulnerability to single‑region disruptions;

- Standards and regulatory attention: the reapproval of a high‑purity Mg-PSZ specification for surgical implant use reinforces a pathway for premium applications, but it also raises the bar for entry and liability exposure for suppliers targeting medical markets;

- Technology and materials innovation: advances in microstructure control and transformation‑toughening have created product differentiation opportunities — from superior thermal shock resistance to dramatically improved fatigue life under cyclic loading.

Competitive landscape — how the leaders are positioned

The Mg-PSZ competitive set is characterized by technical differentiation, IP around compositions and processing, and a mix of global players and regional specialists. The following company snapshots summarize strategic positioning and what it implies for counterparties and investors:

- CoorsTek (United States) — Known for Dura‑Z™ Mg‑PSZ, CoorsTek competes on product robustness for severe‑service applications (valves, pump internals). For OEMs, CoorsTek represents a low‑risk supplier for critical parts where long service life and corrosion resistance are required. Strategic implication: partnership or long‑term supply contracts reduce field failure exposure.

- Morgan Advanced Materials (Nilcra® Zirconia) (United Kingdom / Australia ops) — Morgan’s Nilcra® range, including highest‑toughness and thermal‑shock variants, targets markets replacing metals and carbides in mining, oil & gas, and materials‑handling equipment. They emphasize Weibull reliability metrics; for end‑users this translates into predictable life‑cycle cost reductions. Strategic implication: bidders for large mining or oilfield contracts should model Nilcra® reliability premium into total‑cost estimates.

- Refractron Technologies (United States) — With proprietary Izory®HD compositions and US‑based precision grinding, Refractron positions itself around quality and supply‑chain resilience. For buyers requiring domestic sourcing or precision tolerances, Refractron is a natural fit. Strategic implication: onshore supply agreements for mission‑critical parts can be negotiated as part of resilience strategies.

- Superior Technical Ceramics (STC) (United States) — STC focuses on transformation‑toughened MSZ variants for high‑temperature and down‑hole applications and supplies solutions compatible with ceramic‑to‑metal assemblies. Strategic implication: STC is a candidate supplier for hybrid assemblies where mechanical joining and thermal expansion compatibility are critical.

- C‑Mac International LLC (United States) — Emphasizes valve and pump components with cyclic fatigue resistance. Strategic implication: OEMs in fluids handling should evaluate C‑Mac for retrofit programs where cyclic loading is the failure mode of concern.

- Zircoa Inc. (United States) — Specializes in tailored compositions and high‑temperature crucibles (e.g., compositions designed for PGM melting). Recent product application updates highlight 1850°C capabilities for PGM recycling. Strategic implication: recyclers and metallurgical processors can reduce furnace downtime and erosion‑related maintenance by trialing specialized crucibles.

- Bangalore Ceramics (India) — A regional custom‑forming supplier, useful for cost‑competitive or bespoke shapes in Asia. Strategic implication: cost and lead‑time arbitrage for non‑critical parts, with qualification needed for highly regulated end uses.

Recent industry developments with strategic consequences

- Zircoa’s early‑2026 publication on high‑temperature crucible compositions signals a fast‑growing niche in metal recycling and PGM processing where thermal shock and erosion resistance materially improve furnace throughput and yield.

- Product catalog releases from specialty ceramic houses in 2025 expanded the thermal and chemical stability palette, making Mg‑PSZ a credible alternative to alumina in select process environments.

- ASTM’s reapproval of a high‑purity Mg‑PSZ specification for surgical implants formalizes medical pathways but also creates a compliance hurdle for suppliers; expected consequence is consolidation among suppliers capable of meeting medical‑grade traceability and QA systems.

Risks, triggers and 2026 action checklist

For executives preparing budgets and strategic initiatives in 2026, the brief identifies a compact set of levers and monitoring triggers:

- Supply‑chain hedging: negotiate multi‑year agreements with staged price review clauses; qualify at least two suppliers across different supply regions to mitigate mine‑level concentration risk.

- Portfolio prioritization: allocate R&D and commercial resources to product families that benefit most from Mg‑PSZ’s distinct properties (wear resistance, thermal shock tolerance, fatigue life) rather than chasing volume in highly commoditized subsegments.

- Certification and regulatory readiness: if pursuing medical or aerospace opportunities, budget for extended qualification timelines and traceability investments driven by standards reapprovals.

- M&A and partnership scouting: target bolt‑on acquisitions that add finishing and grinding precision or unique compositions, rather than broad capacity expansion alone.

- KPIs to monitor monthly in 2026: zircon feedstock availability and lead times, supplier on‑time delivery and defect rates, order backlog trends by end‑use, and margin spread versus raw‑material cost movements.

Methodology, scope and data integrity

The study uses a blended methodology: bottom‑up equipment and parts demand modelling, supplier revenue triangulation, primary interviews with OEMs and suppliers, and secondary data from trade sources and standards bodies. Scope covers historical analysis (2020–2025) and forecasts to 2032 (forecast period 2026–2032). All monetary values are reported in USD Million and the study’s base year is 2025. Scenario modelling incorporates alternative zircon supply paths and differing commercial adoption rates across industrial verticals.

How PW Consulting readers should use this brief in 2026

Use this brief as the strategic spine of 2026 planning cycles: incorporate the KPIs into monthly business reviews, use the supplier scoring to prioritize qualification programs, and align R&D sprints to the product families where Mg‑PSZ’s material advantages convert into pricing power. For corporate development teams, the report’s M&A heatmap and value‑creation levers provide a focused short list for fast diligence.

Next steps — where to get the full intelligence

This press overview is intentionally high‑signal and selective. The full PW Consulting Magnesia Partially Stabilized Zirconia Market report contains the granular segmentation, supplier scorecards, price‑curve models, and excel‑based scenario tools that operational teams and investors need to execute in 2026. To access detailed tables, supplier‑level benchmarks, and our downloadable scenario workbook, please visit the PW Consulting report page or contact our industry desk to arrange a briefing and data licence.

For detailed analysis of this topic, please visit the official page:Magnesia Partially Stabilized Zirconia Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com