Rising Investments in Cell Therapy Fuel Cell Dissociation Market Demand

Health |

2026-06-03 15:10:31

PW Consulting is pleased to release an executive briefing derived from our definitive market research on UV and blue light blocking materials. This industry is entering a consequential phase: regulatory tightening, accelerating adoption across optics and electronics, and raw material volatility are converging to reshape supplier economics and customer buying patterns. Our full 2026–2032 forecast offers the empirical foundation senior executives need to convert uncertainty into competitive advantage. Below we summarize the strategic implications and the practical intelligence that will matter for capital allocation, M&A, and product strategy in 2026 — while preserving the report’s proprietary segment-level detail to ensure readers visit our source page for the complete dataset.

UV and Blue Light Blocking Material Market

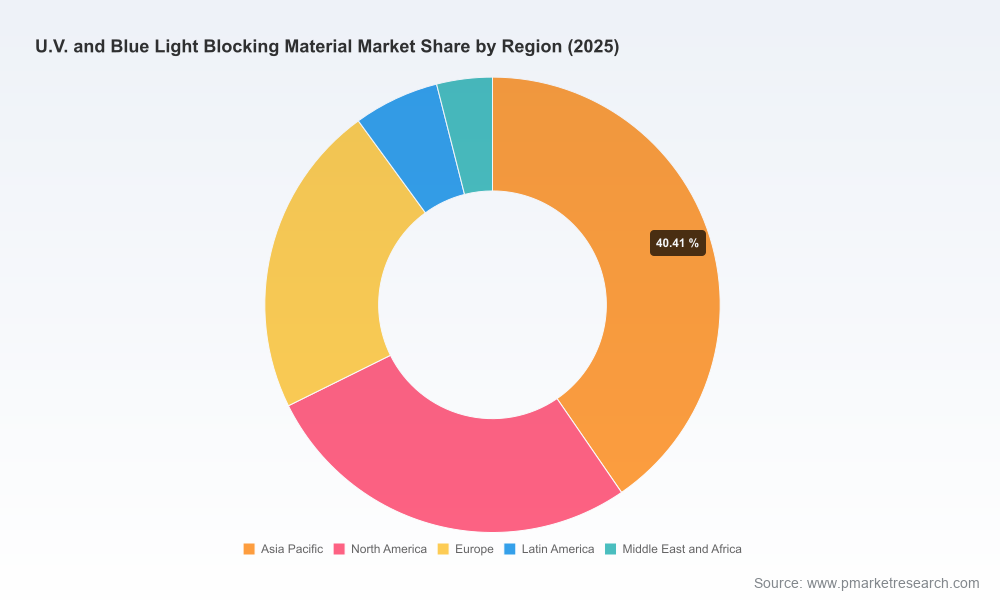

The UV and blue light blocking materials market has demonstrated robust growth over the past half-decade, expanding from approximately USD 2.5 billion in 2020 to roughly USD 3.83 billion in 2025. Our forecast projects compound annual growth of 8.92% across the 2026–2032 horizon, with the market approaching nearly USD 7.0 billion by 2032. That trajectory is underpinned by three structural drivers: (1) growing demand for eye protection and display performance in consumer electronics and eyewear, (2) architectural and automotive glazing requirements for solar control, and (3) expanding use of specialty additives and engineered polymers across medical and optical applications.

UV and Blue Light Blocking Material Market

Regulatory momentum has become the dominant near-term risk and opportunity vector. In mid-2025, the European Commission moved to restrict a widely used benzotriazole-based UV absorber under persistent organic pollutant (POP) controls, setting staged unintentional trace contaminant limits. The change forces immediate reassessment of raw-material qualification, especially for polymers and coated articles destined for EU markets. Simultaneously, certain jurisdictions are offering temporary exemptions or transition pathways, creating a patchwork of compliance obligations that complicates global product launches.

UV and Blue Light Blocking Material Market

For product and regulatory leaders, the 2026 imperative is simple: implement a compliance-first product architecture. That means:

Companies that treat compliance as a strategic enabler — rather than an operational tax — will accelerate market share gains during the transition window.

The competitive set blends global specialty-chemical incumbents, regional masters of formulation, and fast-following local producers. Key players we profile in the report include established conglomerates with deep additive portfolios and nimble regional suppliers that compete on processability and cost-to-serve.

Our company profiles in the full report highlight product families, go-to-market orientations, and partnership footprints for the leading firms. This analysis is built to support supplier selection, alliance-building, and due-diligence processes in 2026.

The market is segmented by material class (base polymers, engineered resins, and chemical absorbers/coatings), application (eyewear, displays, architectural glazing, medical), and geography. Each segment exhibits distinct growth rates, margin characteristics, and regulatory exposure. The full report contains granular revenue and growth matrices by segment and channel — withheld here to preserve the integrity of our client-grade datasets. If you are evaluating product prioritization, pricing frameworks, or distribution strategies, the report’s segment-level outputs will be the primary input to your 2026 operating plan.

PW Consulting’s market study is designed to be immediately operational for executives planning 2026 activities. Key actionable elements include:

Based on our analysis, companies should prioritize the following actions in 2026 to convert market dynamics into defensible growth:

The complete PW Consulting report contains the full quantitative backbone to support the recommendations above: detailed historicals (2020–2025), the 2026 base year calibration, and scenario-driven forecasts to 2032 presented in USD (million). It also includes the full competitive benchmarking, proprietary supplier scoring, and downloadable data tables for use in financial models and board materials. To preserve research integrity and to guide strategic engagement, we present a high-level briefing here and reserve the granular segment and regional splits for report subscribers and clients.

Executives preparing 2026 budgets should use the following sequence to operationalize the research:

PW Consulting’s market study is expressly structured to accelerate those steps with executable templates and validated assumptions. For procurement leads, product chiefs, and corporate development teams, the report will serve as the primary north star in 2026 planning cycles.

We invite market participants to engage with PW Consulting to obtain the full dataset, scenario models, and advisory support. The full report contains the detailed segmentation, company profiles, and downloadable financial models referenced above — information critical to make confident, defensible decisions in a rapidly evolving regulatory and commercial environment.

For detailed analysis of this topic, please visit the official page:UV and Blue Light Blocking Material Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com