Technical Ceramic Evolution: Analyzing Key Drivers Steering Global Aluminum Nitride Consumption

Other |

2026-06-15 10:20:18

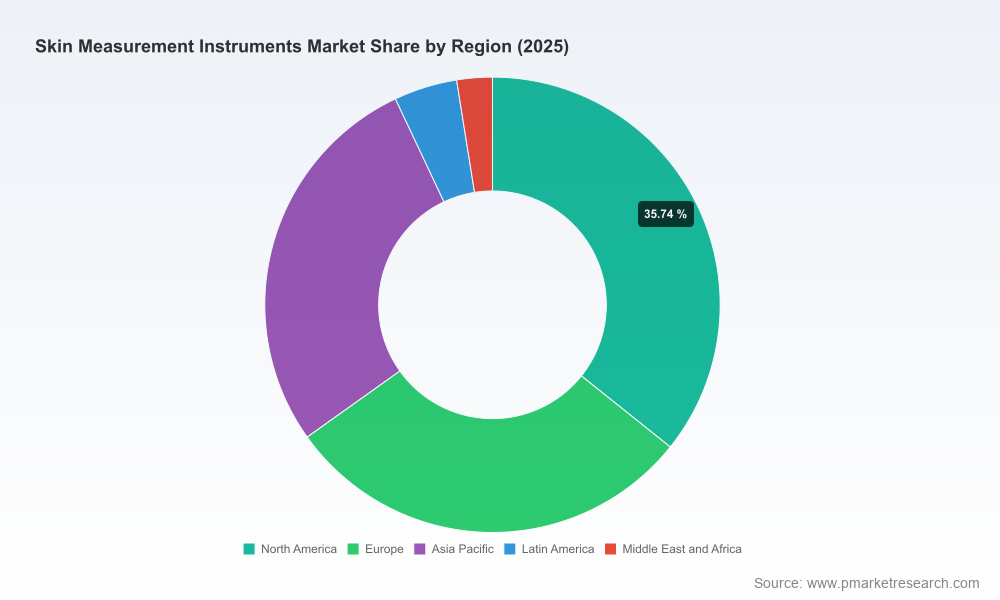

As companies plan capex, product roadmaps, and go-to-market moves for 2026, PW Consulting’s new Skin Measurement Instruments Market study provides an executive-grade synthesis of the forces reshaping an industry that is re-entering a phase of accelerated innovation and commercialisation. The global market has expanded significantly over the past half decade—rising from under USD 700 million in 2020 to just over USD 1.02 billion in 2025—and PW’s base-case forecast projects continued expansion through the 2026–2032 horizon at a compound annual growth rate (CAGR) of 8.24%. This briefing sets out the strategic value of the full report for corporate leaders, investors, and clinical procurement teams while deliberately withholding granular segment-level figures to encourage engagement with the full study.

Skin Measurement Instruments Market

PW’s topline sizing shows the market roughly doubling during the forecast window, with an inflection that reflects a mix of product upgrades (next-generation imaging suites and modular multi-probe platforms), growing adoption in non-traditional channels (retail and personalized beauty consults), and rising clinical utilisation for objective outcome measurement. For executives deciding on 2026 budgets, the implication is clear: investments in modular platforms, software-enabled services, and scalable manufacturing will capture disproportionate upside.

Skin Measurement Instruments Market

The market exhibits moderate concentration: the top three firms account for a meaningful but not dominant share of global revenues, and the top five firms control under half the market—creating space for specialist vendors and regional champions to scale via focused propositions. The full report provides a mapped view of competitive positions, capability matrices, and acquisition targets; below is a high-level synthesis of the incumbent archetypes and illustrative company roles.

Skin Measurement Instruments Market

Representative market participants illustrate these archetypes: long-standing instrument manufacturers renowned for device precision; imaging companies with integrated 3D and AI platforms; portable device specialists with extensive clinical publications; and diagnostic device startups pursuing point-of-care applications. Recent corporate moves—such as the introduction of next-generation 3D/AI imaging platforms and new application notes expanding clinical use cases—underscore the momentum behind platformisation and validation.

Regulatory dynamics are central to 2026 strategy. A significant regulatory milestone in 2026 created a faster pathway for certain optical diagnostic and electrical impedance instruments, enabling broader use of the 510(k) route in the U.S. This change, coupled with targeted reimbursement updates affecting outpatient coding and packaging, reduces time-to-revenue for some device classes and changes procurement calculus for hospitals and clinics.

For product and regulatory teams, the actionable takeaways are:

Our analysis identifies three near-term product strategies that have the highest expected return on investment:

These approaches reduce the dependency on continuous hardware upgrades and create stickier customer relationships—key for market capture during the forecast period.

Sales motion differentiation will be decisive in 2026. The report maps three primary buyer archetypes—clinical procurement (dermatology and hospital outpatient clinics), research and R&D teams (cosmetic and academic), and retail/beauty consultancies—and prescribes tailored commercial strategies for each. Examples of recommended actions include direct enterprise sales and clinical KOL programs for high-touch capital systems, digital trials and partnerships for consumer-facing products, and bundled service offerings for clinics seeking outcome measurement as a differentiator.

Consolidation will be selective rather than sweeping. Strategic buyers are likely to pursue targets that fill one of the following gaps:

Private equity interest typically focuses on companies with recurring revenue potential—platform-based models and consumable-linked instruments rank highly on buyer scorecards.

The complete study is designed for fast use by boardrooms and product teams and includes the following operationally actionable components:

To respect the “trailer” principle that drives qualified engagement, this preview intentionally omits the granular regional and application split figures that buyers and investors typically request when preparing tactical execution plans. The full report contains those segment-level breakdowns, scenario-modeled revenue projections, and a downloadable dataset for internal financial modelling.

The skin measurement instruments market presents a rare combination of scientific defensibility and commercial upside. For organisations that move quickly in 2026—aligning product architecture with regulatory realities, embedding analytics into go-to-market models, and prioritising clinical validation—the window to build sustainable market positions is open. PW Consulting’s full report equips leaders with the data, scenarios, and playbooks needed to convert strategic intent into measurable results.

For access to the complete dataset, segmented forecasts, and the supplier scorecards referenced in this preview, please consult the full PW Consulting Skin Measurement Instruments Market report and datasets on our website.

For detailed analysis of this topic, please visit the official page:Skin Measurement Instruments Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com