Automatic Slack Adjuster Market: Trends and Growth Opportunities

Networking |

2026-03-09 08:44:24

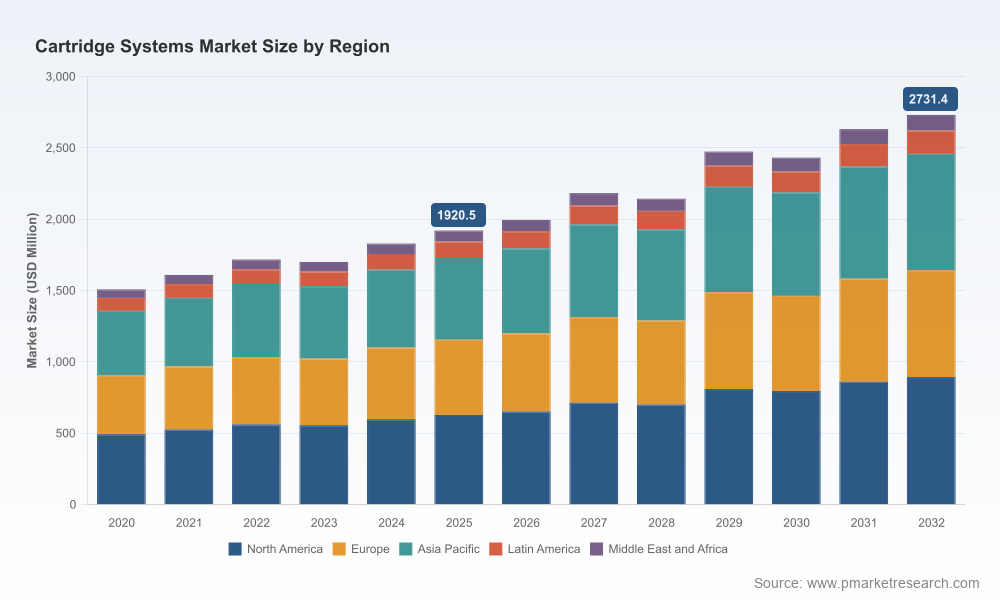

PW Consulting’s latest Cartridge Systems Market report, anchored on a 2025 base year and offering a 2026–2032 forecast horizon, translates industry complexity into actionable guidance for leadership teams preparing strategy for the coming planning cycles. The global cartridge systems market has shown resilient expansion—rising from roughly USD 1.5 billion in 2020 to about USD 1.92 billion in 2025—and is projected to continue growing at a compound annual growth rate (CAGR) of 5.04% through 2032, reaching an estimated USD 2.7+ billion by the end of the forecast window. These headline dynamics mask a rich set of adjacent risks and opportunities; the purpose of this release is to outline the strategic levers executives should prioritize in 2026 while preserving the report’s proprietary segment-level intelligence for subscribers.

Cartridge Systems Market

Evidence-based foresight: The report synthesizes six years of historical performance (2020–2025) with scenario-driven forecasts for 2026–2032. That combination helps finance, commercial, and operations leaders align budgets to realistic demand curves rather than optimistic anecdotes.

Cartridge Systems Market

Risk quantification: We translate raw-material volatility, regulatory shifts and manufacturing capacity constraints into quantified bottom-line scenarios—enabling risk-adjusted capital allocation and more defensible contingency planning.

Cartridge Systems Market

Actionable go-to-market playbooks: For corporates and private equity sponsors considering M&A, vertical integration, or new product launches, the report supplies prioritised target profiles and near-term integration checklists that materially shorten diligence cycles.

The market’s recovery and steady expansion reflect two underlying forces. First, structural demand from healthcare and industrial adhesive applications remains robust as packaging, drug delivery, and assembly processes increasingly rely on precise dispensing and containment. Second, product innovation and sustainability imperatives are reshaping supplier economics and customer sourcing behavior.

Raw-material inflation and regional cost differentials are an immediate strategic concern. The U.S. Producer Price Index for plastics packaging rose materially into early 2026, and commodity resin dynamics remain uneven across regions—polypropylene and HDPE exhibit meaningful price spreads that affect product cost stacks, competitiveness of local manufacturing, and sourcing decisions. These inputs, coupled with intermittent capacity constraints for specialized glass and polymer components, drive margin pressure for manufacturers and influence OEMs’ choices on single-sourcing versus multi-sourcing.

Regulatory and sustainability pressures are converging with commercial incentives. Leading suppliers are launching trials and commercial products that substitute virgin polymers with PCR/PIR streams and paper-based substrates for certain industrial cartridges—moves that have measurable CO₂ benefits while preserving functional performance. This transition is not purely compliance-driven; many customers now demand demonstrable life-cycle benefits as a condition for long-term contracts.

Pharma-focused primary-packaging leaders: Established glass cartridge and parenteral packaging specialists lead on drug-containment credibility, regulatory know-how and high-bar sterility credentials. Their strengths create high barriers for newcomers but also create acquisition and partnership opportunities for companies wanting rapid entry into injectable drug delivery.

Industrial dispensing specialists: Firms that concentrate on adhesives, sealants and automated dispensing systems compete on integration, dispensing accuracy and system-level reliability. Their innovation cadence—especially two-component systems and dispensing hardware—shapes industrial adoption curves in electronics, automotive and construction sub-sectors.

Service and filling-enabled players: Companies offering ready-to-use (RTU) filling lines, integrated sterilization and contract manufacturing for cartridge assembly are becoming strategic partners for OEMs seeking to de-risk capital expenditure and shorten time-to-market.

Consolidation dynamics: Market concentration is moderate; the three-largest firms control a notable share of market value while the top five firms command a substantially larger slice, creating an environment where scale matters for procurement leverage, global footprint and regulatory compliance. Expect continued strategic M&A focused on capabilities (e.g., filling, sustainable-materials expertise) rather than pure volume.

Our competitive analysis profiles leading companies across these archetypes and evaluates their strategic posture, R&D roadmaps, and supply-chain resilience. The profiles identify who is prioritizing pharmaceutical-grade containment, who is accelerating 2K and multi-component system innovation, and where ecosystem partnerships are forming to offer system-level solutions.

Material and circularity experimentation: Large firms are piloting paper-based and recycled-plastic cartridge formats to address scope-3 and customer-level sustainability demands. These launches indicate the next wave of product spec re-definitions that purchasing teams must evaluate for compatibility and long-term cost impact.

Supply-chain signaling: Trade-show initiatives and supplier roadshows in early 2026 focused on nitrocellulose-free inks and sustainable print technologies for packaging, underscoring how adjacent supply-chain actors (inks, labels, secondary packaging) are also part of cartridge system redesigns.

Input-cost realities: Public indices and market monitors show resin prices and packaging producer indices that vary materially by geography—an immediate input to sourcing decisions, hub location economics and hedging strategies for raw-material procurement.

Revisit sourcing architecture now: Running sensitivity analyses across raw-material price scenarios is table stakes. PW Consulting’s model lets procurement leaders stress-test single-supplier contracts, localize critical node production or adopt hybrid sourcing with option clauses tied to PCR content or freight benchmarks.

Prioritise sustainability with performance guardrails: Evaluate low-carbon material options through side-by-side validation protocols. The goal is to avoid “sustainability tax” surprises—materials that reduce Scope 3 emissions but introduce performance variability or regulatory complexity.

Resolve portfolio trade-offs between standardization and customization: Product families that serve high-regulation pharma markets demand different quality systems and capital intensity versus industrial dispensing platforms. Align product investments with target margin profiles and partner ecosystems.

Implications for M&A and partnerships: Acquirers should prioritize bolt-on capabilities—RTU filling, recycled-content injection molding, or precision dispensing hardware—over purely volumetric scale. Our report ranks capability gaps against strategic buyer archetypes to accelerate M&A screening.

Embed regulatory foresight into R&D roadmaps: Anticipatory testing for material-drug interactions, sterilization compatibility and new environmental labeling standards reduces time-to-certification and avoids costly reformulations.

Proprietary forecast model: Scenario-enabled revenue forecasts to 2032 with sensitivity toggles for input-price shocks, geographic demand shifts and product-mix evolution.

Supply chain maps: Node-level analysis of raw-material supply, critical glass and resin capacity, and logistics choke points with mitigation playbooks.

Commercial playbooks: Go-to-market recommendations by customer segment, pricing levers, warranty and service models, and sample contracting language for long-term supply agreements.

Due-diligence toolkit: Standardised scorecards and integration checklists for evaluating acquisition targets and partnership candidates, with value-creation pathways and typical cost-synergy assumptions.

Competitive dossiers: Strategic profiles of leading suppliers across pharma containment, industrial dispensing and filling/RTU services, highlighting differentiators, recent product launches and likely near-term strategic moves.

For CEOs and GMs: use the executive scenarios to update capital allocation and M&A priorities this quarter. For procurement leaders: use our price-sensitivity matrices to re-scope contracts and secure optionality. For R&D and product teams: prioritize material qualification roadmaps that align with both customer endurance requirements and sustainability targets. For private-equity investors: the report’s target archetypes and valuation frameworks compress diligence timelines and clarify post-acquisition value levers.

Our analysis integrates verified market metrics, supplier interviews, plant-level capacity audits and first-pass cost-models to provide a defensible basis for decisions that will be executed in 2026. We intentionally preserve the report’s most sensitive segmentation tables and line-item forecasts to subscribers: the macro trajectory and strategic implications outlined here are a precise guide to the types of decisions the full dataset will support.

To access the complete dataset, proprietary segment forecasts, and supplier scorecards that underpin these recommendations, consult the full Cartridge Systems Market report available through PW Consulting. Our team is available for briefings and customized workshops to translate the insights into an executable 90-day plan.

For detailed analysis of this topic, please visit the official page:Cartridge Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com