Exhaled Nitric Oxide Detectors Market: Strategic Intelligence for 2026 — PW Consulting Official Release

Executive summary

As health systems and device manufacturers recalibrate their portfolios for the next wave of respiratory diagnostics, our latest Exhaled Nitric Oxide (FeNO) Detectors Market report provides a timely, decision-ready view of the competitive and commercial landscape through 2032. The global FeNO detectors market—anchored by portable and clinic-grade instruments—has moved from niche diagnostic adjunct to an increasingly mainstream biomarker tool, driven by guideline changes, regulatory approvals and pragmatic cost‑of‑care conversations. PW Consulting forecasts robust expansion from the 2025 base year into the forecast horizon (2026–2032) at a compound annual growth rate (CAGR) of 7.42%, reflecting both steady clinical adoption and incremental product innovation.

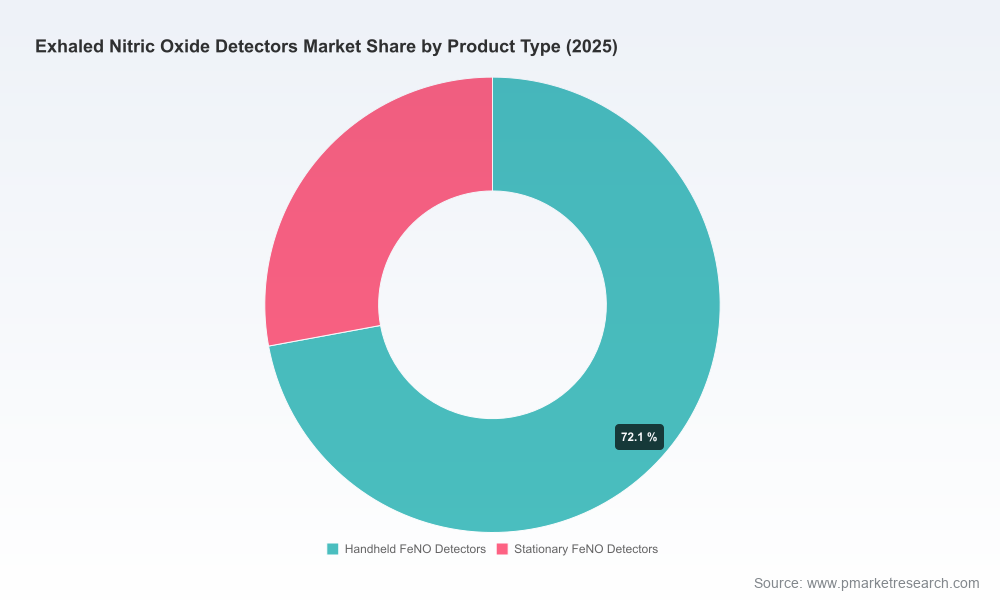

Exhaled Nitric Oxide Detectors Market

Market trajectory and what it means for 2026 planning

Quantitatively, our model shows meaningful growth beyond the 2025 baseline, with the market evolving into a materially larger addressable opportunity by the end of the forecast period. This expansion is not linear; it is punctuated by inflection points tied to regulatory clearances, guideline adoption and device workflow optimizations. For corporate strategists, the implication is clear: 2026 is a pivot year in which investments in distribution, payer engagement and clinical integration will disproportionately influence market share outcomes through 2032.

Exhaled Nitric Oxide Detectors Market

- Growth dynamics: A mid-single-digit to low double-digit growth trajectory (7.42% CAGR) signals steady upside for incumbent manufacturers and late‑stage entrants prepared to invest in evidence generation and reimbursement pathways.

- Timing matters: Recent regulatory and guideline shifts have created a narrow window during which market positioning and clinical partnerships can translate into durable adoption.

- Commercial leverage: Providers are more likely to adopt FeNO testing when devices align with throughput, reimbursement packaging and electronic health record workflows—areas our report quantifies and models for 2026 deployment.

Why 2026 is a strategic inflection point

Several converging factors make 2026 the focal year for boardroom decisions:

Exhaled Nitric Oxide Detectors Market

- Guideline validation: The expanded role for FeNO in diagnosing Type 2 asthma, as reflected in recent guideline updates, reduces clinical adoption barriers and creates a clearer clinical utility narrative for payers and health systems.

- Regulatory momentum: Multiple manufacturers secured or progressed 510(k) clearances in the 2024–2025 window, and further approvals in late 2025 and early 2026 have demonstrably altered competitive positioning and market access strategies.

- Payer and coding dynamics: Reimbursement constructs and the way outpatient bundles are assembled materially influence device economics; consequently, engagement with coding and reimbursement teams must be part of go‑to‑market plans in 2026.

- Concentration and consolidation risk: The market exhibits high concentration among a few leading vendors, amplifying the impact of M&A, distribution partnerships, and exclusive contracts on next‑year share gains.

What the PW Consulting report delivers (practical, action‑oriented)

We designed this research product as an operational playbook for executives and investment committees. The report combines market-sizing, scenario-based forecasts and executable commercial tools—without compromising the proprietary data you’ll need to act.

- Market sizing and validated forecasting models with sensitivity bands across reimbursement, guideline adoption and price erosion scenarios;

- Commercial playbooks for incumbent device manufacturers and new entrants: channel strategies, sales motion archetypes, and provider-targeted value propositions;

- Reimbursement and HTA guidance, including coding strategy templates, payer engagement roadmaps and return-on-investment calculators tailored to hospital outpatient and primary care settings;

- Regulatory and standards matrix: pathway checklists, 510(k) considerations, and conformity to measurement standards that impact clinical acceptance;

- Procurement and tendering playbook for large health systems, with contract negotiation levers and device lifecycle cost analyses;

- Supply chain and manufacturing risk matrix with mitigation measures for component concentration and cross‑border logistics;

- Competitive landscape and M&A playbook: profiles, strategic options, and valuation drivers that matter to buyers and sellers.

Note: As part of our “trailer” approach, this release intentionally omits the report’s granular segment tables and exact regional/application revenue splits. The full dataset and downloadable model are accessible via our report webpage.

Competitive landscape: leaders, challengers and tactical lessons

The competitive picture is defined by a mix of established medtech firms, specialist diagnostics companies and regional manufacturers. Market concentration metrics indicate that the top three vendors control a significant share of revenue, with the top five capturing an even higher share—an indication that scale, clinical credibility and distribution remain decisive.

- NIOX Group (Circassia): The NIOX VERO® device remains a benchmark for point‑of‑care FeNO testing and benefits from strong guideline recognition and standards conformity. Their positioning in clinical pathways and brand recognition with pulmonologists creates high barriers to displacement, particularly in institutional accounts.

- Bedfont Scientific: With a reputation for cost-effectiveness and practical device design, Bedfont’s NObreath® continues to appeal in price-sensitive markets and integrated care pathways. Recent publications highlighting improved asthma control strengthen their clinical narrative.

- Bosch Healthcare Solutions: Regulatory momentum—most notably recent 510(k) clearances—has accelerated Bosch’s entry into key markets with its Vivatmo series, shifting competitive dynamics in outpatient and specialty clinic channels.

- MGC Diagnostics (affiliated with CAIRE): The company’s emphasis on workflow efficiencies (notably the shorter breath maneuver approvals) addresses a practical pain point in busy clinical settings and improves throughput economics for buyers.

- ECO MEDICS: As a provider of high‑precision reference analyzers, ECO MEDICS anchors the research and specialty laboratory segment; its devices are widely used for validation and comparative studies.

- Sunvou and YSENMED: Regional players offering cost‑competitive handheld analyzers are accelerating adoption in emerging markets and tiered care settings, influencing pricing dynamics globally.

Recent developments that matter for near‑term strategy

- Regulatory clearances for new portable systems have expanded the pool of clinically acceptable devices, changing procurement calculus and enabling faster roll-out strategies in 2026.

- Guideline updates that explicitly reference FeNO testing as part of Type 2 asthma diagnosis create stronger payer and provider rationales for routine testing, accelerating coverage discussions.

- New clinical evidence and product positioning around workflow efficiency lower adoption friction in primary care and high‑volume outpatient settings.

Strategic recommendations for executives in 2026

PW Consulting’s experience working with device manufacturers, payers and large providers yields a clear set of near‑term priorities:

- Invest selectively in clinical evidence that demonstrates improvement in care pathways and measurable reductions in exacerbation‑related resource use; this is the most direct route to payer acceptance.

- Prioritize interoperability and workflow: devices that integrate with electronic records and minimize testing time will outperform purely price‑led offerings.

- Engage early with payer medical directors and procurement teams; proactively model how FeNO testing can be packaged within outpatient bundles and chronic disease management programs.

- Consider inorganic options where scale or channel breadth is missing—M&A or exclusive distribution agreements can rapidly change market footprints given current concentration dynamics.

- Design tiered product lines and pricing strategies to defend against low‑cost entrants while protecting margins in premium institutional channels.

Risk scenarios and sensitivity

Our forecast explicitly models upside and downside cases tied to three levers:

- Reimbursement pathway changes and how bundled payments are applied in outpatient settings;

- Speed and depth of guideline uptake across markets and specialty groups;

- Market entry of low‑cost portable devices that could compress pricing in certain geographies.

Each scenario is accompanied by tactical responses—ranging from accelerated clinical programs to channel restructuring—so that leaders can convert foresight into executable actions.

Conclusion — why download the full report

For executives setting 2026 priorities, the choice is between incremental, reactive moves and a coordinated commercial pivot that secures share in the next growth phase. PW Consulting’s Exhaled Nitric Oxide Detectors Market report blends robust quantitative forecasting with practical, actionable guidance—spanning reimbursement playbooks, procurement tactics, regulatory checklists and a competitor playbook grounded in the most recent market developments.

To access the full data tables, region/application breakdowns, and our interactive forecast model (including downloadable scenario inputs), please visit the official report page. The detailed segment intelligence and financial models are available exclusively with the full report.

For detailed analysis of this topic, please visit the official page:Exhaled Nitric Oxide Detectors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com