Purified Water Market: Insights, Key Players, and Growth Analysis

Other |

2026-06-19 11:39:07

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I am pleased to introduce our latest market research brief on the Electrical Measurement System market. This preview explains why the full 2026 report will be an indispensable decisioning tool for executives, product leaders, procurement heads, and investors who must navigate an equipment landscape reshaped by rapid electrification, semiconductor turbulence, and shifting trade policy.

Electrical Measurement System Market

Electrical measurement systems—oscilloscopes, multimeters, power analyzers, spectrum analyzers, clamp meters, and their automated test-system cousins—sit at the intersection of three converging trends that define industrial technology strategy in 2026: aggressive electrification across transportation and energy, exponential complexity in high-speed electronics and RF systems, and the proliferation of data-driven asset lifecycle management. Our analysis places the global market at approximately USD 17.45 billion in 2025, with a near-term uptick to around USD 19.16 billion in 2026. A steady compound annual growth rate of roughly 6.0% through 2032 points to durable demand and multiple strategic entry points across product, software and services layers.

Electrical Measurement System Market

Forward-looking market sizing and scenario modeling calibrated to 2026 decision horizons: baseline, supply-constrained, and acceleration scenarios that translate macro drivers into procurement and R&D implications.

Electrical Measurement System Market

Technology trajectory maps that align instrument capability (bandwidth, dynamic range, accuracy, integration) to near-term use cases—EV power validation, high-speed serial compliance, 5G/6G RF verification, and grid edge power quality monitoring.

Component and supply-chain risk heatmaps that fuse semiconductor export controls, raw-material concentration, and realized lead-time shocks into prioritized mitigation actions.

Commercial-playbook modules: product roadmaps, servitization options (calibration-as-a-service, analytics subscriptions), pricing levers, and channel strategies tailored to Tier-1 labs, service fleets, and OEM production floors.

Deal-level intelligence for M&A and partnership scouting—profiled targets by capability (software analytics, calibration networks, automated test platforms) with acquisition rationale and integration risks.

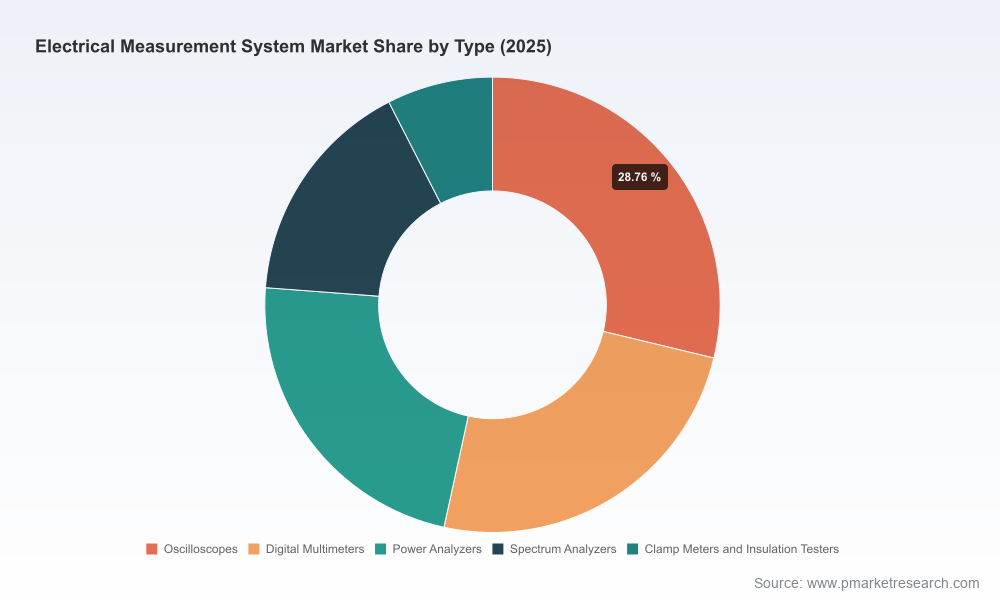

We deliberately present these elements in a hands-on format: executable recommendations, investment thresholds, and time-to-impact estimates. To preserve competitive value, the preview refrains from disclosing line-item regional or application-level shares — the full dataset and drilldowns are available in the premium report.

The market is a mix of R&D-tier leaders, field-service specialists, modular automated-test platforms, and aggressive low-cost entrants. Each archetype implies different strategic imperatives for customers and competitors alike.

R&D and high-performance incumbents (examples include Keysight Technologies, Tektronix, Rohde & Schwarz, Teledyne/LeCroy): these firms continue to invest in high-bandwidth, high-fidelity instruments and integrated software ecosystems. Their strength lies in deep protocol support, instrument accuracy, and validation suites required by semiconductor and advanced wireless customers. Strategic implication: expect premium solutions to expand into software-enabled lifecycle services and to command defense-of-margin investments in calibration automation and remote diagnostics.

Field and service-focused vendors (examples include Fluke, Megger, Hioki): these players dominate reliability, usability, and ruggedization for utility, industrial maintenance, and field service. Their competitive moat is distribution, brand trust, and after-sales support. Strategic implication: opportunities exist to monetize recurring calibration, condition-monitoring subscriptions, and localized service partnerships—especially as field instruments incorporate more intelligence.

Modular automated-test and system integrators (examples include National Instruments / NI, Advantest, Chroma): they are the backbone of production validation and automated functional test. Their roadmaps increasingly prioritize software configurability, higher throughput, and energy-efficiency testing suites aligned to EV and renewable power electronics. Strategic implication: OEMs should evaluate co-development or framework licensing to reduce time-to-market for complex test sequences.

Price-competitive and regionally scaling OEMs (examples include RIGOL, Siglent, GW Instek, B&K Precision): these vendors are compressing feature-to-cost curves and expanding distribution footprints. Strategic implication: incumbents must defend mid-market segments through bundled service offers, while larger customers can leverage competitive bidding to lower TCO for non-differentiated assets.

Recent product activity — from specialty high-resolution insulation testers to micro-precision catalogs — underscores vendor focus on niche capabilities that solve specific reliability and safety needs. Such launches are early indicators of future mainstream requirements in safety-critical electrified systems.

Three supply-side realities are particularly consequential for procurement and product roadmaps:

Raw-material concentration and component scarcity: critical refining capabilities for certain magnet and specialty material inputs remain heavily concentrated in one geography, creating systemic exposure for instrument manufacturers. This concentration amplifies price and availability volatility for critical components and subassemblies.

Semiconductor policy and memory/analog supply pressures: regulatory changes in major markets and AI-driven demand surges have influenced chip pricing and availability. Memory pricing spikes and analog IC lead-time extensions—with some analog parts experiencing multi-month shortages—are increasing the effective lead time for higher-tier instruments and modular test systems.

Logistics and labor-cost shifts: protracted lead times for specific passive and analog components are raising inventory carrying costs and prompting firms to reassess just-in-time assumptions for production and service spares.

Taken together, these factors mean that instrument OEMs and buyers must adopt a risk-aware sourcing posture in 2026: prioritize dual-sourcing, increase strategic inventory for long-lead items, and negotiate supplier commitments that include capacity reservation for critical product lines.

Electrification test suites: power-electronics validation for EV inverters, onboard charging, and bidirectional energy flows is a high-growth pocket. Manufacturers that couple hardware with turnkey test sequences and automation win faster adoption among OEM production teams.

Service and analytics: bundling instruments with cloud-based condition monitoring, predictive maintenance analytics, and calibration subscriptions creates high-margin annuities and improves customer stickiness.

Modular, upgradeable platforms: designing instruments as modular systems that can be field-upgraded mitigates component scarcity and extends installed-base revenue through paid feature unlocks.

Localization and regional manufacturing: selectively locating assembly and calibration can reduce lead-time risk and navigate trade-policy frictions—this is particularly relevant for suppliers serving regulated industries and government customers.

Procurement: implement a differentiated sourcing strategy that categorizes instruments by criticality and sets inventory policy accordingly. For mission-critical R&D and production instruments, secure supplier capacity or pursue managed inventory agreements to avoid single-source exposure.

Product leadership: prioritize modularity and software-driven features. Roadmap at least one major instrument family to support remote diagnostics, feature upgrades, and data-native APIs that integrate with enterprise asset management systems.

M&A and partnerships: favor deals that add software analytics, calibration networks, or regional service footprints. Small, fast acquisitions can accelerate entry into aftersales and recurring-revenue streams.

Risk management: stress-test BOMs against export-control scenarios and rare-material supply interruptions. Build contingency playbooks that include validated second suppliers, cross-qualification of parts, and legally compliant sourcing pathways.

Commercial model: pilot subscription and outcome-based models for field instruments where telemetry enables condition-based billing. This shifts capital expenditure to operational expenditure for customers and supports higher lifetime value for vendors.

Our full Electrical Measurement System Market report provides the operational depth behind the strategic signals above: granular scenario outputs, time-phased supplier risk indices, instrument capability matrices, and commercial-play templates calibrated for 2026 execution. The preview you are reading intentionally omits detailed regional and application-level splits to preserve the proprietary insights that matter most to customers who will act on them.

For leaders who must set budgets, prioritize R&D investments, or evaluate M&A targets this year, the report converts market momentum into a pragmatic roadmap with clear metrics for success and defensible timing for investments.

Electrical measurement systems are foundational tools for the industries driving global electrification and digital transformation. In 2026, the winners will be those who manage supply-chain fragility, embed software into hardware narratives, and shift commercial models toward recurring revenue while safeguarding instrument accuracy and serviceability. PW Consulting’s full market study is designed to be your playbook for those decisions.

To access the complete dataset, scenario models, and vendor dossiers that power these recommendations, please consult the full PW Consulting report.

For detailed analysis of this topic, please visit the official page:Electrical Measurement System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com