North America Die Bonder Equipment Industry Outlook 2034: Advanced Packaging Creating New Opportunities

Other |

2026-06-18 12:22:50

As companies plan capital allocation and growth trajectories for 2026, Ethyl Phenyl Acetate (EPAc) presents a distinctive combination of steady market expansion, concentrated supplier dynamics, and regulatory complexity. PW Consulting’s new market study — based on a 2020–2025 historical review with forecasts through 2032 — positions market participants to convert these characteristics into durable advantage. This preview outlines the strategic value of the full report for executive decision-making while preserving the granular data that drives commercial action (available through our full release).

Ethyl Phenyl Acetate Market

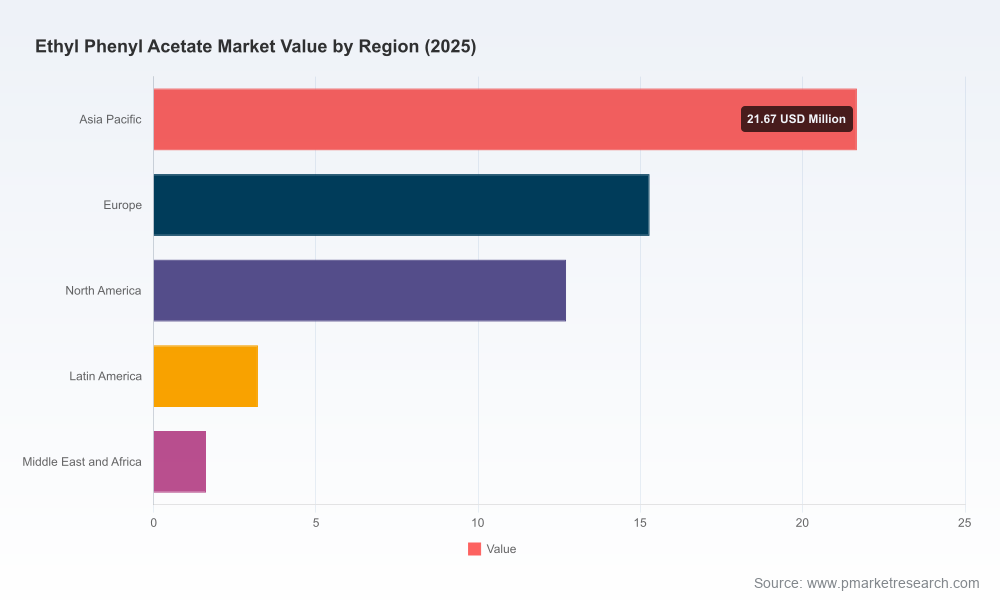

Our modelling shows the global Ethyl Phenyl Acetate market at an estimated USD 54.5 Million in the base year (2025), growing at a compound annual growth rate of approximately 4.95% across the 2026–2032 forecast window and reaching an estimated USD 76.4 Million by 2032. That growth is neither explosive nor marginal — it is the kind of consistent, addressable expansion that favors companies with focused product strategies, disciplined cost management, and regulatory foresight.

Ethyl Phenyl Acetate Market

Executives face a narrow window in 2026 to set the operational posture for the next 3–5 years: commit to plant projects, negotiate long-term feedstock contracts, or pursue targeted M&A. The PW Consulting report translates market-level projections into firm-level decision levers by combining demand forecasting with plant-level economics, supplier benchmarking, and regulatory scenario analysis. In short, the report converts macro growth into tactical actions with quantified upside and downside ranges.

Ethyl Phenyl Acetate Market

Our analysis shows production economics for EPAc are heavily feedstock-driven: raw materials — principally phenylacetic acid and ethanol — account for the dominant share of operating expenses. Phenylacetic acid availability and price behavior are therefore core drivers of manufacturing margins and project viability. In 2025, global phenylacetic acid production provided the necessary supply base for ethyl acetate derivatives at scale; movements in those feedstock markets materially shift breakeven cost at the plant level.

Regulation has a quantitative and qualitative impact on any 2026 plan. Key feedstocks for EPAc are controlled in multiple jurisdictions due to diversion risks, and regulatory changes through 2025 have increased vetting, record-keeping and shipping requirements. These obligations translate into higher onboarding costs for new customers, slower approval timelines for new shipments, and stricter audit regimes for producers and distributors.

The market exhibits meaningful concentration: the top producers and suppliers command material shares of the global supply pool. Within that structure, three strategic archetypes win:

Representative players include multinational flavor & fragrance houses, specialty chemical manufacturers, and regionally focused distributors. Their strengths vary by proposition: some control deep product development and global customer relationships; others offer manufacturing flexibility and competitive lead times. For market entrants and potential acquirers, the choice is between buying scale, acquiring capabilities, or building targeted assets internally.

Two classes of developments are especially relevant for 2026 planning:

Decisions on plant sizing, location and process route should be made from a multi-dimensional view that includes feedstock cost scenarios, labour and utility dynamics, logistics, and access to high-value local markets. Our plant-level models show that breaking ground on a new facility without guaranteed feedstock access and offtake commitments exposes sponsors to substantial downside. Conversely, opportunistic expansions aligned with offtake and long-term supply contracts materially improve IRRs.

Our scenario suite maps outcomes across three vectors: feedstock price shock, regulatory tightening, and demand shifts between natural and synthetic flavor/fragrance ingredients. Each scenario is translated into impacts on EBITDA margin, payback horizon for greenfield projects, and recommended tactical responses. Managers who embed these scenarios in 2026 budgets will have clearer thresholds for action: when to accelerate investment, when to pause, and when to pursue consolidation.

The full study is built for implementation. Highlights include:

Many advisory products stop at descriptive market sizing. Our approach ties that sizing to executable choices: which contracts to sign, what plant scale to build, which certifications to prioritize, and how to structure supply agreements to preserve margin under stress. For executives whose 2026 decisions will shape their competitive position through 2028 and beyond, the value is the reduction of strategic ambiguity and improved capital efficiency.

This preview is intended to demonstrate the analytic depth and practical focus of the full Ethyl Phenyl Acetate market study while reserving the detailed segmentation and proprietary models that underlie our recommendations. For access to the complete dataset, regional and application splits, downloadable financial models, and supplier scorecards, contact PW Consulting or visit our research portal to obtain the full report and speak with one of our industry strategists.

For detailed analysis of this topic, please visit the official page:Ethyl Phenyl Acetate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com