Rhinoplasty in Dubai: Advanced Nose Reshaping Methods

Other |

2026-05-07 09:02:11

PW Consulting today releases an executive briefing drawn from our forthcoming Disproportionated Rosin Market report — an actionable intelligence package tailored to inform boardroom decisions throughout 2026. The brief synthesizes macro trends, supply-chain realities, regulatory considerations, and competitor positioning to highlight where value will be created and captured in the DPR (disproportionated rosin) value chain during the next investment cycle.

Disproportionated Rosin Market

After a steady expansion across the early 2020s, the global disproportionated rosin market has reached a scale that demands strategic reorientation. Our market model — benchmarked to 2025 as the base year and covering historical performance from 2020–2025 with a forecast horizon of 2026–2032 — shows the market continuing to expand at a mid-single‑digit compound annual growth rate (CAGR) of 4.19% through the forecast period. In cash terms (USD, revenue unit: Million), the market expanded meaningfully from the beginning of the historical window and is projected to continue upward momentum into the early 2030s.

Disproportionated Rosin Market

That trajectory has three practical implications for decision‑makers in 2026:

Disproportionated Rosin Market

PW Consulting’s full report is built for use, not just observation. It combines granular market modelling with an operational playbook for procurement, product managers, and corporate development teams. Core deliverables include:

To preserve the commercial value of the analysis and honour competitive confidentiality, the full report contains the detailed segmentation tables, regional and application splits, and proprietary scenario outputs available through the PW Consulting portal.

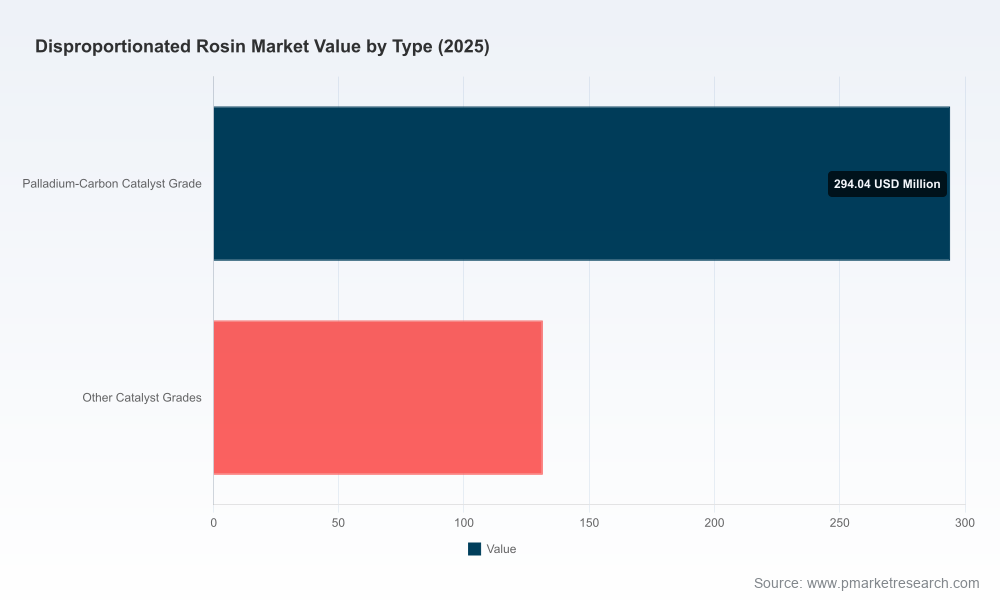

Procurement teams should note three structural facts underpinning DPR economics. First, gum rosin remains the primary upstream feedstock across the industry, representing the majority share of global rosin production. Second, global rosin output exceeds one million metric tons annually, with tall oil rosin — a by‑product of kraft pulping — supplying a sizable minority of that volume; tall oil volumes exceed several hundred thousand metric tons per year and typically trade at higher-purity benchmarks. Third, market export pricing for disproportionated rosin broadly tracks specialty resin price cycles; current industry surveys place average export transaction levels at approximately USD 2,000 per metric ton, with premium differentials for catalytic grades and stabilized formulations.

These realities create three payoffs for 2026 decisions:

Regulatory frameworks — particularly REACH and equivalent regional registrations — continue to shape formulation choices. Disproportionation via catalytic processes is not only a production differentiation; it serves to reduce oxidation susceptibility and supports compliance dossiers for derivative use in adhesives, rubber, and coatings. For manufacturers and buyers alike, technical specifications that align with registration pathways shorten time‑to‑market and reduce product substitution risk. Our report outlines a step‑by‑step compliance checklist for 2026 procurement rounds, including recommended analytical assays and documentation to request from suppliers.

The DPR market sits in the middle ground between commodity resin chains and speciality polymer additives. Market concentration is moderate: the three largest producers account for roughly one-third of supply, while the top five capture less than half — a structure that combines global majors with numerous regional specialists.

Key player archetypes identified in our analysis include:

Participants to watch in the coming 18 months include established western resin integrators that can bundle DPR into larger adhesive and polymer portfolios, and Asia‑based manufacturers that combine scale manufacturing with short lead‑times to regional formulators. The interplay between these two groups is creating the window for strategic alliances, distribution partnerships, and targeted M&A — particularly for companies seeking to accelerate access to specialized grades or to secure feedstock linkages.

Drawing on our modelling and supplier intelligence, PW Consulting recommends four high‑impact actions for executives planning for 2026:

Executives who commission the full PW Consulting report obtain immediate answers to operational questions that cannot be summarized in a briefing without compromising proprietary value. Examples include:

The disproportionated rosin market in 2026 presents a blend of predictable growth and actionable complexity. With a stable mid‑single‑digit CAGR guiding overall demand, this is not a market dominated by scale alone; technical capability, feedstock access, and regulatory alignment determine winners. PW Consulting’s report translates those dynamics into executable steps for procurement, R&D, and corporate development teams preparing budgets and strategic roadmaps this year.

For executives planning capital allocation, supplier negotiations, or M&A activity in 2026, missing a single quarter of opportunity can shift a multi‑year return profile. Our full report contains the granular segmentation, model workbooks, supplier scorecards, and scenario outputs required to make those decisions with conviction. Access the complete analysis, proprietary tables, and actionable annexes via the PW Consulting portal to convert insight into commercial advantage.

For detailed analysis of this topic, please visit the official page:Disproportionated Rosin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com