Road Construction Services Market 2026: Strategic Imperatives from PW Consulting’s New Market Report

As PW Consulting’s Chief Industry Analyst, I am pleased to present an executive preview of our newest market research on Road Construction Services. This briefing distills the critical strategic takeaways that infrastructure owners, contractors, investors, and policy-makers must act on in 2026. The full report—built on a comprehensive base year of 2025 and forecasting through 2032—combines rigorous market modeling, scenario stress-testing, and practical playbooks to guide high-stakes decisions. Below I highlight why the next 12 months are pivotal, which levers will most materially affect outcomes, and how market participants can translate insight into action.

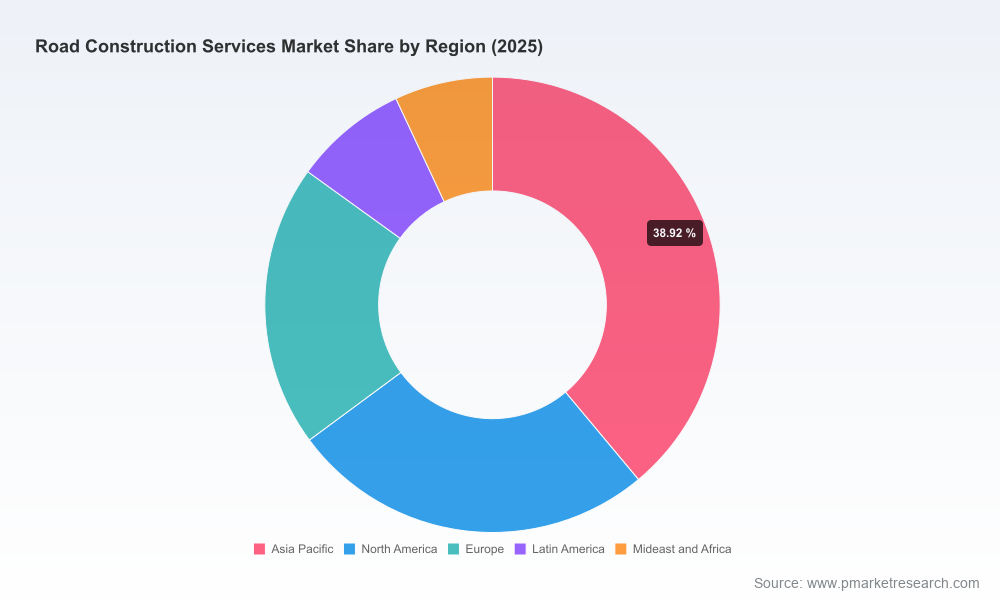

Road Construction Services Market

High-level market trajectory: what the topline means for strategy

Our model projects the global road construction services market to continue expanding at a steady compound annual growth rate (CAGR) of approximately 7.51% through the 2026–2032 forecast window. After registering robust growth through 2025, the market moves into a phase characterized by elevated public-works demand, sustained maintenance backlogs, and differentiated private-sector activity driven by mobility and logistics investments.

Road Construction Services Market

These topline dynamics translate into three strategic realities for 2026 decision-makers:

Road Construction Services Market

- Scale opportunities are real—aggregate market size is meaningfully larger than five years ago, creating room for new entrants and expansion plays.

- Fragmentation persists—market concentration remains low, favoring regional champions and nimble specialists that can move faster than global incumbents on tailored bids and performance-based contracts.

- Volatility risk is elevated—input-costs and labor tightness mean that headline growth does not equate to margin expansion without deliberate operational and contractual adjustments.

Why 2026 is a strategic inflection point

Three converging factors make 2026 a year for decisive action:

- Macro-fiscal momentum: Public infrastructure programs announced during the pandemic recovery years are transitioning from planning to award and procurement stages, accelerating contract flow for major highway and urban mobility works.

- Cost and supply-chain pressure: Material price volatility and tariff regimes introduced in 2025–2026 are re-pricing bid books and capex forecasts across projects, placing a premium on procurement agility and hedging strategies.

- Labor-market tightness: Persistent shortages of skilled trades, coupled with accelerating wage inflation in many markets, are forcing employers to rethink workforce sourcing, productivity-enhancing technologies, and subcontracting models.

Collectively, these dynamics create an environment in which timing, contract design, and execution capability can materially change value capture. Firms that anticipate and adapt will convert market growth into sustainable margin improvement.

Operational levers that will determine winners in 2026

Our fieldwork and quantitative analysis identify five operational levers that separate outperformers from laggards.

- Integrated procurement and materials strategy: Firms that lock in diversified supply sources, adopt indexed contract clauses, and build inventory resilience will limit exposure to short-term price spikes and tariffs.

- Workforce orchestration: Active investments in training, retention incentives, and partnerships with technical schools can offset regional labor gaps. Digital labor-management tools that optimize crew utilization show quick payback in high-cost labor environments.

- Modular and repeatable delivery models: Standardized design-build modules, preassembled elements, and mechanized workflows raise throughput and reduce dependency on scarce skilled trades.

- Data-driven maintenance prioritization: Outcome-based maintenance contracts that leverage remote sensing and predictive analytics redirect spend to interventions with demonstrable ROI, unlocking public-sector dollars.

- Contractual innovation: Performance-linked payment mechanisms, shared-risk indexes for materials, and targeted guarantees for schedule adherence align incentives between owners and contractors in volatile markets.

Competitive landscape: positioning for 2026 bids and partnerships

The global competitive field includes a mix of state-backed engineering giants, diversified European constructors, leading private-sector contractors, and specialist heavy-civil firms. Important structural notes from our analysis:

- Large, integrated construction conglomerates with national program mandates continue to execute mega-projects and cross-border portfolios, often leveraging scale and public-sector relationships to secure long-duration works.

- European and North American firms emphasize concession models, lifecycle maintenance expertise, and sustainability credentials—attributes that win regulated highway and urban mobility mandates.

- Regional and specialist contractors remain the marginal bidders on complex local works where speed, regulatory nuance, and partner networks matter more than global scale.

Selected company insights from our competitive review:

- Major state-backed integrators: A group of Beijing-headquartered state-owned engineering firms maintain broad capabilities across highways, bridges, and major transport corridors. Their global positioning is strengthened by strategic infrastructure initiatives that emphasize cross-border connectivity.

- European diversified players: European construction multinationals combine design-build expertise with motorway concessions and maintenance portfolios, positioning them to capture full-life-cycle contracts and integrated financing opportunities.

- North American heavy-civil specialists: Large U.S. contractors and engineering firms continue to lead on complex, high-spec highway projects where local regulatory knowledge, unionized labor models, and EPC experience are decisive.

Recent market moves reinforce these patterns. For example, a European-led joint venture secured a major highway expansion and interchange renewal contract late in 2025, demonstrating continued appetite for large-capacity upgrades in mature markets. Meanwhile, U.S. firms are formalizing multi-year growth plans and winning task-based state agreements that emphasize mobility system optimization—moves that signal both confidence and strategy recalibration for a more volatile input-cost environment.

Risk landscape and mitigation approaches

Our risk assessment highlights three high-probability exposures and corresponding mitigation strategies that should inform 2026 planning cycles:

- Material-price shocks and tariffs: With tariffs and price surges observed in recent quarters, firms should embed indexed-cost mechanisms in contracts, diversify sourcing, and explore forward-procurement where capital allows.

- Labor scarcity and wage inflation: Workforce shortages necessitate investments in productivity-enhancing equipment, targeted upskilling, and flexible subcontracting frameworks to maintain delivery schedules.

- Policy and permitting uncertainty: Project pipelines can be delayed by regulatory shifts; proactive stakeholder engagement and phased delivery models reduce the risk of stalled cash flows.

What the PW Consulting report delivers—practical content for 2026 action plans

The full report is built as a practitioner’s toolkit. Key inclusions are tailored to support both strategic planning and immediate procurement decisions:

- Topline market sizing and baseline forecasts through 2032, with scenario variants that quantify upside and downside paths under different commodity and labor regimes.

- Detailed playbooks for contractors and owners on procurement design, risk allocation, and contract clauses that protect margins in inflationary environments.

- Operational diagnostics and implementation checklists covering workforce strategy, mechanization opportunities, and digital adoption roadmaps.

- Competitive intelligence dossiers on leading vendors, with comparative capabilities, recent wins, and partnership openings (summarized to preserve competitive sensitivity).

- M&A and strategic partnership matrices that identify adjacencies for capability gaps, and valuation sensitives for target screening.

- Decision-support spreadsheets and scenario-model templates that allow finance and strategy teams to test investment cases under user-defined inputs.

Importantly, the report intentionally reserves granular segment-level percentages and proprietary subregional allocations for the full publication. This “preview” approach is designed to establish the strategic narrative and prompt targeted access to the primary dataset for transaction-grade diligence.

Recommended actions for senior leaders in 2026

Based on our analysis, PW Consulting recommends a focused set of priority actions for the coming 12 months:

- Initiate a three-point procurement resilience program: supplier diversification, indexed contract language, and a small but strategic inventory buffer for critical inputs.

- Accelerate workforce capacity initiatives combining targeted hiring, apprenticeship partnerships, and investment in mechanization that increases per-crew productivity.

- Pursue selective M&A or alliance plays to acquire missing capabilities—either digital maintenance platforms, specialized civil equipment fleets, or regional footholds—using our attached valuation sensitivity templates.

- Revisit bid governance with a standardized margin-protection checklist and a rapid-response post-award change-order framework to preserve cash flow under volatility.

Conclusion: converting market growth into durable advantage

The road construction services market in 2026 presents both tangible growth and meaningful risk. Aggregate demand is expanding and will reward firms that pair scale ambition with operational resilience. Fragmentation creates entry points for focused players; yet input-cost volatility and labor constraints mean that topline growth will not automatically translate into profit unless companies revise procurement, workforce, and contract strategies now.

PW Consulting’s full Road Construction Services Market report provides the detailed quantitative back-up, segment-level diagnostics, and executable playbooks necessary to move from insight to action. For organizations preparing budgets, shaping bid strategies, or evaluating strategic transactions in 2026, the report is designed as a mission-critical resource.

Access and next steps

To review the complete forecast tables, scenario workbooks, and the full competitive dossiers referenced above, please consult the report landing page. Our consulting teams are available to deliver bespoke briefings, build customized financial models from the report’s base datasets, and support rapid implementation sprints tied to procurement and bid cycles throughout 2026.

For detailed analysis of this topic, please visit the official page:Road Construction Services Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com