Breaking: Rock Drilling Equipment Market Set to Surge Amidst Technological Advancements

Other |

2026-06-30 10:06:18

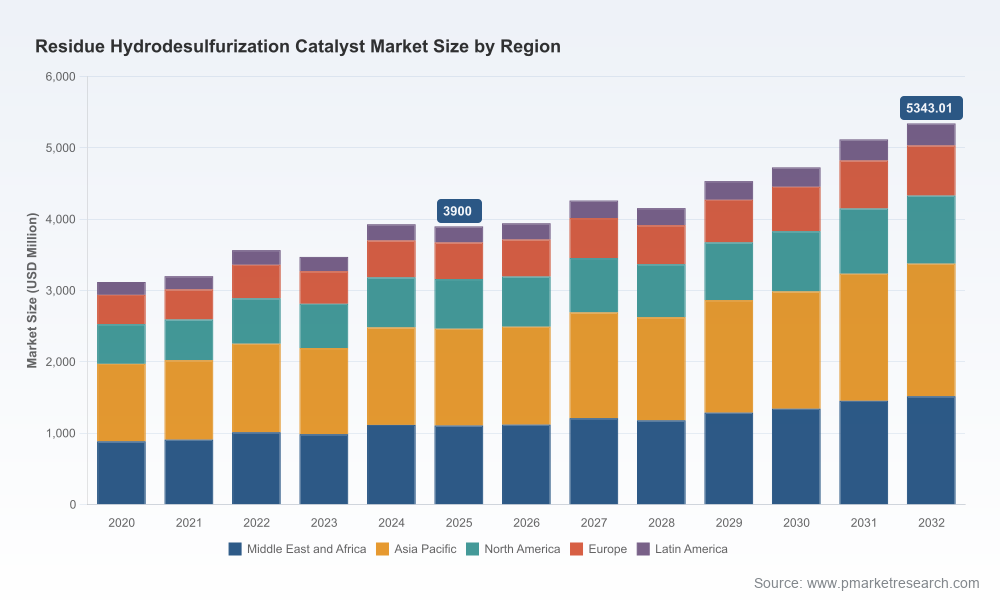

PW Consulting’s new Residue Hydrodesulfurization (R-HDS) Catalyst Market report — anchored on a 2025 base year and projecting through 2032 — offers a decision-grade analytical framework for executives planning capital allocation, technology bets, and go-to-market moves in 2026. Our modeling shows the market around USD 3,900 million in 2025 and a steady trajectory (2026‑2032) that equates to a 4.61% CAGR over the forecast window, culminating in a multi‑billion dollar market by 2032. That macro view masks important pockets of risk and opportunity: the sector is moderately concentrated (CR3 ≈ 58.4%, CR5 ≈ 76.2%), supply chains remain exposed to key raw‑material swings, and regulatory pressure continues to push demand for higher‑activity NiMo and CoMo chemistries. This press release summarizes the strategic value of our report for 2026 decision-making — presenting the depth of our analysis while reserving granular segmentation and proprietary decks for the full study.

Residue Hydrodesulfurization Catalyst Market

Regulatory tightening and fuel-quality enforcement. Global ultra‑low sulfur mandates are accelerating upgrades to residue units and catalyzing demand for high‑activity residue HDS catalysts able to process sour, heavy feeds. Refiners that postpone decisions face both compliance risk and margin dilution as lighter products command premium pricing.

Residue Hydrodesulfurization Catalyst Market

Capital‑intensive retrofit cycles. Many residue‑upgrading projects operate on multi‑year investment timetables; decisions taken in 2026 will determine vendor selection, catalyst formats, and maintenance regimes for a decade. Timing matters: incremental advances in catalyst life or activity can shift project IRRs materially.

Residue Hydrodesulfurization Catalyst Market

Input cost volatility. Raw‑material exposure is non‑trivial: molybdenum spot prices experienced approximately 18–22% volatility over a 12‑month span in 2025, and base metal catalyst feedstocks trade in wide ranges (standard grades in the USD 28–45 per kg band in 2025). Specialty resid formulations command significant premiums versus commodity grades. These dynamics directly affect manufacturing margins, contracting strategy, and the attractiveness of long‑term supply agreements.

Market concentration and consolidation dynamics. With a concentrated supplier base, strategic M&A and partnerships are reshaping capability sets. A notable example: in November 2025, W.R. Grace acquired full ownership of Advanced Refining Technologies (ART), strengthening its footprint in resid hydroprocessing catalyst technologies for fixed and ebullated bed applications. Buyers and incumbents must factor consolidation risk into procurement and competitive planning.

Market sizing and scenario analysis: rigorous, bottom‑up market sizing for 2020–2025 and forward projections through 2032 (base case CAGR 4.61%) with alternate scenarios that stress raw‑material shocks, regulatory acceleration, and changes in refinery feedstock mixes.

Technology and performance benchmarking: comparative evaluation of fixed‑bed, ebullated‑bed and slurry options, with performance trade‑offs (activity, selectivity, resistance to poisoning, cycle life) mapped to refinery operating profiles and feedstock characteristics.

Cost and margin models: transparent manufacturing cost models that isolate raw‑material, processing and logistics components; sensitivity modules show P&L impact from +/-20% swings in key inputs and specialty premium dynamics.

Supplier capability matrix: vendor profiles, technology roadmaps, and a procurement risk matrix that factors concentration, geographic exposure and service capability — enabling RFP design and long‑lead supplier negotiations.

M&A and partnership playbook: target screening criteria, value creation levers (technical, geographic, aftermarket service), and integration risks — essential for private equity and strategic acquirers evaluating catalyst or technology assets.

Operational playbooks for refiners: retrofit sequencing, catalyst changeout strategies, operational levers to maximize run lengths, and contract structures (consignment, risk‑share, performance‑based) tailored to 2026 budget cycles.

The report includes detailed company profiles and capability assessments for the core participants shaping the R‑HDS ecosystem. Leading global technology and catalyst suppliers — including Axens SA, Albemarle, Haldor Topsoe, Honeywell UOP, Johnson Matthey, Shell/Criterion, and BASF — remain central to system performance at scale, generally supplying high‑activity CoMo and NiMo chemistries, advanced supports, and integrated service offerings. Regionally significant producers such as Sinopec and CNPC provide competitive pricing and proximity advantages in Asia.

Key strategic observations:

Incumbents with deep fixed‑bed experience are augmenting portfolios for ebullated and slurry systems to address conversion‑heavy projects and maximize residue conversion to distillate range products.

Specialty formulations and service contracts are becoming differentiators: customers increasingly value vendors that bundle catalyst with performance guarantees, remote monitoring, and lifecycle optimization.

Consolidation increases negotiating leverage but also concentrates supply‑chain risk; the W.R. Grace acquisition of ART exemplifies how scale plus specialized IP can reframe competitive dynamics.

Refiners — prioritize flexibility and staged investment. Adopt retrofit designs that preserve feedstock optionality; use performance‑linked contracts to align supplier incentives and protect margins against metal price spikes.

Catalyst manufacturers — de‑risk supply chains and differentiate through service. Secure long‑term molybdenum and cobalt supply, invest in alternative support technologies that reduce specialty loading, and commercialize predictive analytics to monetize uptime and cycle‑extension.

Investors and acquirers — stress test valuations. Incorporate raw‑material price scenarios and regulatory acceleration into downside cases. Value service revenue and aftermarket capabilities more highly than commodity catalyst sales.

Technology licensors and EPCs — offer modular, retrofit‑friendly packages that reduce brownfield execution risk and accelerate time‑to‑fuel‑compliance; provide bundled warranties to shorten client approval cycles.

Our forecast suite provides a base case (CAGR 4.61%), an upside anchored to accelerated refinery upgrades and favorable feedstock economics, and a downside that models prolonged raw‑material inflation and slower capital deployment. Embedded sensitivity models quantify the impact of key inputs — e.g., a persistent +20% move in molybdenum prices, shifts in specialty premium spreads, or an earlier implementation of ultra‑low sulfur standards — on supplier margins, refiner operating cost per barrel, and project IRRs. These tools are designed to support board‑level deliberations, budget cycles and M&A diligence in 2026.

Set procurement and hedging policies now: move from annual spot buying to a layered procurement posture that combines long‑term offtake, indexed contracts and limited spot exposure.

Re‑prioritize R&D budgets: favor chemistries and support designs that reduce precious metal intensity or extend catalyst life in high‑tar, high‑contaminant feeds.

Design M&A diligence around aftermarket value: catalytic technology is increasingly monetized via service delivery; measure targets accordingly.

Run cross‑functional war games: align commercial, operations and technical teams on retrofit sequencing and vendor selection to avoid costly rework and downtime.

In keeping with the “trailer” principle, this release demonstrates the rigor and strategic orientation of PW Consulting’s analysis while intentionally withholding core proprietary segmentation tables and granular regional/application shares that are central to transaction and procurement decisions. The full report contains detailed regional and application splits, vendor share tables, price decks, and downloadable financial models that enable immediate scenario testing. These elements are available exclusively in the complete study and the accompanying data workbook.

Decisions made in 2026 will shape refinery competitiveness and catalyst supplier economics for years. PW Consulting’s Residue Hydrodesulfurization Catalyst Market report translates a complex interplay of regulation, feedstock evolution, raw‑material volatility, and supplier consolidation into pragmatic choices: which technologies to adopt, how to structure supply agreements, what to prioritize in R&D, and how to size M&A moves. For executives who need to convert macro signals into executable plans for capital allocation and commercial negotiation, our report provides the analytics, frameworks, and vendor intelligence to act with confidence.

For access to the full dataset, proprietary segmentation, vendor scorecards, and the downloadable scenario models referenced here, please visit PW Consulting’s report page or contact our market access team to schedule a briefing.

For detailed analysis of this topic, please visit the official page:Residue Hydrodesulfurization Catalyst Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com