Low Fat Soya Flour Market: Strategic Imperatives for 2026 — PW Consulting Executive Brief

As companies finalize strategic plans for 2026, the low fat soya flour market presents a distinct combination of steady growth, structural consolidation, and rapid innovation that will shape supplier selection, product development, and capital allocation decisions. PW Consulting’s latest market study synthesizes historical performance (2020–2025) with a robust forecast model for 2026–2032 to deliver pragmatic guidance for executives, investors, and supply chain leaders. The headline: the addressable market expanded materially through 2020–2025 and, under our base-case assumptions, will continue to grow at a mid-single-digit compound annual growth rate (CAGR) over the 2026–2032 forecast window — a trajectory that supports targeted expansion while demanding disciplined commercial execution.

Low Fat Soya Flour Market

Macroeconomic Snapshot: Growth with Predictable Momentum

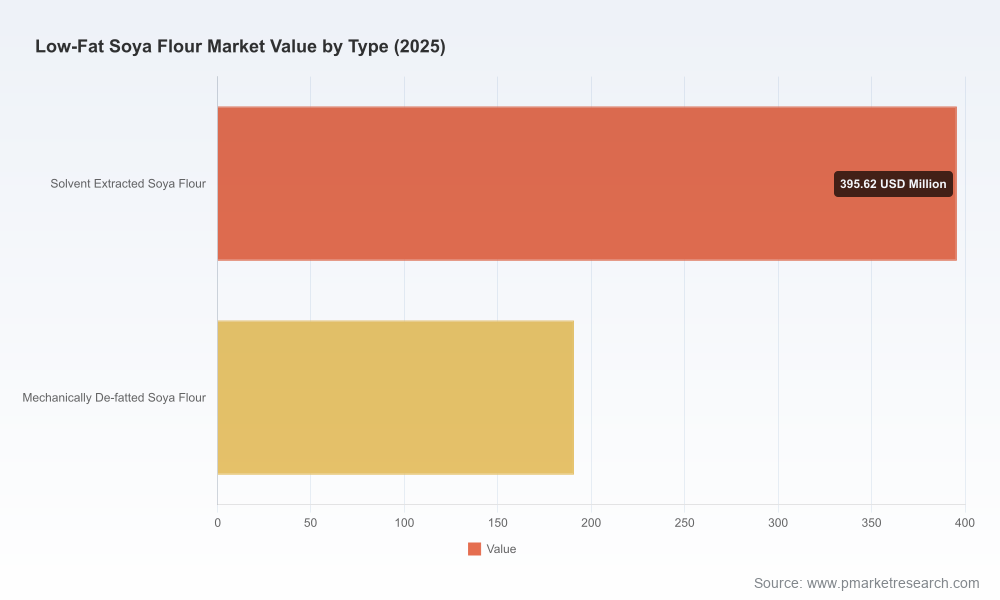

Our market sizing shows the low fat soya flour sector recovering and re-accelerating after short-term volatility in the early 2020s. Between 2020 and 2025 the market moved from a smaller base to a substantially larger footprint, reflecting stronger end-market adoption in bakery, plant-based protein, and fortified nutrition. From 2026 onward, our modelling projects steady growth to the end of the forecast horizon; the report quantifies this path and applies sensitivity analysis across alternative demand and input-cost scenarios. The forecasted CAGR for 2026–2032 (5.72%) frames a market environment that is attractive to both incumbent processors and new entrants — but it also highlights the importance of granular, actionable intelligence when sizing investments or negotiating supply contracts.

Low Fat Soya Flour Market

Why 2026 Matters — Dynamics Converging Now

- Demand-side diversification: Consumer preferences continue shifting toward protein-dense, lower-fat formulations in bakery, functional beverages, and meat-alternative products. Low fat soya flour’s technical attributes — notably its protein functionality and low residual fat — keep it central to reformulation strategies.

- Supply-side adjustments: Global soybean processing activity has risen to record levels, altering meal and flour flows. Regional crushing increases and changing export dynamics are reshaping trade patterns and local availability.

- Regulatory and classification clarity: Low fat soya flour is clearly identified within international tariff frameworks, enabling more predictable customs treatment and facilitating cross-border commercialization for exporters and importers who prioritize compliance-first strategies.

- Consolidation and concentration pressures: The market exhibits moderate concentration among leading processors. That dynamic creates both negotiating leverage and integration risk for buyers — an important input when evaluating long-term supplier commitments or considering vertical investments.

- Product innovation and premiumization: New ultra-high plant protein offerings and targeted low-fat formulations are expanding the addressable use-cases for soya flour, from texturizing meat analogues to protein-fortifying bakery mixes.

Strategic Takeaways for 2026 Decision-Making

- Procurement strategies must evolve from cost-only to capability-aware: Low fat soya flour suppliers differ not just on price but on certification, non-GMO sourcing, traceability, and technical support. RFPs should include performance-based clauses tied to functional outcomes (e.g., dough machinability, protein solubility) rather than only to commodity-price pass-throughs.

- Hedging and flexible contracting are mission-critical: Raw material flows and crush dynamics create episodic price pressure. Structured contracts with indexed pricing, floor/cap mechanisms, and volume flexibility reduce margin volatility for both processors and downstream manufacturers.

- Invest selectively in product differentiation: There is commercial value in low-fat soya flours tailored for specific applications (e.g., bakery vs. meat analogues). Prioritize product development that demonstrably reduces downstream processing complexity or cost, or that enables premium positioning through label claims.

- Monitor consolidation activity and partnership opportunities: With a meaningful portion of the market clustered among top processors, acquisitive or collaborative moves can quickly change regional access and margin pools. Use concentration metrics and scenario exercises (included in our report) to stress-test M&A rationale.

- Build resilience into supply chains: Source diversification, capacity visibility, and logistics contingency planning are no longer optional. Our report’s supplier risk matrix helps teams rank sourcing alternatives by disruption risk and cost-to-switch.

- Regulatory readiness as a commercial lever: Leverage tariff classification and labeling clarity to unlock new routes-to-market, particularly for exporters — and to accelerate product launches in regions where compliance delays historically hindered market entry.

Competitive Landscape — Who Matters and Why

The low fat soya flour market is shaped by established global agribusinesses, regional processors, and specialized ingredient houses. Our competitive analysis examines strategic positioning across capability, scale, and product portfolio.

Low Fat Soya Flour Market

- Cargill, Incorporated: A global processor supplying branded defatted/low-fat soy flour with defined functional claims. Its emphasis on application support (e.g., improved dough machinability and egg replacement) makes it a preferred partner for large bakery and snack manufacturers seeking technical co-development.

- Archer Daniels Midland Company (ADM): ADM’s breadth of processing capacity and its non-GMO options position it as a scale supplier for food and feed customers. Its infrastructural reach is a strategic advantage in price-sensitive, high-volume segments.

- Tiger Soy, LLC: A regionally-focused supplier that differentiates through local sourcing, Non-GMO and gluten-free credentials — relevant for customers pursuing shorter supply chains and traceable inputs.

- Soy Austria Produktions GmbH: A supplier with a clear non-GMO, ingredient-centered portfolio that serves food manufacturers requiring specialty and consistent-quality low-fat variants.

- Agricultural Cooperative BACEX, Bic Services, Seasons International, CHS Inc., Bunge Limited: These players span cooperative models, ingredient specialists, exporters, and global crushers; collectively they form a diverse supplier ecosystem that buyers should map against reliability, certification, and technical service levels.

Recent market developments underscore both capacity and capability shifts: new processing facilities and ultra-high-protein product launches indicate ongoing investment into the value chain. For buyers and investors, these developments signal potential margin pressure in commoditized channels and opportunity in higher-value differentiated niches.

What PW Consulting’s Report Delivers — Practical, Transaction-Ready Intelligence

This study is designed as a decision-support tool for 2026 planning cycles. Key deliverables include:

- Transparent market-sizing and trend analysis built on a reconciled historical dataset (2020–2025) and scenario-driven forecasts for 2026–2032.

- Supply-demand balance models, including crush and by-product flow sensitivities, with alternate scenarios to stress-test procurement and investment choices.

- Segment-level frameworks (by region, product type, and application) that explain route-to-value and margin pools — presented without exposing client-sensitive microdata in this briefing.

- Competitor benchmarking and capability maps for the leading processors and ingredient specialists, including go-to-market and partnership archetypes.

- Commercial playbooks: sourcing templates, pricing-policy guidelines, and a supplier-risk assessment toolkit to accelerate contract negotiations and onboarding.

- M&A and capital-allocation guidance, with a shortlist of target profiles and valuation sensitivity tables for strategic and financial buyers.

- Interactive datasets and dashboard access for in-house analysts to re-run scenarios with custom assumptions.

How to Use This Intelligence — Three Immediate Moves for 2026

- Execute an immediate supplier-capability audit: Use our supplier-risk matrix to re-evaluate current contracts before annual renewals. Focus on technical support, certification coverage, and delivery resilience.

- Pilot differentiated SKUs: Allocate a modest R&D and commercial testing budget to reformulations that leverage low fat soya flour’s functional benefits; measure manufacturing efficiency gains and consumer acceptance concurrently.

- Prepare strategic optionality: Develop contingent capital plans (e.g., JVs, minority investments, or tolling agreements) that can be activated if market concentration or price moves threaten supply security or margin targets.

Final Note — The Missing Pieces You Need

This press briefing highlights the strategic implications emerging from PW Consulting’s research while preserving the proprietary datasets and granular segment tables that underpin our conclusions. Executives evaluating expansion, procurement, or transaction activity in 2026 will need the full report’s detailed spreadsheets, regional and application breakdowns, and the downloadable scenario models to operationalize the advice above. For access to those resources, primary interview transcripts, and the interactive dashboard, please visit the PW Consulting research portal to request the full Low Fat Soya Flour Market report and schedule a briefing with our sector leads.

For detailed analysis of this topic, please visit the official page:Low Fat Soya Flour Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com