New Chinese Pastries Market 2026: Strategic Imperatives for Growth, Resilience, and Competitive Advantage

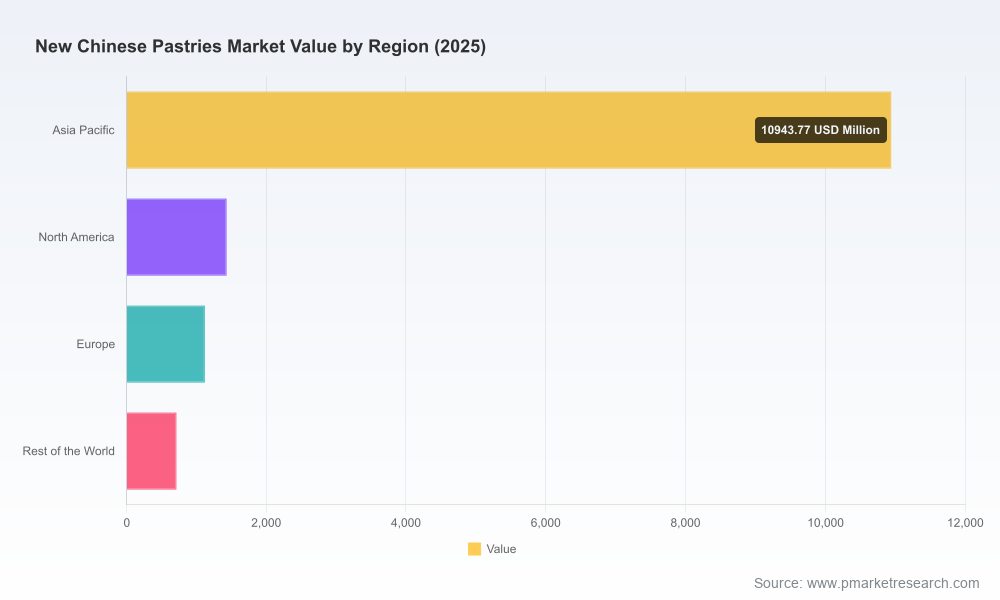

PW Consulting’s latest market study, New Chinese Pastries Market (base year 2025; forecast period 2026–2032), synthesizes five years of historical dynamics and a seven‑year forward-looking view to equip senior executives with the actionable intelligence required to make high‑stakes decisions in 2026. The industry is now a multi‑billion dollar market: our modelling places global revenues at USD 14,212.0 Million in 2025, growing at a compound annual growth rate (CAGR) of 8.42% into the forecast window. By 2032, the market is projected to approach USD 25.9 billion (USD Million basis), reflecting durable consumer demand and rapid commercialization of new product formats.

New Chinese Pastries Market

Why this report matters for 2026 decision cycles

- Timing. 2026 is the inflection year where regulation, ingredient cost structure, and channel evolution intersect — creating both risk and differentiated opportunity for first movers.

- Prioritization. Boards and corporate strategy teams need a prioritized roadmap: where to invest in product innovation, which channel economics to double down on, and which supply chain vulnerabilities to remediate before they become critical.

- Execution. The report is engineered not as a descriptive summary but as an execution guide — it translates market projections into concrete actions for R&D roadmaps, industrial investment, trade and retail partnerships, and M&A scouting.

Macro view: growth profile and structural signals

After a period of steady expansion between 2020 and 2025, the New Chinese Pastries market is entering a phase of accelerated monetization across premium, convenience, and frozen formats. Our top‑level figures show a consistent, mid‑single digit plus compound growth trajectory that supports sustained private investment and strategic reallocation within larger bakery portfolios. Despite this growth, market concentration remains low: the three‑firm concentration ratio (CR3) is around 18.45% and the CR5 is approximately 25.3%, underscoring a fragmented competitive environment where regional champions and specialist innovators continue to capture share from incumbents.

New Chinese Pastries Market

Key market dynamics shaping strategic choices

- Consumer sophistication and premiumization. Urban consumers are trading up into premium and fusion varieties while seeking cleaner labels, textural novelty, and convenience for on‑the‑go occasions. This dynamic drives SKU proliferation, premium pricing windows, and larger margins for branded premium products.

- Regulatory inflection points. Recent policy changes — most notably new national nutrition labelling rules expanding mandatory disclosures and the extension of allergen and intake warning regulations for prepackaged foods — materially affect product formulation, packaging design, and go‑to‑market timing. Enforcement timelines mean product relabeling and reformulation projects need to be underway in 2026 to avoid market disruptions in 2027–2028.

- Input cost and trade policy exposure. Our cost sensitivity work flags wheat flour and other commodity inputs as critical levers: wholesale wheat flour pricing and a substantial tariff environment on imports materially influence where manufacturers choose to localize flour sourcing, scale frozen production, and invest in ingredient innovation (e.g., high‑yield blends, alternative flours).

- Channel transformation. E‑commerce and frozen retail models continue to redefine national distribution footprints and cold‑chain requirements. Specialty bakery retail remains an important margin channel, but omnichannel strategies that integrate direct‑to‑consumer subscriptions, cold‑chain logistics, and retail partnerships show the fastest route to scale in our scenario analysis.

- Innovation supply chain. Trade shows and industry expos remain pivotal deal‑making venues: the Bakery China series (notably the 2025 and 2026 events) has accelerated ingredient innovation, processing automation, and packaging solutions — and is now a leading indicator of what will scale commercially within 12–24 months.

Operational and regulatory operational checklist for 2026

- Compliance sprint: initiate product label audits and allergen inventories now to meet new GB standards and mandatory warning label requirements ahead of enforcement windows.

- Ingredient hedging: build wheat and fat price scenarios into three‑year financial plans and evaluate local sourcing vs. tariff exposure given current import duty regimes.

- Cold‑chain readiness: invest selectively in freezing and frozen logistics capabilities where unit economics demonstrate higher lifetime customer value and reduced wastage.

- Channel playbooks: pilot premium DTC offerings with limited SKUs while expanding frozen SKU availability into supermarket and e‑commerce partners for broader reach.

Competitive landscape: what leading players are doing

The industry is characterized by a mix of national bakery groups, specialized frozen‑goods manufacturers, regional artisanal brands, and international incumbents adapting products for local tastes. Major players highlighted in our analysis include multinational and home‑market firms that each pursue distinct strategies:

New Chinese Pastries Market

- Dali Foods Group and larger national bakers are leveraging scale to invest in frozen production lines, distribution center rationalization, and export readiness — focusing on portfolio extension and cost optimisation.

- Specialist frozen pastry producers have prioritized supply chain integration and B2B customer wins by offering co‑packing and private label solutions to retail and foodservice partners.

- Artisanal and premium patisserie brands are playing the experience and gifting card, doubling down on premiumization, seasonal launches, and limited‑edition formats that command price premiums.

- International suppliers and Japan‑based bakers, active in the mainland and regional markets, typically bring process know‑how and Western baking techniques adapted to local palates; their strategic play is often through partnerships, licensing, or acquisition of local platforms.

Across these firm types, the pattern is clear: companies that pair nimble product development with disciplined route‑to‑market execution and regulatory readiness are winning scale while retaining margin. Our competitive profiles and capability matrices provide a granular read on each archetype, and identify potential M&A and partnership targets for acquirers seeking rapid entry.

What the report delivers — practical, executable assets

- A market sizing and scenario toolkit (USD Million basis) from 2020–2032, including base‑case and sensitivity paths keyed to input cost and regulatory shock scenarios.

- Channel economics models that map unit economics for specialty retail, frozen distribution, and e‑commerce, with break‑even analysis for cold‑chain investment.

- Product portfolio scorecards and an innovation prioritization matrix that quantify return‑on‑innovation for texture, formulation, and packaging interventions.

- A regulatory compliance playbook that decodes the new national food labelling rules and allergen/warning requirements, with a 12–18 month implementation checklist for R&D and packaging teams.

- Supply chain stress tests and raw‑material hedging scenarios (wheat price sensitivity, tariff exposure), and supplier risk heatmaps for critical inputs.

- Competitive diagnostic pages for leading firms and a curated shortlist of strategic targets for acquisition, JV, or co‑development across prioritized markets.

Risks, blindspots, and watch‑points for executives

- Regulatory execution risk: delayed relabeling or misaligned product formulations could trigger recalls or retail delistings in core metropolitan markets.

- Commodity volatility and trade policy: sudden swings in flour prices or shifts in import duties could compress margins for producers without diversified sourcing.

- Channel mis‑allocation: overinvestment in low‑margin channels without simultaneous brand and logistics investment can erode returns.

- Product proliferation: SKU bloat without disciplined rationalization increases complexity and capital tie‑up in frozen and retail inventory.

Strategic recommendations for 2026 action plans

- Implement a two‑track portfolio strategy: defend core heritage SKUs while allocating a fixed portion of R&D budget to fusion and textural innovations targeted at premium segments.

- Accelerate compliance and packaging redesigns now to avoid disruption at enforcement milestones; treat compliance as a commercial enabler rather than a cost center.

- Prioritize channel pilots that demonstrate repeat purchase economics and low unit logistics cost before national rollouts.

- Use trade events and ingredient expos as sourcing accelerators — target componentization of recipes to allow rapid reformulation in response to raw material shocks.

- Evaluate inorganic options in adjacent frozen snack and premium gifting spaces where scale and distribution gaps can be closed through acquisitions.

Conclusion — the strategic value of proprietary insight

In a fragmented but fast‑growing market, the difference between a reactive and a proactive strategy is measured in months and millions of dollars. PW Consulting’s New Chinese Pastries Market report supplies executives with the strategic roadmaps, operational checklists, and scenario models necessary to convert market growth into lasting competitive advantage in 2026 and beyond. We intentionally present deep, decision‑ready analysis while reserving segment‑level tables and detailed financial models for the full report — a designed friction to ensure that market participants engage directly with the primary deliverable for transaction‑grade intelligence.

To request the full report package, including downloadable modelling worksheets, executive briefings, and company‑level dossiers, please visit our official report page or contact our client services team for a briefing and licensing options.

For detailed analysis of this topic, please visit the official page:New Chinese Pastries Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com