Global AI Data Service Market Growing at 15.2% CAGR Through 2034

Other |

2026-07-04 05:54:30

As rugby's commercial ecosystem enters its next growth chapter, PW Consulting releases a focused industry brief designed to convert market intelligence into boardroom action. Built on a 2020–2025 historical base and a 2026–2032 forecast horizon, the study synthesizes macro demand trends, supply-side stressors, regulatory inflections and competitive manoeuvres. The headline: the global rugby equipment market has demonstrated resilient expansion through mid‑decade and is projected to continue growing at a steady compound annual growth rate of approximately 5.18% through 2032. For executives preparing 2026 budgets, channel plays, product roadmaps or M&A screens, the report functions as a strategic trailer—showing where value pools are expanding while preserving the granular segment numbers for subscribers who access the full dossier.

Rugby Equipment Market

Market trajectory — After recovering from pandemic distortions, the market expanded across the 2020–2025 period and is expected to reach a materially larger base by 2032. This continuity of growth validates both participation-driven demand and premiumisation in core categories.

Rugby Equipment Market

Concentration dynamics — Market concentration has stabilised in the mid‑range: the top three and five vendors control a meaningful share of revenue, reflecting a competitive environment where legacy brand equity and licensing arrangements remain decisive.

Rugby Equipment Market

Participation tailwind — Global registered player numbers climbed to roughly 9.6 million by 2024, with youth participation driving equipment upgrades and repeat purchases. This participation base is a leading indicator for grassroots-to-pro equipment demand into 2026 and beyond.

Senior leaders must translate these macro signals into concrete choices. Our report isolates five immediate priority actions for 2026 planning cycles:

Reassess product portfolios through a safety-and-performance lens. Regulatory updates (notably World Rugby Law 4 on impact testing that took effect in 2023) have raised the bar on protective equipment certification. Companies that accelerate compliance and communicate safety performance will capture premium positioning among clubs, academies and parents.

Hedge material cost exposure. The synthetic materials that underpin rugby balls and many protective components experienced price volatility—PVC/PU inputs rose materially in 2024—so procurement teams should model cost-plus versus fixed-margin scenarios and secure diversified supplier options.

Prioritise youth and grassroots channels. Youth demand expanded significantly in 2024, creating outsized lifetime value opportunities. Tailored SKUs, modular protective kits and academy sponsorships yield higher conversion rates than undifferentiated mass assortments.

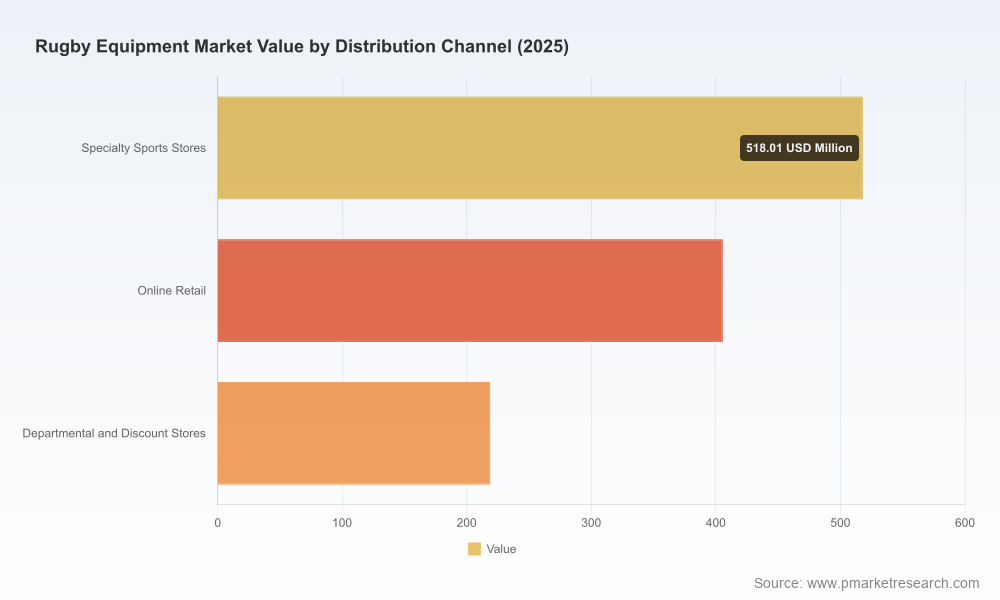

Invest selectively in digital direct-to-consumer (DTC) capabilities. Online retail has matured into a core distribution vector. Top performers blend proprietary customization tools, data-driven sizing and omnichannel fulfilment to shorten purchase cycles and increase attach rates for apparel and accessories.

Design M&A and partnership screens around capability gaps. Given the market’s moderate concentration, bolt-ons that add proprietary ball technology, headguard IP or club-level B2B training equipment can accelerate scale without chasing broad market share battles.

Our competitive analysis drills into incumbent brand strengths and emergent specialty manufacturers. Established global sports houses and niche rugby specialists coexist in a layered competitive structure: global apparel and footwear companies bring scale, distribution and major tournament partnerships; heritage ball makers and specialist protective-equipment manufacturers hold technical know‑how, official licensing and product credibility with governing bodies.

Legacy specialists retain technical leadership. Long-standing ball manufacturers and certified headguard producers continue to dominate official match supply due to decades of testing and endorsement relationships with governing bodies.

Global apparel and footwear brands leverage tournament sponsorships. Partnerships with World Rugby and national federations create episodic volume surges around flagship events, amplifying brand reach and accelerating the adoption of new match apparel and boot technologies.

Mass-market retailers compete on accessibility. Large sporting retailers and value chains sustain broader participation at entry price points, which is essential to conversion funnels and long-term player activation.

Adidas rolled out official tournament match balls and kits in late‑2023, reinforcing the commercial value of major-event licensing and the impact of event calendars on product launches.

Heritage manufacturers upgraded ball grip and certification in 2024, highlighting continuous product innovation as a table-stakes requirement for match‑grade equipment suppliers.

Specialist safety equipment firms released new headguard models compliant with enhanced impact standards in early 2025, underscoring the premium potential for certified protective goods.

Major heritage apparel exhibitors showcased sustainable performance fabrics at mid‑2025 trade events, signaling a pivot to environmentally conscious materials that do not compromise on performance.

Procurement and operations teams should note three near-term operational levers that our modelling indicates will have the highest ROI in 2026:

Supply diversification and near‑sourcing for critical polymer inputs to mitigate petrochemical price shocks.

Streamlined compliance pathways for import-sensitive markets (e.g., EU chemical restrictions), reducing time-to-shelf for revised protective-gear formulations.

Inventory and promotion optimisation that aligns with tournament calendars and youth-season peaks to avoid steep markdowns and capture event-driven demand surges.

The full report combines industry breadth with execution depth. Subscribers gain access to:

Scenario-based market forecasts through 2032 with embedded sensitivity to participation, price and material-cost variables.

Competitive scorecards that evaluate R&D capability, channel footprint, licensing exposure and product compliance readiness for the leading firms across the ecosystem.

Playbooks for go-to-market: channel prioritisation matrices, product bundle strategies for youth and academy markets, and digital commerce conversion tactics.

Supply chain risk maps that identify single‑source dependencies and recommend mitigation tactics, including supplier qualification checklists and cost hedging templates.

A transaction toolkit for M&A and JV screening: valuation heuristics, integration risk checklists and a shortlist of capability targets aligned with different strategic trajectories.

Regulatory-impact appendices outlining compliance actions for Law 4 testing, regional chemical limits and product labelling best practices.

Executives should treat the report as both a diagnostic and an operational roadmap. Recommended usage patterns:

C-suite strategy sessions — Translate the forecast scenarios into revenue targets and margin guardrails for FY2026.

Product and R&D — Prioritise investments in certified safety innovations and sustainable materials that offer differentiated value with defensible pricing.

Commercial teams — Reallocate marketing and inventory spend to youth acquisition and DTC channels where lifetime value curves are steeper.

Corporate development — Use the M&A toolkit to evaluate tuck‑ins that close capability gaps rather than pursuing headline market-share plays.

The study’s base year is 2025, using a historical window covering 2020–2025 and a forecast period from 2026–2032. Our topline CAGR and trajectory projections integrate primary interviews with manufacturers, retail sell-through analytics, tournament licensing calendars and material-cost inputs. Where regulatory or safety events materially altered supplier practices—such as the 2023 impact-testing standard—those events were explicitly modelled. We also incorporated recent industry incidents and supply events into downside scenarios to ensure decision-grade robustness.

This release is intentionally selective: it outlines strategic inflection points, operational levers and competitive dynamics while withholding granular regional and product split figures to protect the proprietary models reserved for subscribers. If your 2026 planning requires: (a) detailed market sizing by region and product; (b) channel‑level revenue projections; (c) supplier scorecards and contactable targets; or (d) customised scenario runs calibrated to your balance sheet—PW Consulting can provide the full report and tailored advisory engagement.

Contact our Industrial Sports Equipment Practice to schedule a briefing of the full Rugby Equipment Market report and a customised workshop on translating these insights into a 90‑day action plan for 2026.

For detailed analysis of this topic, please visit the official page:Rugby Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com