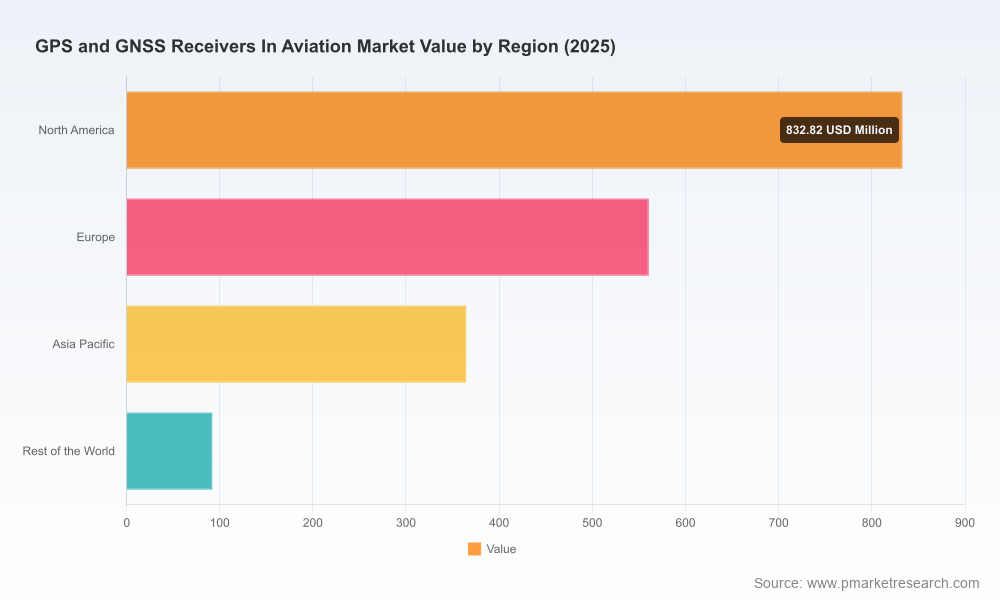

PW Consulting Forecasts Aviation GPS & GNSS Receivers Market to Grow at 6.75% CAGR, Reaching USD 2,922.52 Million by 2032

Technology |

2026-07-01 10:25:13

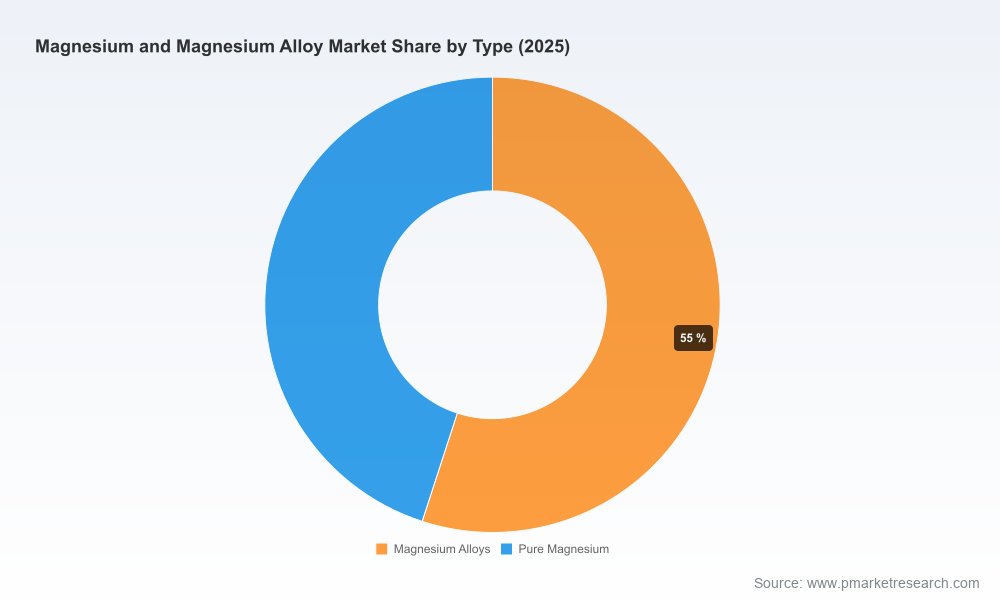

As global manufacturers accelerate lightweighting, electrification and sustainability initiatives, magnesium and its alloys are re-emerging as a strategic material of choice. PW Consulting’s new Magnesium and Magnesium Alloy Market report (base year 2025; forecast period 2026–2032) projects a structurally upward market trajectory at a compound annual growth rate (CAGR) of 6.25%. In monetary terms, the market expands from an estimated USD 5,250 Million in 2025 to roughly USD 8,025 Million by 2032—an expansion that materially alters sourcing, investment and technology priorities for 2026 planning cycles.

Magnesium And Magnesium Alloy Market

Regulatory repositioning. Magnesium’s addition to the USGS 2025 Critical Minerals List crystallizes government attention on domestic sourcing, secure supply chains and strategic stockpiling. This changes procurement calculus and elevates capital allocation to near-market production projects.

Magnesium And Magnesium Alloy Market

Geopolitical supply dynamics. China continues to dominate primary magnesium supply. Estimates place its share of global primary production in the high eighties percentage range, triggering policy-supported investments in Australia, North America and other jurisdictions to reduce dependency.

Magnesium And Magnesium Alloy Market

Market-price signal. Short-term price volatility persists: US import prices for high-purity primary magnesium averaged close to USD 3.13 per pound through late 2025, after an initial downcycle, while European markets experienced material year-on-year fluctuation. Tariff actions—such as the reinstatement of a 25% duty on some Chinese magnesium imports in 2025—generated an immediate market response, with spot prices reacting in the mid-teen percentage range. These shocks are both a risk and a signal for strategic action.

Technology and feedstock shifts. The Pidgeon process and dolomite feedstock remain dominant in certain supply chains, while electrolytic routes, recycling and alternative feedstock projects (including fly-ash recovery) are reaching commercial inflection points. Investors and operators must evaluate technology risk-adjusted returns as part of 2026 capital plans.

Strategic playbooks for procurement and sourcing: decision trees that help corporate procurement and operations teams prioritize supplier diversification, on-shore capacity development and inventory strategies under multiple tariff and demand scenarios.

CapEx vs. Opex frameworks: an investment readiness assessment that compares electrolytic, thermal reduction and secondary (recycling) routes across unit economics, emissions profiles and timelines to first production.

Supply-chain stress-tests: bespoke modelling to simulate the impact of sudden export restrictions, lake-level constraints on brine operations, and rapid demand shifts from key consuming industries (automotive, aerospace, electronics).

Commercial due diligence modules: playbooks and checklists for project finance teams and corporate development units assessing JVs, offtake agreements and strategic minority investments.

Regulatory & policy matrix: actionable guidance for government engagement, incentive capture and tariff mitigation strategies mapped to common corporate profiles.

Price-sensitivity and hedging models: scenario-tested exposure matrices for buyers and sellers to optimize hedging instruments, inventory targets and contractual terms.

The report synthesizes a multi-source evidence base: plant-level capacity and utilization data, trade flow analytics, primary interviews with producers and large integrators, plus macro demand forecasts aligned to automotive, aerospace and electronics production scenarios. Our historical calibration window spans 2020–2025 with the forecasting horizon set for 2026–2032. Core outputs are stress-tested across alternative macro and policy scenarios to ensure robustness for board-level decision frameworks and three-to five-year capital plans.

The market is concentrated but not monopolistic: the top three players account for a meaningful share of market revenue while the top five expand that concentration materially. This concentration underpins both bargaining power and opportunity for differentiated entrants.

US Magnesium LLC (Salt Lake City, Utah, USA — https://usmagnesium.com/): Primary brine-based producer supplying high-purity magnesium for aerospace, automotive and defense. Recent operational adjustments linked to brine intake and lake-level dynamics make its asset operations a focal point for supply continuity risk analysis.

Dead Sea Magnesium Ltd. (Israel): Producer using Dead Sea brine electrolysis, focused on high-purity grades for automotive and industrial applications—positioned where brine chemistry and electrolytic technology intersect.

RIMA Group (Belo Horizonte, Brazil): Thermal-reduction specialist with global die-casting and specialty alloy reach, representing the Latin American production base and export dynamics.

Norsk Hydro ASA (Oslo, Norway — https://www.hydro.com/): Combines alloy production with recycling services, highlighting the growing premium for circular supply strategies in automotive lightweighting programs.

Meridian Lightweight Technologies (Strathroy, Ontario, Canada — https://www.meridian-mag.com/): High-pressure die-caster focused on automotive powertrain and structure components — an example of downstream integration capturing more of the value chain.

Additional strategic names include Magontec, Luxfer MEL Technologies, POSCO, a cluster of large Chinese producers and emerging projects in Australia and North America that are advancing low-carbon or alternative feedstock pathways.

Recent headline developments reinforce strategic themes. In late 2025 and early 2026 we observed: a JV term sheet to develop domestic electrolytic production from Arkansas brine resources; operational filings and infrastructure planning by major brine-based producers to mitigate lake-level constraints; and a multi-hundred-million-dollar financing indication for a commercial plant based on fly-ash feedstock. These developments are not isolated—they are the beginning of a broader rebalancing of supply risk and technology competition.

Re-evaluate supply mix: prioritize a balanced portfolio of primary, recycled and alloy-sourced material to reduce single-supplier and single-route exposure.

Accelerate strategic partnerships: identify JV or offtake partners for projects that de-risk feedstock and technology execution horizons.

Embed policy scenario planning: run procurement and investment decisions against tariff, subsidy and critical-minerals policy outcomes—particularly in North America, Europe and Australia.

Invest in recycling and carbon accounting: buyers will monetize lower scope-3 footprints; producers can capture margin uplift by offering certified low-carbon products and traceability.

Hedge price exposure: use the report’s price-sensitivity modules to set inventory, contract length and strike strategies tied to plausible price-path scenarios.

Pursue targeted M&A: prioritize assets that accelerate technology capability (electrolytic cells, modern die-casting capacity) or provide non-Chinese primary supply optionality.

To convert insight into timing, we map three decision triggers that should prompt immediate action in 2026:

Policy shock: any material change to import tariffs or critical-minerals incentive programs that alters cross-border price differentials and project economics.

Capacity shock: first-mover commissioning of non-Chinese, large-scale primary magnesium plants or rapid scaling of recycling capacity that changes net global supply balance.

Feedstock disruption: constraints in dolomite availability or brine inflows that affect regional primary routes and create localized pricing dislocations.

We translate these triggers into operational playbooks in the full report so leadership teams can set clear ‘if/then’ escalation paths tied to procurement, engineering and finance decision timelines.

For executives and boards planning 2026 budgets and strategic investments, magnesium is no longer a niche materials call; it is a core element of product architecture, supply resilience and sustainability positioning. PW Consulting’s report provides governance-ready tools: scenario-calibrated forecasts, supplier risk matrices, project-level economic comparisons and a clear set of tactical moves that convert market insights into defensible investments.

This preview intentionally highlights the strategic contours and operational levers without disclosing the granular segmentation tables, regional and application splits that are critical for transaction and procurement execution. For the complete datasets, segmentation models, supplier scorecards and downloadable Excel-based scenario tools, please access the full Magnesium and Magnesium Alloy Market report on PW Consulting’s report page.

For detailed analysis of this topic, please visit the official page:Magnesium And Magnesium Alloy Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com