Brugada Syndrome Treatment Market Future Trends

Wellness |

2026-05-27 07:06:55

PW Consulting’s new Prefabricated Security Booth Market report equips executives and procurement leaders with a practical, decision-ready view of a market that is maturing into a highly specialized, value-driven landscape. Our analysis shows the global market expanded from a mid-single‑hundred million USD base in the early 2020s to an estimated USD 642.6 Million in 2025, and we forecast continued growth to roughly USD 933.5 Million by 2032 — a compound annual growth rate (CAGR) of 5.48% across the 2026–2032 forecast horizon. These headline figures understate the strategic complexity behind purchasing, designing and delivering security booths in 2026: rising material costs, tightening ballistic and safety standards, and service-led differentiation are reshaping competitive advantage.

Prefabricated Security Booth Market

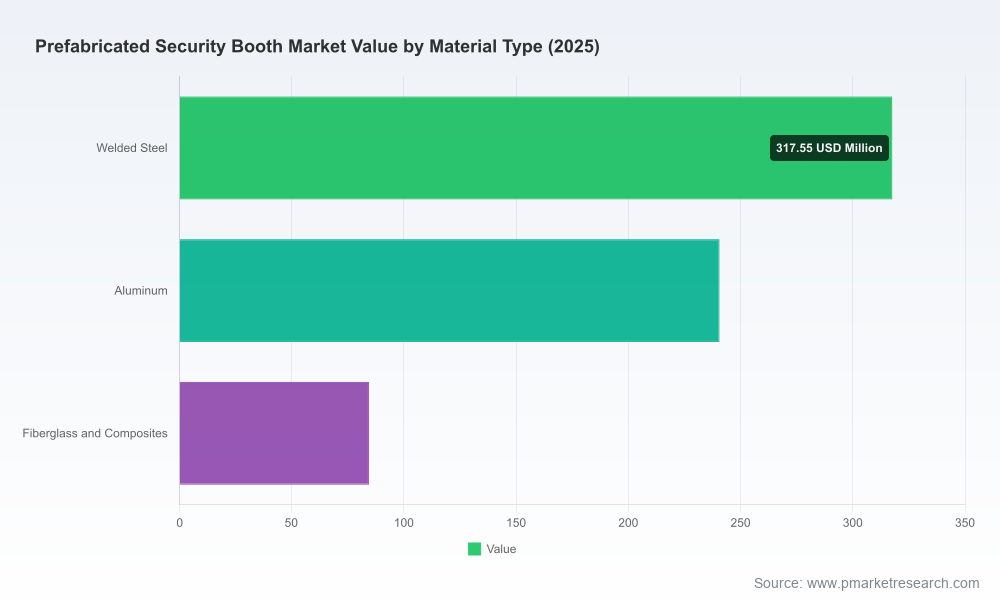

Input-cost pressure is escalating. Steel and aluminum price swings materially influence unit economics and the viability of different material choices; U.S. steel product prices rose sharply into late 2025, and aluminum unit costs have seen pronounced increases amid supply and clean-energy demand shifts. Nonresidential construction input inflation is also compressing margins for modular fabricators.

Prefabricated Security Booth Market

Regulatory and specification complexity is rising for high‑risk applications. Ballistic ratings (UL 752 Levels 1–4), structural standards for steel framing, and facility‑specific codes for critical infrastructure are increasingly mandatory inputs to product design and procurement contracts.

Prefabricated Security Booth Market

Customer expectations are shifting from pure hardware to lifecycle solutions. Buyers now require integrated access control, remote monitoring, rapid deployment, and proven maintenance pathways alongside ballistic or environmental protection offerings.

Actionable market-sizing and scenario forecasts covering 2020–2025 historical performance and 2026–2032 baseline and stress scenarios, enabling CapEx and procurement planning under different inflation and demand trajectories.

Supplier playbooks and decision matrices: comparative profiles for OEMs and systems integrators, vendor selection criteria, lead-time and logistics checklists, and a procurement negotiation toolkit tailored to prefabricated security booths.

Cost model templates that quantify the sensitivity of unit economics to steel and aluminum price movements, labor rates, freight and customs exposure, and finish‑material choices.

Compliance and certification roadmap: a minimum viable checklist for ballistic ratings, structural references, fire and life-safety compliance, and government procurement standards for high‑threat installations.

Go‑to‑market playbooks for manufacturers and solutions providers, including channel strategies, aftermarket service bundles, and digital retrofit pathways for legacy booths.

The prefabricated security booth market remains fragmented: our concentration metrics indicate the three largest firms collectively capture well under one‑fifth of overall revenue, and the top five account for less than one‑quarter. This fragmentation favors companies that can demonstrate specialization, compliance, or cost leadership while enabling room for strategic alliances and roll‑up activity.

Key provider archetypes and representative companies include:

Premium, specification-driven manufacturers — B.I.G. Enterprises: decades-long experience producing bullet‑resistant and code‑compliant booths for Fortune 500s and government agencies. These firms compete on custom engineering, advanced materials and documented performance for high-risk sites.

Modular systems and standard-size specialists — PortaFab and Panel Built: platforms that focus on rapid delivery, a range of standard footprints, and panelized systems that simplify on-site installation. Their value proposition emphasizes speed and predictable specification sets.

Ballistic and high‑security integrators — Delta Scientific, Porta‑King, Kontek Industries: providers whose product lines and engineering processes are tailored towards UL-rated ballistic protection, integrated access-control, and field‑tested security configurations for infrastructure and government work.

Material specialists and export-oriented producers — Mardan Fabrication, Karmod, Austin Mohawk: firms optimizing for material advantages such as aluminum or fiberglass for corrosion resistance and low maintenance in harsh environments, often with international shipping and customization capabilities.

Turnkey and local service players — Guardian Booth, Par‑Kut, Little Buildings, Allied Modular, Speed Space: companies that combine manufacturing with logistics, installation, and aftermarket service, catering to venues that require full lifecycle management (stadiums, airports, hospitals).

For buyers and partners, the strategic implication is clear: alignment to a supplier archetype matters more than price alone. Premium contracts require detailed ballistic certification and program management; high-volume campus deployments prioritize repeatable footprints and service economics.

Hedge material exposure and redesign for material efficiency: Given recent year‑over‑year surges in steel and aluminum costs and construction input inflation, procurement teams should implement indexed pricing clauses, multi‑sourcing strategies, and re-evaluate design tolerances to reduce unnecessary material mass.

Adopt a compliance-first procurement checklist: For high-risk installations, require suppliers to provide third‑party certification evidence (UL 752, ASTM references, or government-specific standards) as part of initial bid packages to avoid costly redesigns.

Differentiate through service and digitization: Manufacturers should productize aftermarket support (SLA tiers, remote health monitoring, predictive maintenance) and offer retrofit kits to convert legacy booths with smart sensors and access-control integration.

Standardize platform footprints for scale while maintaining upgrade paths: Use a two-track product architecture — a set of standardized, fast‑to‑deploy models for volume deployments, and a configurable premium track for ballistic or mission‑critical applications.

Assess nearshoring and inventory buffer strategies: Lock smaller safety stock quantities of critical inputs, qualify regional fabricators, and negotiate shorter lead-time options for mission-critical projects to mitigate global supply volatility.

Integrate lifecycle cost analyses into procurement decisions: Move beyond purchase price to include energy, maintenance, repair, and end‑of‑life disposal (or recycling) costs in vendor scoring.

Explore selective M&A and partnerships: Given the fragmented market structure, strategic bolt‑on acquisitions (service networks, regional installers, component suppliers) can rapidly increase scale and narrow delivery windows.

Risks: Sudden commodity price spikes, changes to import tariffs, and evolving certification standards can create bid‑to‑contract mismatches and margin pressure. Low‑cost imports remain a threat on commoditized, non‑ballistic units.

Opportunities: Retrofit demand for digital and environmental upgrades, growth in transportation and critical‑infrastructure security budgets, and premium contracts tied to ballistic protection and integrated access control represent outsized margin pools.

Near-term triggers to monitor: movements in steel and aluminum pricing, newly published government procurement requirements for sensitive facilities, and major infrastructure project awards in key regional markets.

Our report is designed to be a pragmatic tool: finance teams will find model-ready inputs for forecasting and cost‑sensitivity testing; operations and procurement will get supplier evaluation templates and contract language to protect margins; product and sales leaders will gain go‑to‑market playbooks to segment customers by risk and service intensity. The combination of a quantified market outlook, scenario-tested cost models, and supplier archetype mapping makes the report operationally actionable for the decisions you will make in 2026.

For organizations evaluating suppliers or considering strategic moves, the path forward is straightforward: prioritize compliance and service differentiation, mitigate material exposure through contracting and design, and exploit the fragmented competitive landscape to scale via partnership or targeted acquisitions. PW Consulting’s Prefabricated Security Booth Market report provides the empirical evidence and the tactical templates to execute those strategies efficiently.

PW Consulting has structured the full dataset, proprietary cost models and vendor playbooks to support immediate procurement cycles and FY2026 strategic planning. To access the comprehensive methodology, scenario workbooks, and vendor benchmarking appendices, visit our report page or contact a PW Consulting industry advisor for a guided briefing and customized extracts tailored to your project portfolio.

For detailed analysis of this topic, please visit the official page:Prefabricated Security Booth Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com