Nateglinide Market: Insights, Key Players, and Growth Analysis

Other |

2026-07-03 05:20:24

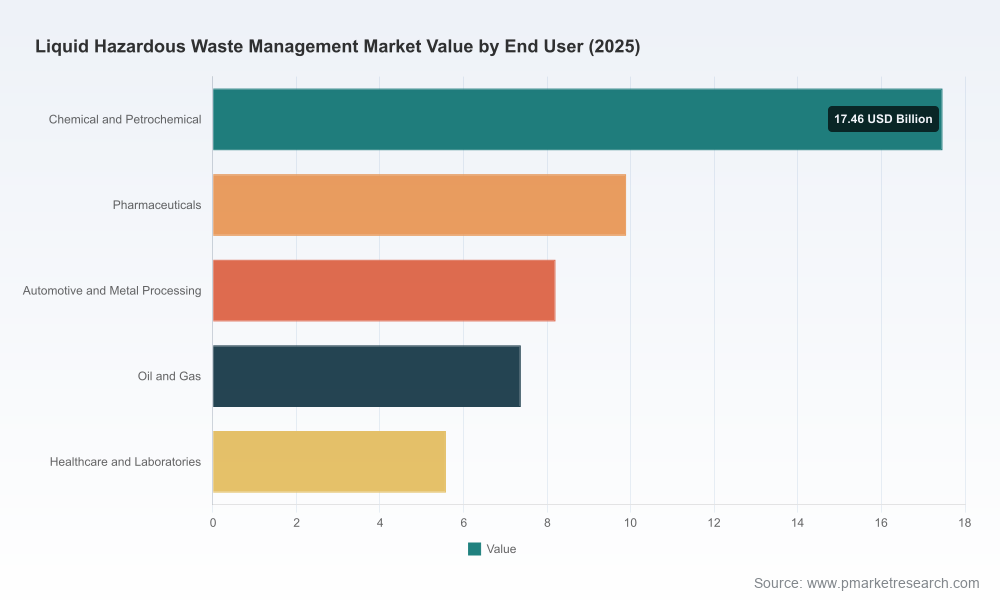

PW Consulting’s latest market intelligence on Liquid Hazardous Waste Management (base year 2025) arrives at a pivotal moment for corporate decision-makers. Global market dynamics that accelerated through the early 2020s continue to reshape operator economics and create new points of strategic leverage. Our analysis shows the market expanded from approximately USD 36 billion in 2020 to USD 48.5 billion in 2025 and is forecast to grow at a compound annual growth rate (CAGR) of 6.08% across the 2026–2032 horizon — reaching an estimated USD 73.34 billion by 2032. These headline figures set the commercial context for investments, outsourcing decisions, and regulatory compliance planning in 2026.

Liquid Hazardous Waste Management Market

Measured, predictable growth — The market’s steady CAGR masks important structural shifts: clients face tighter environmental regulation, legacy disposal routes are under pressure, and new treatment technologies are altering cost curves. Organizations that understand the intersection of regulation, capacity, and technology will be able to convert compliance obligations into competitive advantage.

Liquid Hazardous Waste Management Market

Fragmentation offers transaction upside — Despite the scale of the overall market, concentration remains low (CR3 ~18.5%, CR5 ~27.4%), leaving the sector open to consolidation. Corporates and private equity investors looking to build regional scale or capability-led platforms can still acquire attractive assets at relative multiples.

Liquid Hazardous Waste Management Market

Operational and financial exposure — Liquid streams are often high-frequency, high-cost operational inputs for industrial generators. Strategic choices around capex versus outsourcing, the siting of treatment capacity, and contingency planning for manifesting and transport are now central to resilience planning.

This report is built for action. It goes beyond market sizing to provide executable guidance for boardrooms and operational teams tasked with 2026 strategy execution. Key practical deliverables include:

Operational playbooks for liquid hazardous waste management covering collection logistics, transport contracts, interim storage, and selection of treatment pathways (thermal treatment, physico-chemical, resource recovery, engineered injection where applicable).

Capital planning models with scenario-driven NPV/IRR outputs for greenfield treatment facilities, brownfield upgrades (e.g., high-temperature incineration), and modular mobile treatment options. Models are parameterized so executives can run “what-if” analyses against fuel, labor, and regulatory cost shocks.

Procurement and outsourcing decision frameworks that align total cost of ownership with compliance risk appetite — including templates for contingency sourcing when regional capacity constraints emerge.

Regulatory impact simulations: quantitative assessment of proposed and pending regulations (including electronic manifests and international shipment amendments) on operating costs, turnover times, and cross-border routing.

Vendor diligence packages and M&A playbooks: valuation comparables, integration checklists, earnout structures tied to capacity utilization, and post-merger modernization roadmaps.

Technology roadmaps assessing the maturity, capital intensity, and operating economics of incumbent and emergent treatments — enabling prioritized R&D and capex allocation.

The report’s competitive analysis profiles market participants across capability, footprint, and strategic orientation. Key themes include scale players expanding through acquisition, specialist firms deepening technical capabilities for complex streams (including mixed radioactive liquids), and regional operators competing on speed and local compliance expertise.

Veolia Environnement SA — A global integrator with deep thermal-treatment and recycling assets, aggressively expanding in the U.S. via acquisitions and high-temperature capacity projects. Veolia’s strategy reinforces the value of integrated networks that combine collection, transport, and centralized treatment to manage throughput volatility.

Clean Harbors, Inc. — North America’s large-cap services provider with entrenched emergency-response and industrial services capabilities. Its fleet-based collection model and emergency response positioning make it a preferred partner for industrial generators seeking turnkey solutions.

Waste Management, Inc. and Republic Services, Inc. — Large North American players leveraging scale and logistics to offer comprehensive hazardous and non-hazardous liquid waste services; both are active in technology trials and selective M&A.

SUEZ (Veolia) and Tradebe — European-rooted specialists providing integrated treatment and recycling services with cross-border capabilities important for multinational generators facing international shipment constraints.

Stericycle, Covanta, GFL, Heritage-Crystal Clean, US Ecology (now integrated into larger platforms), Perma-Fix, and sector specialists such as Liquid Environmental Solutions — these firms add technical depth (medical/regulatory compliance, energy-from-waste integration, mixed radioactive waste handling, and mobile treatment services) that address niche but high-margin segments.

Recent industry moves underscore the strategic calculus: major acquisition activity and capacity augmentations in 2025–2026 demonstrate how incumbents are securing feedstock access and treatment headroom ahead of tightening regulations and municipal permitting challenges. Notable developments include a multi-billion-dollar acquisition to scale U.S. operations, expansions of high-temperature incineration capacity, and permitting wins that materially increase processing throughput for complex liquid streams.

Regulatory changes in 2025–2026 are reshaping workflows and capital allocation. Highlights that every corporate strategist must track include:

Transition to electronic manifests — regulators are moving to digital-only manifesting systems with defined compliance windows. This reduces administrative friction but increases compliance visibility and auditability; firms must invest in data integration and traceability to avoid penalties and to leverage manifest data for operational optimization.

Expanding classifications and shipment constraints — treaty amendments and rulemakings affecting electronic and electronic-component waste impact cross-border logistics; generators and service providers must reassess transshipment routes and contractual commitments.

State-level moratoria and permitting uncertainty — select jurisdictions proposing moratoria on new or expanded facilities elevate the strategic value of existing permitted capacity and local partnerships, and strengthen incentives for facility upgrades over new builds.

Organizations that act now can convert compliance costs into strategic differentiation. Our recommended actions fall into three horizons:

Immediate (0–12 months): shore up compliance and continuity. Validate manifesting systems, secure contingency contracts for overflow treatment, and conduct a rapid risk-mapping of generator sites against regional capacity constraints and anticipated regulatory changes.

Near-term (12–36 months): optimize operational footprint and partnerships. Prioritize investments in contracts or minority stakes with permitted facilities, negotiate volume-guarantee clauses with price collars, and pilot modular/mobile treatment units where permitting timelines impede fixed-capacity expansion.

Medium-term (36+ months): pursue capability-led consolidation. Use targeted acquisitions to acquire technical capabilities (e.g., solvent recovery, mixed-rad waste processing) or geographic access, and align R&D investments with decarbonization and circularity objectives that can unlock recycled solvent markets.

Our research transforms public signals — regulatory filings, company disclosures, permitting records, and transaction activity — into actionable scenarios and quantified stress-tests for corporate strategy. The report provides: benchmarking dashboards, executable M&A playbooks, and a decision-support toolkit that links operational KPIs to shareholder outcomes.

Importantly, while this preview communicates high-level trajectories and strategic options, the full report contains the granular segmentation, regional dynamics, treatment-method economics, and per-segment forecasts needed to quantify opportunity and risk at facility and portfolio level. To preserve the commercial utility of that granular intelligence, we have intentionally withheld proprietary subsegment tables and region-by-application breakdowns from this summary. Clients and subscribers can access the complete datasets, proprietary models, and company valuation decks through PW Consulting’s report portal.

As firms plan budgets and capital allocation for 2026, three priorities should guide decision-making: secure access to permitted treatment capacity, invest in digital traceability to meet evolving manifest and reporting obligations, and evaluate consolidation targets that close capability gaps. The market’s steady growth and low concentration create abundant strategic options — but the timing of regulatory changes and the pace of capacity investments will determine which players capture margin expansion.

PW Consulting’s Liquid Hazardous Waste Management Market report equips executives with the scenario-based frameworks and models necessary to make those choices with confidence. For access to the full forecast tables, segment-level economics, and transaction-level insights, please consult the report on our website.

For detailed analysis of this topic, please visit the official page:Liquid Hazardous Waste Management Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com