PW Consulting: Strategic Brief — RF EAS Label Market 2026 Outlook

Executive summary

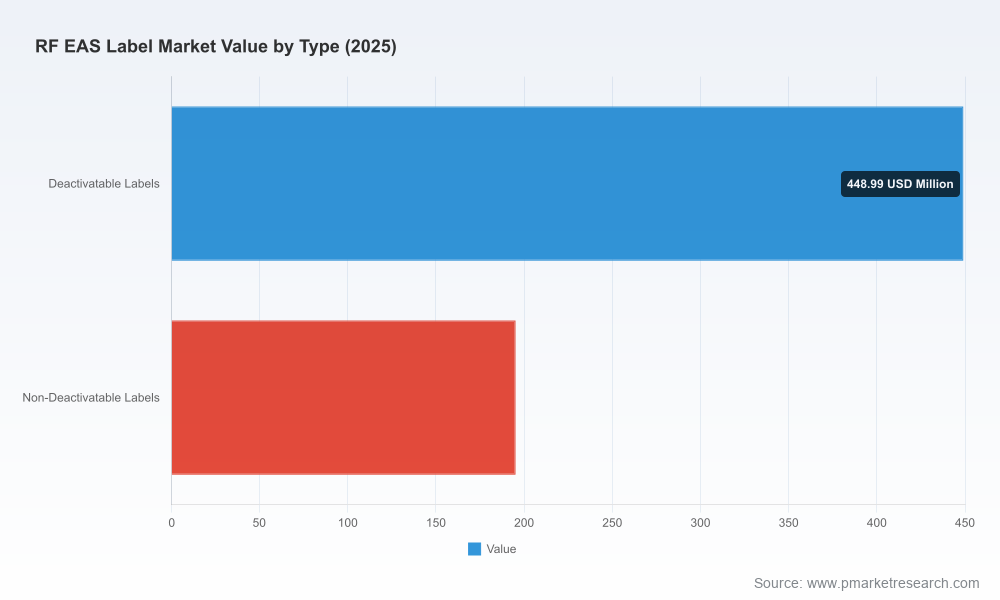

PW Consulting’s new RF EAS Label Market report (base year 2025; historical analysis 2020–2025; forecast 2026–2032) synthesizes commercial, technical and regulatory vectors that will inform procurement, product and M&A choices in 2026. The global RF EAS label market—measured in USD Million—stood at USD 644.11 Million in 2025 and is projected to reach USD 692.03 Million in 2026, continuing along a multi-year trajectory supported by a compound annual growth rate (CAGR) of 3.99% through the 2026–2032 forecast window. That steady expansion belies substantial structural change: platform convergence (RF EAS + RFID + cloud operations), regulatory pressure on packaging components, and an accelerating battle against organized retail crime using metallurgical countermeasures.

Rf Eas Label Market

Why this report matters for 2026 decision-making

- Timing: 2026 is the inflection year when cloud orchestration of loss-prevention devices and POS-integrated detection begin shifting capital and operational priorities. Suppliers who migrated to cloud-first platforms in 2024–25 are now converting pilots to scaled rollouts.

- Risk and compliance: Extended Producer Responsibility (EPR) schemes and the EU’s Packaging and Packaging Waste Regulation (PPWR) are changing packaging-cost math. Our analysis maps how EPR dynamics affect label design, supplier selection and total cost of ownership (TCO).

- Competitive advantage: Early adopters of integrated architectures (antenna + checkout + store ops) capture not only shrink reduction but measurable labor and inventory benefits. The report quantifies the decision levers and the thresholds at which investment in higher-cost, higher-performance labels and systems becomes accretive to margins.

Market trajectory — what the headline numbers hide

The headline CAGR of 3.99% across 2026–2032 reflects a market shifting from volume-driven replacement toward value-driven upgrades. While the market value increases year-on-year in absolute USD Million terms, the drivers of growth vary: product innovation in metal-detection and micro-labels, software-enabled service offerings, and regulatory tailwinds that re-price packaging components. Importantly, concentration metrics indicate a market with meaningful scale advantages: the top three vendors account for a sizeable share while the top five increase that dominance further, a dynamic that creates both barriers and opportunities for nimble entrants and specialists.

Rf Eas Label Market

Report contents — practical, actionable intelligence

- Methodology and validated market sizing: transparent assumptions, scenario runs and sensitivity testing for 2026–2032.

- Commercial playbooks: procurement scorecards, supplier negotiation templates, and deployment roadmaps tailored to retailers, brand manufacturers and label converters.

- Technology matrices: comparative assessment of label architectures (including metal-resistant designs, micro labels and source-applied solutions), detection performance, and integration complexity with POS and RFID systems.

- Regulatory and sustainability toolkit: EPR impact modeling, design-for-recyclability checklists, and a compliance roadmap aligned to current US state laws and EU PPWR trajectories.

- Vendor evaluation and partnership framework: an independent rubric to assess commercial fit, manufacturing footprint risk, and product roadmap alignment without disclosing proprietary segment-level volumes.

- Investment guidance: acquisition targets, coalition strategies (co-development, licensing) and financial thresholds for in-market scale-up versus outsourcing.

Competitive landscape — players, positioning and recent moves

The market comprises global incumbents with vertically integrated portfolios and regional specialists focused on cost, customization and rapid innovation. PW Consulting’s assessment highlights different strategic postures among core players:

Rf Eas Label Market

- Checkpoint Systems (Division of CCL Industries): A clear platform player with extensive in-house manufacturing and a wide portfolio spanning grocery to apparel. Recent initiatives show a push toward systems integration—most notably the launch of cloud-based store operations and the introduction of a POS-integrated antenna solution—signaling a move from component supplier to systems provider.

- ALL-TAG Corporation: North American-focused manufacturer known for source tagging and high-shrink-item solutions. Its strength lies in customizable formats and compatibility with major ecosystems—positioning it well for partnerships with apparel and hard-goods retailers prioritizing loss prevention at origin.

- Hangzhou Century Co., Ltd.: Aggressive innovation cadence in flexible circuit soft labels and metal-detection systems. Product introductions and trade-show presence in early 2026 underscore ambitions to address both everyday shrink and organized retail crime (ORC) challenges with metal-aware detection solutions.

- All4Labels Global Packaging Group: A global converter offering customized RF labels and hard tags; its value proposition centers on packaging expertise and multi-tech support (AM + RF), serving clients that seek single-supplier simplicity for labeling and security.

- Emerging Chinese manufacturers (Novatron Electronics, Alien-Security, Nanjing Bohang): These players compete primarily on cost, speed-to-market and flexible production. Their investments in etching, die-cut and anti-shielding variants are lowering technical entry barriers for retailers with tight cost targets.

Tactical implications: the market’s CR3 and CR5 concentration levels mean scale and integration capabilities matter—buyers should assess supplier roadmaps for cloud and POS integration, geographic manufacturing resilience, and sustainability compliance to avoid downstream cost shocks.

Market dynamics and headwinds

- Materials and supply chain: RF EAS soft labels typically rely on paper substrates with embedded aluminum or copper circuits to form resonant antennas at ~8.2 MHz. These inputs create a predictable but politically sensitive supply chain; volatility in metallurgical prices and recycling requirements will shape unit costs and material choices in 2026.

- Regulatory pressure: EPR schemes and packaging regulations are not uniform—jurisdictional variation (including recent US state-level enactments) forces manufacturers and brands to evaluate end-of-life responsibilities, reporting obligations and potential fee structures. Early compliance planning is essential to avoid retrofitting costs.

- Technology convergence: The integration of RF EAS with RFID and cloud-based store operations is altering vendor economics. Hardware margins compress, but recurring revenue streams from software and managed services create higher lifetime value for suppliers that execute.

- Security sophistication: Organized retail crime (ORC) is leading to demand for metal-resistant detection and “anti-shielding” label variants. Products that combine detection fidelity with manufacturability will command premium positioning.

Actionable recommendations for 2026

- Retailers — Pilot integration, then scale: Run a 6–12 month pilot that couples POS-integrated antennas with cloud store operations in high-shrink formats; measure shrink, throughput and labor delta before enterprise rollout.

- Brands and converters — Re-evaluate design-for-recyclability: Update label specifications to meet anticipated EPR scoring; select substrates and adhesives that reduce end-of-life fees and simplify recycling streams.

- Suppliers — Productize services: Move beyond unit sales. Bundle detection hardware with analytics and managed services to create recurring revenue and stickier client relationships.

- Investors and M&A teams — Look for capability gaps: Targets should provide either differentiated metal-detection IP, scalable source-tagging solutions, or cloud operational assets that accelerate platform adoption.

- Procurement — Stress-test supplier resilience: Incorporate material substitution clauses and compliance warranties in contracts to mitigate EPR exposure and metal-price risk.

What the full report provides (and why you should read it)

The full PW Consulting report contains the granular models, segment breakdowns, vendor scorecards and a downloadable ROI calculator that translate the headline USD Million market view and CAGR into program-level business cases. In line with our “trailer” approach, this brief demonstrates the analytic depth and actionable orientation of the work while preserving the detailed segmentation and proprietary forecasts for the report itself.

Next steps

- Decision-makers: use this brief to align 2026 budgets to the market inflection points identified above—particularly integration pilots and EPR compliance workstreams.

- Procurement and technology teams: request the vendor evaluation toolkit from PW Consulting to accelerate supplier selection and deployment plans.

- Investors: engage PW Consulting for a confidential briefing that overlays our market model onto target company financials and integration roadmaps.

PW Consulting’s RF EAS Label Market report is designed as a practical guide for 2026 strategy: it balances empiric market sizing (USD Million and CAGR), competitive intelligence, technology assessment and regulatory foresight to help organizations act with confidence in a market that is growing modestly in value but rapidly in complexity. For access to the full dataset, proprietary segment-level forecasts, and our vendor scorecards, please visit the report landing page or contact PW Consulting for a briefing.

For detailed analysis of this topic, please visit the official page:Rf Eas Label Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com