Desktop Plasma Cleaner Market: Strategic Imperatives for Enterprises Entering 2026 — PW Consulting Market Brief

Executive snapshot

As PW Consulting’s Senior Strategic Consultant and Chief Industry Analyst, I present a focused briefing on our newly published Desktop Plasma Cleaner Market study (base year 2025, historical review 2020–2025, forecast 2026–2032). The market for desktop plasma cleaners is on a measured, durable growth path — expanding at a compound annual growth rate (CAGR) of 6.5% through the forecast window. From an estimated market size in 2025 of USD 275.5 Million (USD, Million), the market is projected to transition into a larger, more commercially integrated segment by 2032 — a trajectory that will materially affect procurement, R&D prioritization, and supply-chain decisions in 2026 and beyond.

Desktop Plasma Cleaner Market

Why this market matters to enterprise decision-makers in 2026

- Operational leverage for high-mix, low-volume manufacturing: Desktop plasma cleaners are now critical for surface activation, contaminant removal, and sample preparation across electronics, medical devices, and R&D environments. Their role is expanding from bench labs into localized production nodes where fast, repeatable surface treatment is a differentiator.

- Capital-light process optimization: With clear improvements in uptime, modularity, and process gas control, desktop units provide a lower-cost route to process qualification compared with larger vacuum systems — enabling product teams to accelerate prototypes to pilot runs without outsized capex.

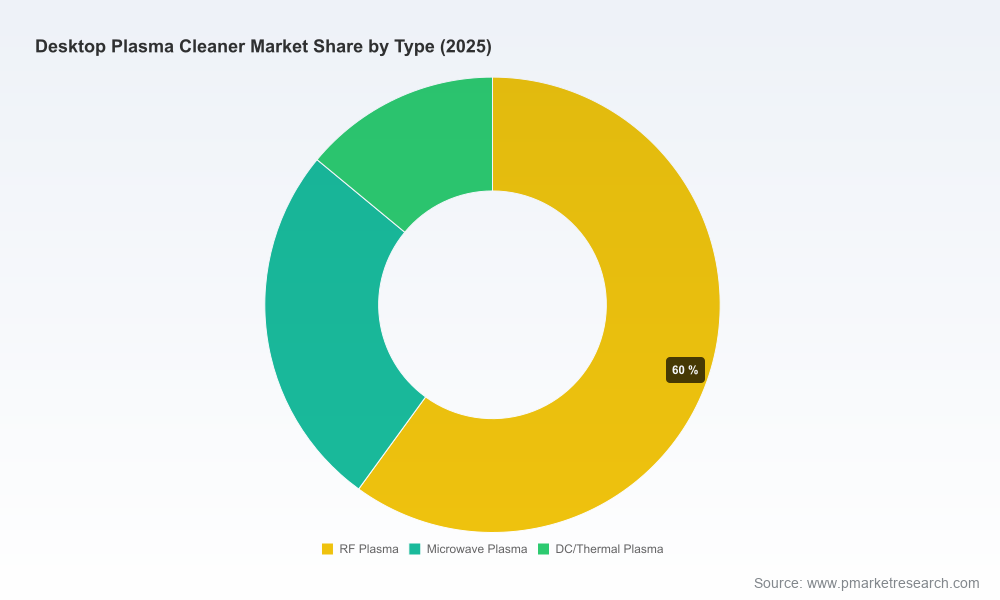

- Supplier strategy and risk mitigation: The vendor base is fragmented but maturing. Leading vendors hold a meaningful share of the market while many regional and niche suppliers address specialized needs. This dynamic creates opportunities for dual-sourcing, supplier consolidation, and strategic partnerships in 2026.

Market trajectory — what the numbers tell us (high-level)

Our analysis traces compound growth that reflects continued adoption in semiconductors, medical/biotech, and academic/research users. The market expanded steadily from the early 2020s into 2025 and is forecast to continue its ascent through 2032. For commercial planners, the implication is clear: component procurement cycles, equipment qualification timelines, and vendor roadmaps should be re-aligned to a market expanding at mid-single-digit CAGR and moving toward broader commercial adoption rather than remaining a purely laboratory-centric technology.

Desktop Plasma Cleaner Market

Report practical contents — what’s inside and how it helps

This study is constructed to be operationally useful for decision-makers who need to move quickly from insight to action. Core deliverables include:

Desktop Plasma Cleaner Market

- Market sizing and forecast model (2020–2032) with scenario analyses for adoption rates under conservative, base, and accelerated commercialization cases.

- Action-oriented buyer guides: procurement checklists, TCO (total cost of ownership) frameworks, and template technical specifications to accelerate vendor evaluation cycles.

- Competitive mapping and supplier shortlists: vendor profiles, capability matrices, and suggested sourcing strategies by functional need (R&D, microscopy prep, pilot production).

- Technology and process deep-dive: component-level risks (e.g., chamber metallurgy, RF power supplies), common process gases and chemistries, and operational best practices for throughput and reproducibility.

- Regulatory and standards overview: compliance considerations impacting procurement and deployment in laboratory and industrial settings.

- Investment and M&A vantage: strategic criteria for identifying targets and areas where bolt-on acquisitions or partnerships can accelerate market entry.

Competitive landscape — how providers are differentiating

The desktop plasma cleaner market exhibits a mix of long-established specialists, regionally focused manufacturers, and new entrants with niche propositions. The market concentration is moderate: the top three vendors account for a material portion of revenue, and the top five collectively increase that share, signaling room for both consolidation and continued competition.

- Established laboratory specialists (e.g., long-standing US and European vendors) leverage decades of product refinement and channel relationships with research institutions. Their strength is reliable product operation, documentation for compliance, and mature after-sales support.

- Regional and high-volume manufacturers, especially from Asia, are focusing on cost-performance trade-offs and rapid delivery for OEM and production-oriented buyers. These firms are increasingly visible on global supplier shortlists and are investing in quality systems to meet international buyer requirements.

- Technology-focused vendors distinguish on tabletop ergonomics, modularity, and user experience — enabling non-expert operators to achieve repeatable surface treatments with minimal ramp-up time.

Key names evaluated in the study include long-time laboratory incumbents, European engineering specialists, and several Asia-based producers that have increased market visibility through product positioning and distributor partnerships. Recent vendor movements — including manufacturer rankings updates and publicized product references — suggest an active market where positioning and channel strategies will be decisive in 2026.

Dynamics shaping the market (what executives must monitor)

- Materials and components: Desktop systems commonly utilize stainless-steel chambers and RF power supplies operating at established industrial frequencies. Availability and cost of these components, together with supply-chain lead times for critical electronics, directly influence delivery and pricing strategies.

- Process gas economics and supply: Oxygen, argon, and gas mixtures remain the practical workhorses for surface cleaning and activation across polymers, metals, and elastomers. Gas handling requirements, purity, and safety protocols influence both capital design and operating expenditure.

- Standards and certification: Compliance with quality and safety standards remains an important purchase criterion for institutional and industrial buyers. ISO systems and CE compliance are increasingly table stakes for suppliers seeking global market access.

- Application pull: Adoption is driven by concrete use-cases — from microscopy sample prep (SEM/TEM/FIB) to medical-device bonding and small-batch electronics assembly. These application drivers shape product requirements such as chamber size, process recipes, and automation interfaces.

Strategic implications and recommended actions for 2026

To translate the market outlook into defensible advantage, PW Consulting recommends a set of prioritized actions for enterprises considering investment, procurement, or partnerships in desktop plasma technologies.

- Align procurement cycles to forecasted adoption curves: Move from ad-hoc buys to a structured sourcing program that includes vendor qualification, lifecycle cost modeling, and service-level agreements.

- Design dual-sourcing strategies for critical processes: Given supplier diversity, pairing a leading specialist with a competitive regional supplier mitigates geopolitical and logistics risk while preserving quality standards.

- Invest in process reproducibility before scale: Standardize process recipes and validation protocols centrally so that desktop units deployed across sites deliver consistent outputs — a key requirement for distributed manufacturing models.

- Prioritize interoperability and automation readiness: For buyers planning to integrate plasma units into production lines, select units with available communication interfaces, recipe management, and automation-friendly footprints.

- Consider targeted partnerships or bolt-ons: For OEMs and capital equipment companies, evaluating tuck-in acquisitions that add desktop plasma capabilities can shorten time-to-market for surface-treatment offerings.

Risk matrix — what can derail plans

Risks that merit attention include component supply bottlenecks (power electronics and vacuum seals), inconsistent quality from lower-cost suppliers, and evolving regulatory expectations in medical and semiconductor markets. Our report includes mitigation blueprints for each risk, with suggested contract language and qualification test plans tailored for 2026 procurement cycles.

Actionable 12–18 month plan (concise roadmap)

- Month 0–3: Execute a rapid supplier shortlisting using PW Consulting’s procurement checklist and minimum technical specification template.

- Month 3–6: Run parallel pilots with at least two differentiated vendors (one incumbent specialist and one competitive regional supplier) focusing on throughput, repeatability, and operator training time.

- Month 6–12: Consolidate supplier contracts with SLAs for uptime and support; roll out standardized process recipes and qualification documentation across pilot sites.

- Month 12–18: Scale deployment into production-adjacent nodes, leverage lessons learned to refine TCO models, and evaluate strategic acquisition targets if rapid vertical capability is required.

What the full PW Consulting report unlocks

The published study is structured to move executives from hypothesis to tactical execution. It includes downloadable models, supplier scorecards, procurement templates, and validated scenario-based forecasts. Importantly, for organizations that require confidential briefings or bespoke modules (for example, IP-led deployment strategies or region-specific sourcing roadmaps), PW Consulting offers customized workshops and decision-support sessions to translate the study’s insights into executable programs.

Closing — the opportunity for 2026

The desktop plasma cleaner segment is transitioning from a niche lab tool into an enabling technology for distributed microfabrication, advanced assembly, and high-fidelity sample preparation. With a projected mid-single-digit CAGR and a step-change in adoption across R&D and small-batch production, 2026 is a pivotal year for companies to define their approach: accelerate through procurement and process standardization, or risk ceding operational leverage to more agile competitors.

PW Consulting’s Desktop Plasma Cleaner Market study equips leaders with the market intelligence, operational templates, and competitive insight required to make those choices with confidence. For a full breakdown of methodologies, scenario models, and our vendor scorecards, consult the comprehensive report and contact PW Consulting for a tailored advisory engagement.

For detailed analysis of this topic, please visit the official page:Desktop Plasma Cleaner Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com