How the US CRISPR and Cas Gene Market Is Accelerating Precision Medicine Breakthroughs

Health |

2026-07-03 07:14:05

As global material handling, robotics, and automated logistics architectures accelerate their shift toward higher-density facilities, omni-directional wheel technologies are moving from niche enablers to mission-critical components. Our new Omni Wheel Market Report (base year 2025) synthesizes quantitative market trajectories and qualitative competitive intelligence to arm corporate leaders with the insights required to make high-stakes 2026 decisions on sourcing, product roadmaps, and inorganic growth.

Omni Wheel Market

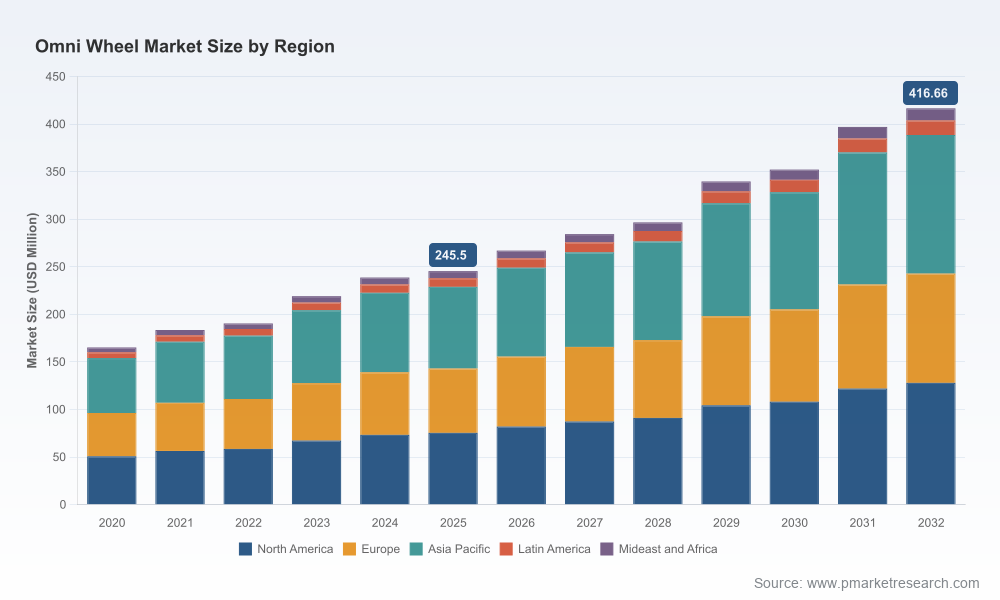

The omni wheel market has demonstrated steady expansion through the 2020–2025 historical window, reaching a total market size of approximately USD 245.5 Million in 2025. Our forecast extends from 2026 through 2032 and models continued growth driven by the densification of automation and last-mile intralogistics requirements. The market is expected to advance at a compound annual growth rate (CAGR) of 7.85% across our forecast period, taking the market beyond the mid-point of the decade and reinforcing omni wheels as a structurally growing category. This trajectory underscores a clear signal: 2026 will be a critical operational and financial planning year for OEMs, system integrators, and material-handling end-users.

Omni Wheel Market

Strategic market outlook: A calibrated, scenario-based forecast for 2026–2032 that connects macro adoption drivers (automation, AGVs, compact warehousing) to realistic supplier capacity and demand-side constraints.

Omni Wheel Market

Procurement playbook: Bid templates, total cost of ownership (TCO) calculators, and contract clauses tailored to omni wheel procurement — including guidance on volume bands, lead-time hedging, and clause language to allocate raw-material inflation risk.

Supplier benchmarking toolkit: A reproducible scorecard to evaluate manufacturers and distributors across technical robustness, materials traceability, IP posture, lead-time reliability, and aftermarket support.

Engineering & materials dossier: Practical guidance on material selection (with a focus on engineering polymers such as Polyoxymethylene/POM), manufacturing considerations (injection molding best practices), and trade-offs between light- and heavy-duty designs for defined life-cycle targets.

Use-case ROI models: Ready-to-run models that quantify ROI for retrofits and greenfield installations across representative automation scenarios — enabling rapid board-level decision making with material sensitivity analyses.

M&A and partnering playbook: A decision framework for identifying bolt-on acquisition targets, licensing opportunities, and strategic distribution partnerships that can immediately improve route-to-market.

Automation density and spatial optimization: Customer demand is increasingly concentrated in environments where 360° maneuverability materially improves throughput per square meter. The adoption curve for omni wheels is being pulled by integrators seeking smaller turning radii, more flexible layout changes, and reduced conveyor complexity.

Material supply & cost pressure: Omni wheels are predominantly manufactured from engineering polymers, notably Polyoxymethylene (POM), via injection molding. Recent pricing data in April 2026 indicates meaningful uplifts (for example, material price points in major regions have risen year-over-year), amplifying the need for procurement-led hedging strategies and design-level material efficiency reviews.

Ergonomics and regulation: The ergonomic advantages of omni wheels (more intuitive, safer manual handling interfaces and improved control in assisted-carry systems) are translating into regulatory acceptability and, in some sectors, preferential procurement. Buyers should map these ergonomic advantages to risk-reduction KPIs as part of supplier evaluations.

Concentration and competitive structure: The market exhibits moderate concentration — the top three players account for a notable share of sales and the top five materially expand that footprint. This structure creates both opportunities and risks: a defined set of suppliers simplifies supplier rationalization strategies while also creating potential single-source vulnerabilities for critical OEMs.

Our competitive analysis focuses on technology leadership, channel models, and the degree to which companies have translated product IP into scalable commercial models. Highlights from our assessment include:

Innovative polymer-based manufacturers with vertical IP (example: patented multi-directional designs and full injection-molded polymer constructions) continue to set performance and durability benchmarks. These companies are prime partners for high-spec industrial and mission-critical applications, but their pricing and lead-time dynamics must be modeled into TCO calculations.

Distributors and systems-focused firms that bundle omni wheels with motors, controllers, and educational kits play a strategic role in expanding addressable demand. Their reach into educational and light-industrial segments accelerates adoption and can serve as a low-cost testbed for new product iterations.

Regional suppliers with tailored product lines for local markets offer speed-to-market advantages. However, for global platform OEMs, variability in material specifications and finish standards requires a harmonization layer in procurement contracts to prevent integration surprises during ramp-up.

Manufacturers with deep polymer injection-molding expertise and patented wheel architectures are positioned to capture premium industrial applications. Their presence at major trade events and recent product portfolio refreshes indicate a shift from proof-of-concept sales toward scalable commercial deployments.

Distributors and robotics kit providers are lowering the barrier to adoption in education and lab environments, seeding future commercial demand while offering system integrators a broad component set for rapid prototyping and small-batch projects.

Smaller specialized suppliers remain critical to niche segments and can be attractive acquisition targets for larger OEMs pursuing faster entry into specific geographies or application verticals.

Raw-material volatility: Given recent rises in engineering polymer prices, buyers should implement a two-layer mitigation: (1) short-term procurement hedges and consignment agreements with key suppliers; (2) mid-term design reviews aimed at material reduction and substitution where performance permits.

Supply-concentration risk: With a moderate CR3/CR5 profile, companies should avoid over-reliance on a single supplier for scale deployments. We recommend diversifying supplier bases across technology clusters (proven polymer-molding vendors, specialist material science partners, and regionally agile assemblers).

Integration complexity: Omni wheels change system dynamics (traction models, swivel control, wear patterns). Early-stage integration pilots that combine mechanical, controls, and maintenance workflows reduce go-live friction and produce replicable operational playbooks.

For procurement leaders: Use our TCO models and supplier scorecards to renegotiate multi-year contracts before the next procurement cycle closes. For R&D and product leaders: Apply the engineering dossier to right-size wheel selection and material choices for target life-cycle costs. For M&A teams: Filter potential targets using our acquisition criteria to prioritize bolt-ons that close capability gaps, shorten innovation timelines, or open preferred distributor channels.

Product introductions and trade show activity by leading manufacturers in late 2024–2026 demonstrate the transition from laboratory innovation to commercial scaling. These platform launches are being aligned with broader automation shows and logistics exhibitions, underscoring market readiness.

Price movements in core feedstock materials have made sourcing strategies a determinative factor for margin management in 2026. Buyers who lock favorable terms or adopt substitution strategies will materially outperform peers on gross margin preservation.

Regulatory and safety advantages tied to ergonomic materials handling are beginning to influence procurement specs in industries sensitive to workplace injury rates, accelerating the inclusion of omni wheels in bidding requirements.

Omni-directional wheel technology is no longer a marginal choice — it is a component-level lever that can unlock higher throughput, lower OPEX in constrained spaces, and differentiated service propositions for automation providers. The 2026 planning horizon will separate organizations that treat omni wheel selection as an engineering detail from those that fold it into their strategic footprint, supplier strategies, and capital allocation plans. Our report provides the pragmatic tools and strategic framing to ensure your organization selects and scales the right omni wheel solutions with confidence.

This article is a strategic preview. To access the complete dataset, detailed supplier profiles, segmented demand models, and proprietary ROI calculators, consult the full Omni Wheel Market Report available from PW Consulting. The full report contains the granular segmentation and supporting exhibits necessary to operationalize the guidance summarized here.

For detailed analysis of this topic, please visit the official page:Omni Wheel Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com