Waist-Level Viewfinder Market: Strategic Preview for 2026 Decision-Makers

PW Consulting — Executive press release based on the Waist Level Viewfinder Market report (Base year: 2025)

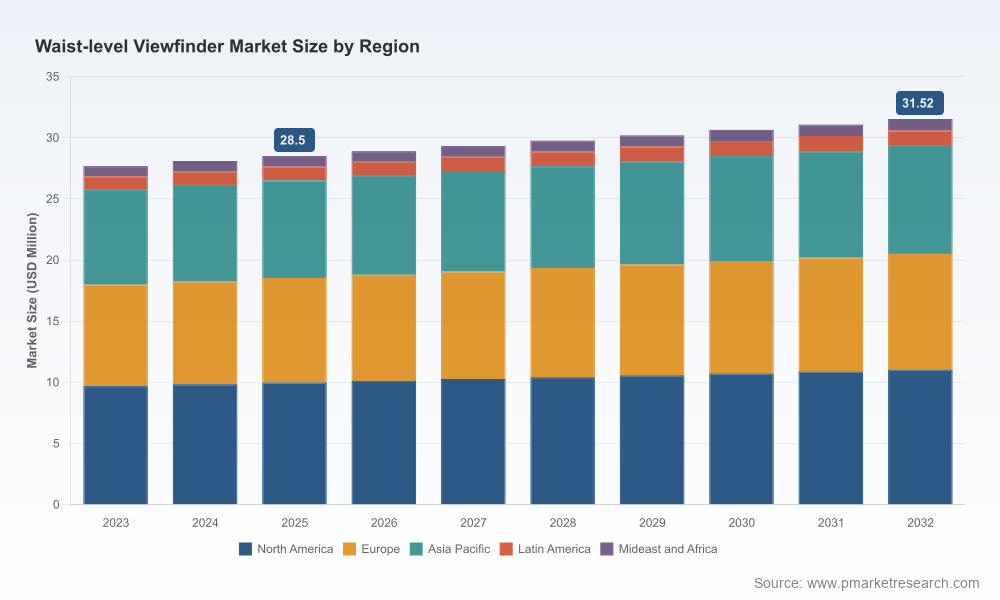

As camera manufacturers and specialist accessory makers balance nostalgia-driven product moves with pragmatic commercial pressures, PW Consulting’s latest Waist Level Viewfinder Market study delivers a timely, decision-oriented intelligence pack for 2026. The global market — measured in USD Million and modelled from a five-year historical base (2020–2025) into a 2026–2032 forecast horizon — sits in a phase of steady, modest growth. After reaching USD 28.5 Million in our 2025 baseline, the market is projected to expand at a compound annual growth rate (CAGR) of 1.45% through the forecast period, arriving at the high‑single‑tens million range by 2032. This measured trajectory and the market’s concentrated supplier structure create a strategic landscape where targeted moves generate disproportionate returns.

Waist Level Viewfinder Market

Why this preview matters for 2026 corporate strategy

For executives facing portfolio prioritization in 2026, the waist-level viewfinder (WLV) segment represents a classic “small but strategic” market: stable demand with pockets of high-margin premium activity and a broad aftermarket/accessory ecosystem. The market’s modest growth profile demands discrimination — capital and R&D must be allocated to initiatives with clear value multipliers. Our report surfaces the operational levers and market signals that will decide winners in the next 18–36 months: product architecture choices, channel and accessory partnerships, pricing cadence for entry vs. premium SKUs, and an evidence-driven approach to product nostalgia (retro optics) versus modern ergonomics.

Waist Level Viewfinder Market

Key strategic takeaways

- Stability with selective upside: With a low-single-digit CAGR, the sector rewards efficiency, premium differentiation, and aftermarket/ecosystem play rather than pure volume bets.

- Concentrated competitive dynamics: The upper tier of manufacturers captures the majority of value — enabling incumbents to defend margins but leaving niches for agile third‑party innovators.

- Accessory market as a growth vector: Low-cost optical WLV accessories for mirrorless and digital bodies have emerged as a rapid adoption channel that can expand addressable demand without major product development cycles.

- Product innovation is directional: Prototypes and retro-inspired digital approaches are validating consumer appetite for tactile, optical shooting experiences, but companies must translate interest into clear product roadmaps and monetization strategies.

What the PW Consulting report contains — practical, transaction-ready insight

This study is designed as a working guide for product strategists, commercial leaders, M&A teams, and channel partners. It is intentionally operational, with sections that include:

Waist Level Viewfinder Market

- Market modelling and scenario matrices that translate the base year (2025) into risk-weighted revenue pathways across 2026–2032.

- Product and feature roadmaps delineating where optical-only, hybrid optical-electronic, and retro-mirror solutions create distinct value propositions.

- Go‑to‑market playbooks for OEMs and accessory makers, covering direct-to-consumer, specialist retail, and wholesale bundling strategies.

- Buyer persona mapping and pricing benchmarks to align SKU architecture with professional, fine‑art, and consumer segments.

- Channel and aftermarket maps showing where low-cost accessories expand distribution versus where premium interchangeable solutions reinforce brand equity.

- M&A and partnership heatmaps identifying target archetypes (technology enablers, accessory specialists, legacy-brand custodians) and valuation logic under different integration scenarios.

- Supply chain resilience checklists and cost-to-serve models calibrated for small-batch premium manufacturing and low-cost accessory production.

- Scenario planning for three external shocks (rapid mirrorless adoption, component price inflation, and nostalgic demand surge) with response playbooks.

Competitive landscape — who to watch and how they play

The market is shaped by a mixture of iconic heritage manufacturers, new entrants, and nimble accessory makers. Our competitive chapter combines company-level strategic profiles with capability maps and suggested counterplays.

- Hasselblad (Gothenburg, Sweden) — A heritage medium-format manufacturer that integrates waist-level viewfinders into its V-system and H-series product ecosystems. Their strength lies in brand equity, professional channel relationships, and high-margin positioning. For challengers, the strategic lesson is to focus on differentiated ergonomics or service bundles rather than trying to outcompete on brand prestige.

- Mamiya (Japan) — A historical player with a strong presence in the used and aftermarket space. Mamiya’s legacy support and second-hand ecosystem keep a baseline of demand alive for interchangeable waist-level systems; acquirers and aftermarket service providers can monetize this installed base through certified refurbishment programs and branded accessories.

- Ulanzi (China) — A rapid mover in the accessory tier, recently launching compact optical WLVs for mirrorless cameras with cold shoe mounts and switchable framelines. Ulanzi’s playbook focuses on low-cost, high-turnover accessories that expand the market by lowering the cost of experimentation for consumers.

- CHI (Chinotechs, China) — Introduced a metal-bodied optical WLV with retro styling and durable construction. Their strategy illustrates an effective middle path: premium-feel accessories at accessible price points that appeal to hobbyists and prosumers seeking tactile shooting experiences.

- Reflx Lab (China) — Specializes in compact universal WLV accessories optimized for compatibility across cold shoe platforms. Their modular approach underscores a growing premium on cross-platform interoperability in the accessory segment.

- Canon (Tokyo, Japan) — An instructive entrant via prototype launches at CP+ 2026 showcasing digital cameras with waist-level optical viewing. Canon’s approach is a signal to incumbents and accessory makers that larger OEMs are exploring retro-inspired, tactile products — potentially widening distribution opportunities but also elevating competitive stakes if prototypes move to production.

Recent developments to integrate into 2026 planning

- Major OEM prototypes showcased at CP+ 2026 indicate a renewed interest in mirror-based optical interfaces for digital bodies — a product development signal that can influence component sourcing and partnership timelines.

- Multiple third-party launches in late 2025 demonstrate rapid commercialization of low-cost WLV accessories compatible with modern mirrorless systems. These products serve as both market expanders and segmentation clarifiers: they attract hobbyists and reduce friction for brand switching.

- Accessory pricing dynamics — accessory makers are successfully deploying aluminum-bodied optical viewfinders at accessible price points — which supports volume growth in adjacent accessory channels but pressures OEMs to articulate premium features that justify higher price tiers.

Strategic recommendations for 2026

Our recommendations distil modelling insights and competitive scans into executable priorities for 2026:

- For established OEMs: Prioritize a dual-path product roadmap — defend high-margin interchangeable systems for professional users while validating limited-run, retro-inspired digital products through pre-orders or controlled market tests. Use prototypes and user co-creation to de-risk launches.

- For accessory specialists: Scale compatibility-first products rapidly while building a services layer (calibration, framed guides, soft-case bundles) that lifts average order value and customer lifetime value.

- For retailers and distributors: Curate assortments that pair low-cost trial accessories with premium, brand-defining solutions. Position experiential retail events (hands-on demo days) to convert tactile interest into premium purchases.

- For investors and M&A teams: Target mid-sized accessory manufacturers with strong OEM relationships or legacy-brand custodians with demonstrable aftermarket revenue streams. Integration value will come from channel synergies and the ability to scale low-cost accessories across global mirrorless adoption curves.

- For supply chain leaders: Implement flexible sourcing strategies — small-batch metal fabrication for premium accessories and modular sourcing for plastic or optical components — to manage cost volatility while preserving launch agility.

Signals to watch in 2026

- OEMs moving from prototype to limited production runs — a transition that would materially shift competitive dynamics.

- Accessory pricing and margin compression in key channels — an indicator of commoditization and the need to differentiate through service and ecosystem features.

- Growth in aftermarket and refurbishment — evidence that second‑hand demand is a durable revenue stream, especially for medium-format legacy systems.

Closing note — how this report helps you act in 2026

PW Consulting’s Waist Level Viewfinder Market report is structured to be actionable: a concise strategic narrative backed by financial modelling, market concentration analysis, product roadmaps, channel blueprints, and M&A heatmaps. It provides the context and tools required to convert modest market growth into focused, high-return initiatives. If your 2026 planning includes product launches, accessory partnerships, or M&A activity in the photographic optics value chain, this report calibrates risk, highlights practical levers, and spells out near-term plays to capture share without overcommitting capital.

For the full dataset, granular segmentation, and downloadable modelling templates that support scenario-based board decisions, please refer to the report landing page (full access is required to view proprietary segment-level figures and appendices). PW Consulting’s analysts remain available to deliver bespoke workshops that translate the report’s findings into a one‑year operational plan and product launch playbook.

For detailed analysis of this topic, please visit the official page:Waist Level Viewfinder Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com