HDD Suspension Market 2026: Strategic Imperatives from PW Consulting’s Latest Industry Brief

As enterprises and hardware OEMs prepare 2026 roadmaps for storage infrastructure, PW Consulting’s new HDD Suspension Market report delivers the kind of actionable intelligence that separates reactionary responses from proactive strategy. Built on a six-year historical base and a seven-year forecast horizon, the study synthesizes market sizing, technology trajectories, supplier economics, and supply-chain stress tests to help commercial leaders, procurement teams, and R&D heads make materially better decisions in the year ahead.

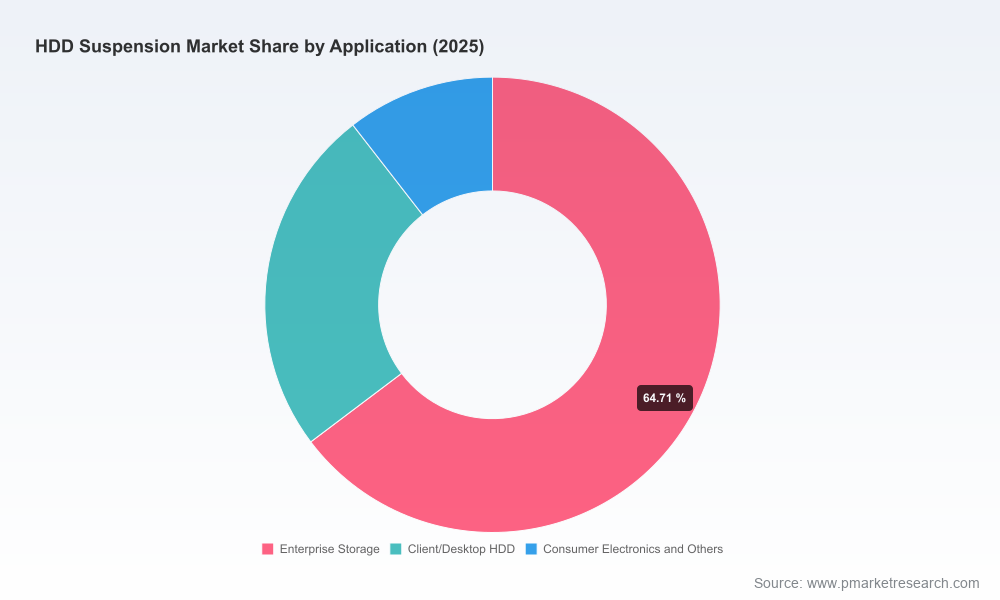

Hdd Suspension Market

Why 2026 is a Pivotal Year

Our analysis shows the HDD suspension market—a critical yet often underappreciated element of disk-drive performance and cost—has demonstrated resilience through cyclical demand swings. After recovering from mid-decade volatility, the global market reached an assessed USD 480.0 Million in our 2025 base year. Under our central scenario, the market is projected to grow at a compound annual growth rate (CAGR) of 4.15% over the forecast period, reaching roughly USD 638.06 Million by 2032.

Hdd Suspension Market

Those topline figures, however, mask important inflection points that will determine supplier viability and buyer risk in 2026: continued miniaturization and higher areal density requirements; integration of micro-actuators and PZT technologies; and persistent supply-side constraints around key raw materials and subcomponents. The report unpacks these dynamics and converts them into prioritized actions for corporate decision-makers.

Hdd Suspension Market

What the Report Contains: Practical Tools for Decision Makers

- Robust market model: Time-series market sizing (2020–2025) and scenario-driven forecasting (2026–2032) with sensitivity testing against demand shocks, price volatility, and technology adoption curves.

- Supplier benchmarking suite: Comparative scorecards for production footprint, technology readiness, quality certifications, and financial resilience—designed to support sourcing rationalization and dual-sourcing strategies.

- Technology roadmaps: Evidence-based timelines for micro-actuator adoption, flex and wire suspension evolutions, and HAMR/PMR-related integration challenges—paired with implications for qualification cycles and design-for-manufacturing.

- Cost and margin playbooks: Bottom-up cost models and margin sensitivity tables that quantify the impact of raw-material swings (e.g., stainless steel input costs) and labor-rate changes on supplier pricing and buyer TCO.

- Supply-chain risk matrices: Actionable mitigation plans for component lead-time spikes (notably PZT micro-actuators), export-control exposure, and single-source dependencies.

- M&A and partnership scouting: Heatmaps highlighting acquisition targets, JV synergies, and capability gaps where strategic investments can accelerate access to advanced suspension technologies.

- Regulatory & compliance checklists: Practical compliance steps for cleanroom and manufacturing standards that now affect qualification timelines and audit requirements.

Competitive Landscape: Who Matters and Why

The HDD suspension market is highly consolidated, with concentration metrics underscoring the dominance of a small set of specialized suppliers. Our report highlights that the top three suppliers account for a very large share of market supply, and the top five are nearly ubiquitous across enterprise qualification programs—creating both strategic dependency and bargaining leverage.

- NHK Spring Co., Ltd. (Yokohama, Japan) — A global leader in precision gimbal assemblies and flex suspensions, NHK Spring remains a technology pacesetter. Its October 2025 product launch for next-generation suspensions designed for 30TB+ PMR drives underscores the company’s R&D focus on micro-actuator integration.

- Hutchinson Technology Incorporated (HTI) (Hutchinson, MN, USA) — Known for PZT-enabled and wire-suspension designs, HTI’s June 2025 supply qualification with a leading enterprise HDD OEM is a bellwether for its competitiveness in high-capacity data-center platforms.

- Tatsuta Electric Wire & Cable Co., Ltd. (Osaka, Japan) — A specialist in flex circuit suspensions, Tatsuta’s November 2024 flex upgrades supporting higher per-platter densities demonstrate its alignment with client HDD performance roadmaps.

- Suzhou Jinfu Precision Industry Co., Ltd. (Suzhou, China) — A regional manufacturing powerhouse supplying critical load beams and base plate components to OEMs; its scale in precision stamping makes it a key node in short-cycle production.

- Nippon Micro Metal Co., Ltd. (Osaka, Japan) — Focused on precision metal parts essential to suspension reliability, Nippon Micro Metal’s capabilities matter where micron-level tolerances impact yield and field reliability.

For buyers and investors, the practical implication is twofold: first, qualification cycles are increasingly long and costly, so early engagement with leading suppliers is decisive; second, because the market is concentrated, any operational disruption at a major supplier can produce rapid ripple effects across procurement and production timelines.

Supply-Chain Dynamics and Operational Risks

- Raw-material pressures: Steel-strip inputs used for load beams have experienced notable price uplift driven by upstream supply shocks. These cost moves have direct pass-through into supplier pricing and can compress margins for thinly capitalized producers.

- Labor and capacity: Skilled assembly labor markets in Southeast Asia are tightening, raising localized costs and elongating labor ramp timelines for precision assembly lines.

- Component lead times: Critical subcomponents—most notably PZT micro-actuators—are facing extended lead times, with procurement windows that can extend many months. Buyers must re-evaluate safety-stock policies and qualification priorities in response.

- Regulatory and geopolitical constraints: Cleanroom standards are now non-negotiable for qualifying suspension vendors. Parallel to this, export controls on advanced manufacturing equipment introduce executional complexity for suppliers with facilities in affected jurisdictions.

Strategic Recommendations for 2026 Decision-Making

Based on our integrated modeling and supplier fieldwork, PW Consulting recommends that commercial and engineering leaders focus on a compact set of strategic moves in 2026 to preserve uptime, cost competitiveness, and time-to-market.

- Prioritize dual-path qualification: Qualify at least two suppliers for each critical suspension family—one global leader and one regional manufacturer—to balance performance and supply resilience.

- Negotiate raw-material escalation mechanisms: Rework contractual terms to include transparent cost pass-through formulas or shared-savings clauses tied to steel and specialty-alloy indices to reduce contentious pricing cycles.

- Invest in subcomponent inventory selectively: For components with structural lead-time risk (e.g., PZT actuators), adopt a risk-weighted inventory policy—protect platform launches with strategic buffers while avoiding excessive working capital drag.

- Embed manufacturing compliance into supplier scorecards: Make ISO cleanroom certification and control over export-sensitive equipment part of ongoing supplier performance monitoring and renewal criteria.

- Accelerate design-for-manufacture (DFM) initiatives: Align suspension design choices with available supplier capabilities to reduce qualification cycles and yield risk; leverage modular designs to facilitate supplier interchangeability.

- Monitor consolidation opportunities: Given the market concentration, targeted M&A or strategic partnerships can be accretive to capability and margin—especially where bolt-on technologies (micro-actuators, flex circuits) reduce end-system risk.

How PW Consulting’s Report Supports Execution

We designed this study to be immediately actionable. Beyond the executive narrative, clients receive a toolbox of deliverables—editable cost models, supplier scorecards, scenario runners, and a prioritized action plan tailored to specific buyer archetypes (OEM, contract manufacturer, enterprise storage buyer). The report’s datasets and models are intended to be operationalized into 2026 procurement cycles, R&D planning, and investment committees.

Next Steps and Where to Find the Full Intelligence

The public summary above outlines the strategic contours that will guide smart decisions in 2026. For procurement directors, VP-engineering, and corporate strategists who require the underlying datasets, scenario runs, and supplier-level assessments, PW Consulting provides those detailed deliverables via our full report package and client workshops.

To access the comprehensive models, supplier scorecards, and qualification checklists that underlie the forecasts and recommendations presented here, please visit our official report page. The detailed segmentation tables, granular regional and application breakdowns, and downloadable templates are reserved for report subscribers to preserve the integrity of competitive insights and to support actionable deployment.

Final Note

In a market characterized by technological nuance and concentrated supplier power, the difference between smooth platform launches and costly delays often comes down to the depth of supplier relationships, foresight in inventory and qualification planning, and the ability to translate macro trends into micro-operations. PW Consulting’s HDD Suspension Market report is designed to sharpen that translation—and to put pragmatic, risk-calibrated options on the table for 2026.

For detailed analysis of this topic, please visit the official page:Hdd Suspension Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com