How Are Construction Services in Riyadh Changing in 2026 and What Does That Mean for You?

Home |

2026-06-30 13:20:18

PW Consulting today releases an executive briefing summarizing the strategic value of our full Packaged Baked Goods Market report for corporate planning in 2026. Designed as a decision-ready roadmap, the report translates market-scale dynamics, competitive positioning, regulatory pressure, and raw-material risk into actionable options for CEOs, commercial leaders, supply‑chain chiefs, and investors. Below we outline the high-level storylines and decision levers that matter this year — while reserving the granular sub‑segment forecasts and SKU-level analytics for subscribers of the full report.

Packaged Baked Goods Market

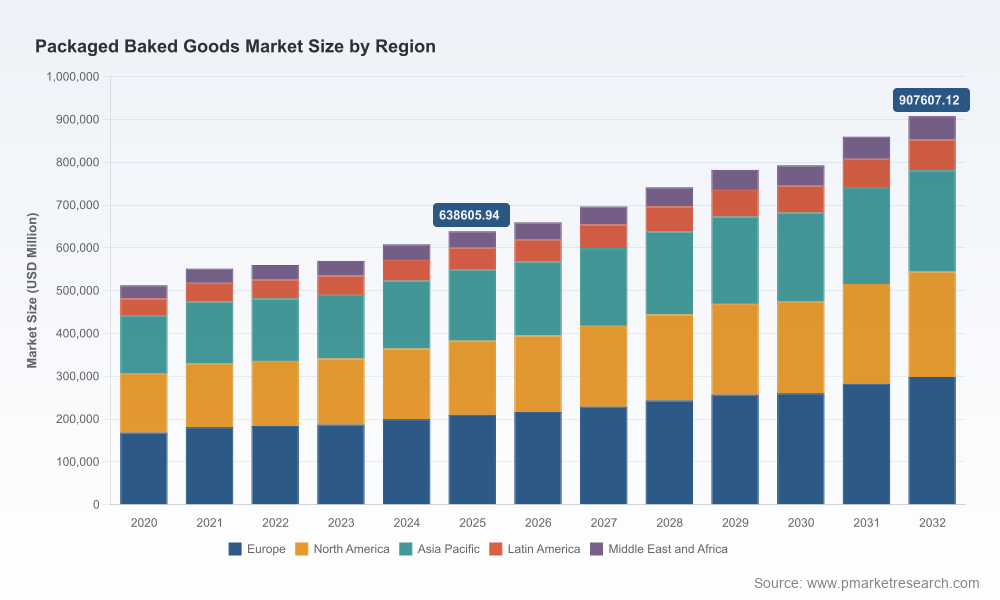

The packaged baked goods market is in a multi-year growth phase that is both broad and resilient. After steady expansion during 2020–2025, the market reached roughly USD 638.6 billion in 2025 and is projected to grow at a mid-single-digit compound annual rate. Our base forecast shows sustained expansion from 2026 through 2032, taking the market to roughly USD 907.6 billion by the end of the forecast window — representing a structural opportunity for firms that can align portfolio, price and channel strategy to evolving consumer preferences.

Packaged Baked Goods Market

Two structural features are important for 2026 planning. First, the market remains fragmented: the top three players account for under 15% of industry revenue and the leading five players account for less than one‑fifth, underscoring persistent local and niche competition. Second, growth is not uniform by route-to-market or product archetype; premiumization, health/functional claims, and convenience formats continue to pull share from legacy SKUs — a theme that will accelerate as retailers and foodservice partners reset assortments.

Packaged Baked Goods Market

Scale matters, but so does focus. Low concentration means national/global players can still win through distribution scale and procurement advantage — but targeted investments in product differentiation and retailer collaboration are often higher-return than broad-based share-chasing.

Margin compression is a real operational threat. Input-cost volatility (notably wheat-flour pricing and packaging inputs), coupled with retailer promotional intensity, will pressure margins. Our modelling shows hedging strategies, supplier consolidation, and logistics optimization produce more immediate margin relief than price-led measures alone.

Regulatory and packaging risk shifts the investment calculus. New front-of-package nutrition proposals and the expanding patchwork of Extended Producer Responsibility (EPR) rules mean 2026 is the year to finalize compliance roadmaps and pilot sustainable-packaging formats — delaying action risks expensive retrofitting later.

The market’s fragmented shape creates distinct strategic archetypes. Global platform players, regional champions, and specialty innovators each have different playbooks. Below is a synthesis of incumbent positioning and the likely strategic moves we expect to see through 2026.

Grupo Bimbo (Mexico City) — A distribution-first global leader. Their scale and bakery-centered supply chain make them a natural orchestrator of private-label and own-brand growth in multiple markets. In 2026 they are likely to double down on procurement synergies and frozen/fresh integration to defend margins.

Mondelēz International (Chicago) — Sweet-snack dominance with strong biscuit and cookie franchises. Expect continued brand-extension and channel-focused innovations (snack formats, on-the-go packs) to capture incremental occasions, particularly in convenience and impulse segments.

Flowers Foods (Thomasville) — A U.S. fresh-packaged specialist recently active with product-line innovations (keto and organic variants). Their playbook in 2026 centers on premium and health-forward SKUs while protecting fresh logistics networks against cost inflation.

General Mills (Minneapolis) — Multifaceted player pairing bakery-related brands with broader cereal/snack capabilities. We expect stronger cross-category promotional tie-ins and more deliberate e‑commerce pricing experiments from them.

Yamazaki Baking (Tokyo) — A quality- and freshness-driven operator whose international expansion targets urban convenience markets. Their strength in localized product innovation makes them a fast follower for region-specific flavor trends.

Associated British Foods / Warburtons / Aryzta / Britannia / Nestlé / Hostess and others — Collectively these players illustrate two trends: (1) established brands using R&D and line extensions to defend core categories, and (2) opportunistic consolidation where frozen or foodservice adjacencies create scale benefits. Expect targeted M&A and JV activity around frozen bakery and ingredients in 2026.

Specialist and private-label challengers — New entrants and regional specialists continue to win distribution through retailer exclusives, private-label contracts, and niche health claims. Their agility creates a continuous churn opportunity for incumbents who do not maintain a rapid NPD cadence.

Product innovation and premiumization: recent product launches show a push into keto, organic, and ready-to-bake formats. Companies that can industrialize these innovations without excessive cost will capture disproportionate share.

Ingredient and safety incidents: voluntary recalls and allergy alerts underline how quickly operational incidents can erode retailer trust and shelf presence. Robust traceability, allergen-control programs, and rapid recall protocols are now baseline requirements.

Ingredient-price and tariff pressures: wheat-flour price trajectories and 2025 tariff shifts materially increase input cost risk. Our scenario work indicates that broad tariffs and packaging-price uplifts can raise input-costs by a mid-single-digit to low-double-digit percentage — forcing companies to choose a mix of absorption, tactical price moves, and product reformulation.

Labeling and packaging regulation: proposed front-of-package nutrition labeling and state-level EPR requirements create a two-front compliance challenge in 2026: update packaging artwork and develop circular packaging pathways. Both require capital and longer lead times.

The complete Packaged Baked Goods Market report is structured for immediate use by commercial and operations teams. Highlights include:

Quantitative demand scenarios that blend consumer-incidence modeling with channel-shift sensitivities and price-elasticities — usable as inputs to P&L and SKU-pricing models.

Proprietary supplier-benchmark toolkit for ingredient risk: this flags concentration of critical inputs, identifies hedging pathways, and models the impact of tariffs and freight on cost-to-serve.

Channel playbooks for supermarkets, convenience, online, and specialist retailers that rank levers by execution complexity and short/medium-term revenue impact.

A readiness matrix for packaging and labeling regulation that sequences compliance steps by legal lead time, technical feasibility, and capex intensity.

Competitive heatmaps and capability assessments for 14 leading companies — focused on go-to-market, R&D intensity, manufacturing flexibility, and sustainability program maturity.

Actionable implementation roadmaps (90‑, 180‑, and 360‑day plans) for pricing, NPD pipeline rationalization, and supply‑chain resilience — complete with KPIs and owner templates.

Immediate (0–3 months): finalize input-cost pass-through and promotional plans; validate recall/traceability readiness; commence packaging artwork updates in line with anticipated FOP rules.

Near term (3–12 months): invest in reformulation pilots to maintain margin under higher input-cost scenarios; launch a targeted premium/health sub-line with clear retailer pilots; secure alternative suppliers for critical inputs and lock logistics capacity.

Medium term (12–36 months): implement EPR-compliant packaging strategy, scale best-performing new products, and pursue selective M&A to acquire frozen/foodservice capabilities or to consolidate regional manufacturing footprints.

Two simple facts make the 2026 planning cycle pivotal: the market’s scale is large enough that small percentage share moves materially affect revenue, and regulatory and input-pressure timelines compress decision windows. PW Consulting’s report converts those macro realities into prioritized, executable moves — not only by indicating where demand will be, but by showing how to operationalize growth with measurable impact on margin and risk.

This briefing is a curated preview of the report’s strategic recommendations. The full report includes the granular segment forecasts, SKU- and channel-level analytics, and downloadable financial models required to run board-level scenarios and execution plans. For access to the complete dataset, proprietary scoring tools, and customizable implementation templates, please visit our report page or contact PW Consulting’s industry desk.

PW Consulting stands ready to convert these insights into a tailored 2026 action plan — from cost containment and NPD acceleration to regulatory compliance and M&A readiness.

For detailed analysis of this topic, please visit the official page:Packaged Baked Goods Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com