Enzymatic Wound Debridement Market 2025 2031: Recent Trends, Growth Analysis & Strategic Outlook

Other |

2026-03-16 15:32:31

PW Consulting’s latest market research on Magnetic Clamping Technology frames 2026 as the inflection year for operational leaders, OEMs, toolmakers and investors who want to convert incremental productivity gains into sustained competitive advantage. Anchored on a 2025 base year and a 2026–2032 forecast horizon, the study projects the global market to expand at a compound annual growth rate (CAGR) of 6.45% and provides multi-scenario financial models that map a path to an estimated market size by the end of the forecast period. The analysis synthesizes market sizing, competitive benchmarking and implementation tools to guide capital allocation, procurement and product strategy decisions through 2026 and beyond.

Magnetic Clamping Technology Market

Magnetic clamping is no longer a niche workholding solution. It sits at the intersection of three irreversible trends: accelerated factory automation, the pursuit of cycle-time reduction in high-mix manufacturing, and tighter regulatory and cleanroom requirements for plastics and rubber processing. For executives planning 2026 investments, three practical implications are immediate:

Magnetic Clamping Technology Market

Our report quantifies these dynamics in a data-driven framework—using validated inputs from 2020–2025 historical performance and scenario modelling across 2026–2032—so leaders can stress-test the outcomes of alternative investment choices without waiting for market signals that will be late and imprecise.

Magnetic Clamping Technology Market

The report is intentionally operational. It is structured to be used in procurement negotiations, product development roadmaps and corporate-strategy offsites. Key deliverables include:

To honour the “preview” framing of this release, we describe the scope and strategic value of these modules here, reserving the proprietary numeric splits and granular regional/application tables for the full report download.

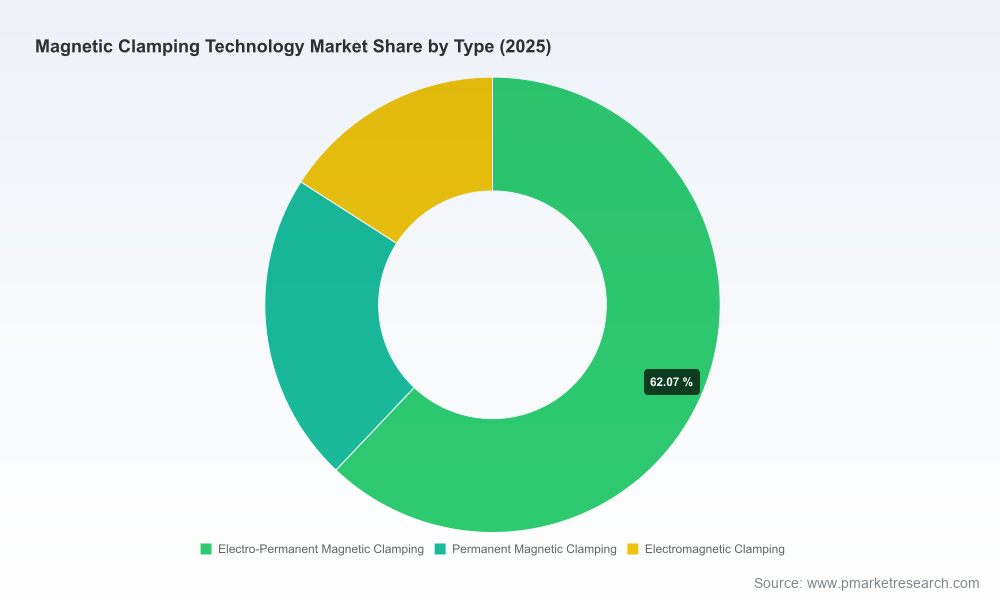

The magnetic clamping landscape combines a set of established global engineering leaders with technically specialised regional players. Market concentration indicates that leading vendors control a meaningful share of the market, but there is room for differentiated competitors to win in vertical niches and through system integration.

Recent market activity underscores an active innovation and commercialization cycle: trade-show demonstrations and product launches across 2025–2026 signal intensified go-to-market efforts and cross-technology integrations. These developments create near-term differentiation opportunities for buyers willing to pilot next-generation chucks and quick-change systems.

Raw-material dynamics are now a board-level issue for magnetic clamping suppliers and their buyers. High-performance systems frequently rely on neodymium-containing magnets; in 2026, neodymium oxide traded at elevated levels, reflecting sustained demand from electric vehicles and wind turbines. The broader rare-earth market also remains substantial and growth-driven.

Strategic levers to mitigate this risk (and covered in detail in the report) include:

Regulation is simultaneously a constraint and a commercial enabler. The introduction of standards such as ISO 23582-1:2023 establishes uniform expectations for the design and safe integration of magnetic clamping systems on plastics and rubber machines. Separately, electro-permanent systems intended for mold clamping are increasingly aligned with cleanroom classes (ISO Class 7 and 8), and their “energy-only-on-switching” characteristic supports low-emission factory designs.

For decision-makers, regulatory readiness converts to faster procurement cycles and lower integration friction. The report provides a compliance checklist and test protocols so buyers can specify verifiable requirements in tenders and acceptance testing.

Below are prioritized actions tailored to common strategic profiles. These are designed for rapid adoption in 2026 planning cycles.

This article intentionally describes the report’s methodological approach and strategic outcomes while withholding detailed subsegment tables and region/application splits to preserve the “preview” value for our subscribers. The full report contains detailed market-by-region, by-type and by-application models, vendor-level financial estimates, downloadable Excel models, playbooks for pilots and rollouts, and a workshop kit for translating findings into a 12-month implementation plan.

Executives planning capital deployment, procurement negotiation or M&A activity in 2026 should request the complete report and schedule a customised briefing. PW Consulting can also deliver scenario workshops that adapt our models to client-specific machine fleets, tooling mixes and geographic footprints.

Contact PW Consulting to access the full Magnetic Clamping Technology Market report, obtain vendor scorecards and secure a tailored 90-day implementation roadmap designed to convert insight into measurable operational and financial outcomes.

For detailed analysis of this topic, please visit the official page:Magnetic Clamping Technology Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com