Brine Preparation Systems Market 2026: Strategic Imperatives from PW Consulting’s New Industry Report

Executive preview

As organizations finalize capital plans for 2026, decisions around brine preparation systems carry outsized consequences across food processing, winter maintenance, chemical manufacturing, and industrial water treatment. PW Consulting’s latest market study delivers a directional intelligence package designed to convert market visibility into executable strategy. Our analysis tracks market development from 2020 through a 2026 baseline and extends to 2032, quantifying an expected market progression that reflects steady, technology-driven expansion. The headline: the global brine preparation systems market continues on a multi-year growth path, with an implied compounded momentum that informs investment timing, technology selection, and supply‑chain hedging.

Brine Preparation Systems Market

Market snapshot: scale and trajectory

PW Consulting’s modeling shows the market expanding from its early‑decade base to a materially larger opportunity by the end of the current forecast window. After recovering and stabilizing across 2020–2025, the market advances into the 2026–2032 forecast period at a mid-single-digit compound annual growth rate (CAGR). Our numeric projections for the full market are included in the report and form the basis for scenario modeling used throughout our advisory outputs. Complementing top‑line expansion is a moderate level of supplier concentration—large incumbents hold a meaningful share of the competitive landscape, leaving room for specialized and regional challengers to win through product differentiation and service models.

Brine Preparation Systems Market

Why 2026 is pivotal for procurement and R&D leaders

Three converging forces make 2026 a strategic inflection point for firms evaluating brine infrastructure:

Brine Preparation Systems Market

- Operational maturity of automation: Automated and semi‑automated systems have matured to a point where lifecycle cost advantages are clearer than ever—particularly where process consistency, reduced salt consumption, and labor optimization are priorities.

- Raw material & input volatility: Salt and related feedstock dynamics—illustrated by historically low unit pricing in some geographies and rising demand in chemical value chains—mean procurement strategies will materially alter operating margins unless addressed with inventory and supplier diversification plans.

- Regulatory and sustainability pressure: Environmental rules tied to de‑icing runoff and chloride discharge are already shaping specification requirements and will increasingly favor systems with tighter controls, metering, and traceable usage data.

Operationally actionable deliverables in the report

PW Consulting’s report is structured to be immediately operational for corporate strategy, procurement, and engineering teams. Key practical components include:

- Investment playbooks that translate top‑line scenarios into recommended CapEx phasing—covering retrofit vs. greenfield choices and quick‑win upgrades for automation and process controls.

- Vendor selection matrices and scorecards customized for different buyer archetypes (municipal fleets, large food processors, industrial OEMs), enabling rapid short‑listing and RFP design.

- Unit‑economics templates and ROI calculators to assess total cost of ownership across manual, semi‑automatic, and fully automated systems, including sensitivity to salt price and labor cost inputs.

- Regulatory impact maps showing where specification changes matter most and what mitigation levers (e.g., dosage control, pre‑wetting vs. blended strategies) materially reduce compliance costs.

- Implementation roadmaps that sequence pilot, scale, and operations handover, with risk registers tied to supply‑chain constrictions and commissioning bottlenecks.

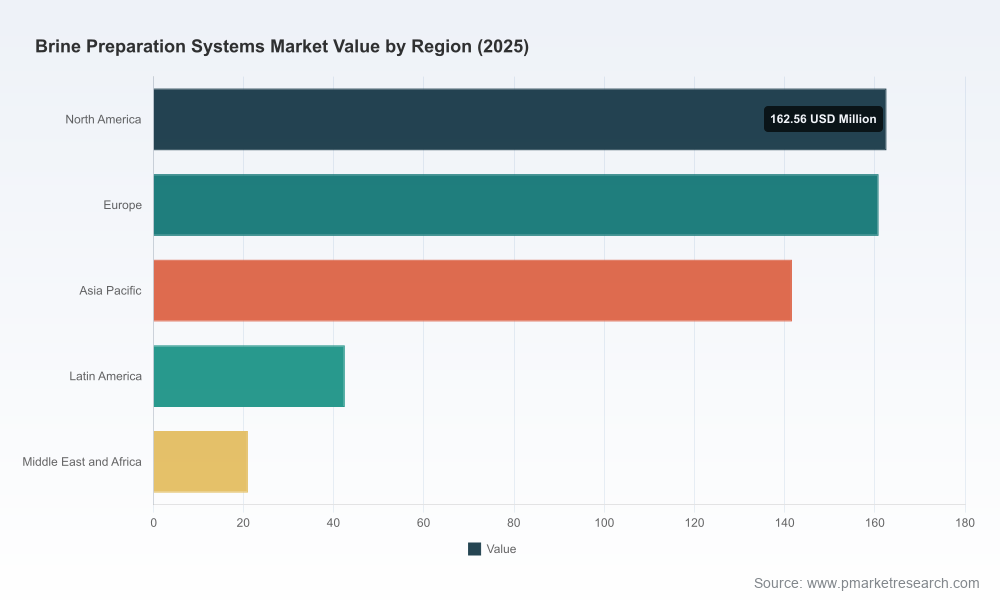

To preserve commercial value for our subscribers and corporate clients, the report intentionally omits publication of detailed sub‑segment and regional numeric splits in this public summary. Those granular tables and downloadable models are provided on the report landing page and within client‑level deliverables.

Demand drivers and market dynamics

Three demand vectors are shaping system selection and vendor opportunity:

- Food industry quality and yield optimization: Food processors prioritize consistent brine concentration, mixing repeatability, and hygienic design to improve product yield and reduce rework. Innovations in automated dosing and mixing controls directly translate to margin uplift in high‑volume processing lines.

- Municipal and winter maintenance efficiency: Municipalities and contractors are adopting brine systems to lower salt usage per lane mile while improving pre‑treatment logistics. Environmental restrictions on runoff and community pressure for lower chloride loads are accelerating interest in metered, traceable brine delivery.

- Industrial feedstock growth: Increased demand for caustic soda and PVC in certain regions has lifted the importance of consistent brine quality for chloralkali processes; this industrial segment values throughput reliability and integration with downstream chemical handling systems.

External contextual signals underpin these dynamics. For example, the industrial salts market remains substantial, driving supply and logistics attention; meanwhile, granular salt trade flows into some markets influence local brine production economics. PW Consulting’s regional briefs map these supply‑chain dependencies in proprietary detail for clients.

Competitive landscape: incumbent capabilities and white‑space

The supplier ecosystem is diverse, spanning specialized brine equipment makers, global process OEMs, and commodity vendors extending into brine services. The market’s current structure—neither atomized nor monopolized—creates opportunities for both scale players and niche innovators.

- BrineMaker Inc. — Strength: intelligent briner design with U.S. manufacturing footprint optimized for logistics. Strategic focus should be on leveraging digital controls and aftermarket service contracts to expand lifetime value.

- GEA Group — Strength: industrial process pedigree and systems like MixMaster that emphasize hygiene and efficiency. Multinational reach positions GEA well for large food processors seeking single‑vendor system integration.

- BAK Food Equipment — Strength: operator‑focused customization for protein and seafood processors; competitive edge in minimizing downtime through robust mechanical design.

- AccuBrine & VariTech — Strengths: municipal and winter‑maintenance automation, upflow technologies and a focus on reducing chloride and salt usage. These vendors are attractive partners for public sector pilots seeking measurable environmental outcomes.

- GVM Inc., Camion Systems, Brine Masters, and other U.S. specialists — Strengths: practical product portfolios for highway and municipal customers, often at compelling price‑performance points that win in high‑volume, cost‑sensitive RFPs.

- Cargill Deicing Technology — Strength: global dealer network and integrated supply model, coupling feedstock supply with equipment options to create bundled offerings for large public clients.

- NOWICKI USA, Rhino Manufacturing, AUTOBrine, Marlo, Pengwyn, Dultmeier — Strengths: niche engineering options, corrosion‑resistant materials, modular capacity and touch‑screen controls; attractive to processors requiring high food‑safety standards or compact footprints.

Strategic implications: buyers should map vendor capabilities to the specific value metric they prioritize—throughput, salt reduction, hygiene compliance, or lifecycle cost. Vendors competing on hardware alone will find margins compressed; those layering software, service, and supply integration will capture disproportionate value.

Risks and watch‑points for 2026 decision cycles

- Supply volatility: Regional salt supply and logistics can shift the economics of centralized brine production. Hedging strategies and multi‑source procurement reduce exposure.

- Regulatory tightening: Anticipate incremental restrictions on chloride discharge and de‑icing runoff. Systems offering precise metering and telemetry will be easier to certify and operate under stricter regimes.

- Integration complexity: Retrofitting automated brine systems into legacy process lines often uncovers hidden costs. Our implementation playbooks highlight common failure modes and mitigation steps.

- Consolidation pressure: Expect middle‑market consolidation among equipment makers; acquirers will target companies with both installed bases and recurring aftermarket revenue.

How PW Consulting helps you act

For executives preparing 2026 procurement and R&D roadmaps, the report translates market intelligence into prioritized action. Typical engagements we facilitate include vendor due diligence, procurement RFP development, pilot design and measurement, ROI validation, and M&A target screening. Our public release is intentionally a “trailer”: it demonstrates methodological rigor and strategic insight while directing buyers and investors to the full dataset and the proprietary annexes that drive transactional decisions.

Next steps and access

Leaders seeking to convert these insights into a 2026 action plan should request the full report and our executable toolset. The complete deliverable includes the granular segmentation tables, regional forecasts, detailed vendor scorecards, and editable financial models that underpin the recommendations summarized here. PW Consulting is available for workshops to align executive priorities, tailor the procurement matrix to your risk profile, and run vendor selection simulations that quantify tradeoffs between cost, compliance, and continuity.

In a market where incremental improvements in mix control, metering, and automation directly lift yield and reduce environmental footprint, the right brine preparation strategy is both an operational improvement and a strategic differentiator. PW Consulting’s report equips you to make those decisions with clarity and confidence for 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Brine Preparation Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com