Ophthalmic OCTA Equipment Market: Strategic Imperatives for 2026 — PW Consulting Report Preview

The ophthalmic optical coherence tomography angiography (OCTA) equipment market is entering a phase of accelerated clinical adoption and commercial re-pricing that will materially affect strategic decisions in 2026. PW Consulting’s latest market study — based on 2020–2025 historical tracking and a 2026–2032 forecast horizon — synthesizes revenue trajectories, reimbursement shifts, regulatory milestones and competitive manoeuvres into an actionable playbook for device manufacturers, hospital systems, imaging groups and investors. This release highlights the report’s strategic value while intentionally withholding detailed segment datapoints to encourage access to the full dataset on our portal.

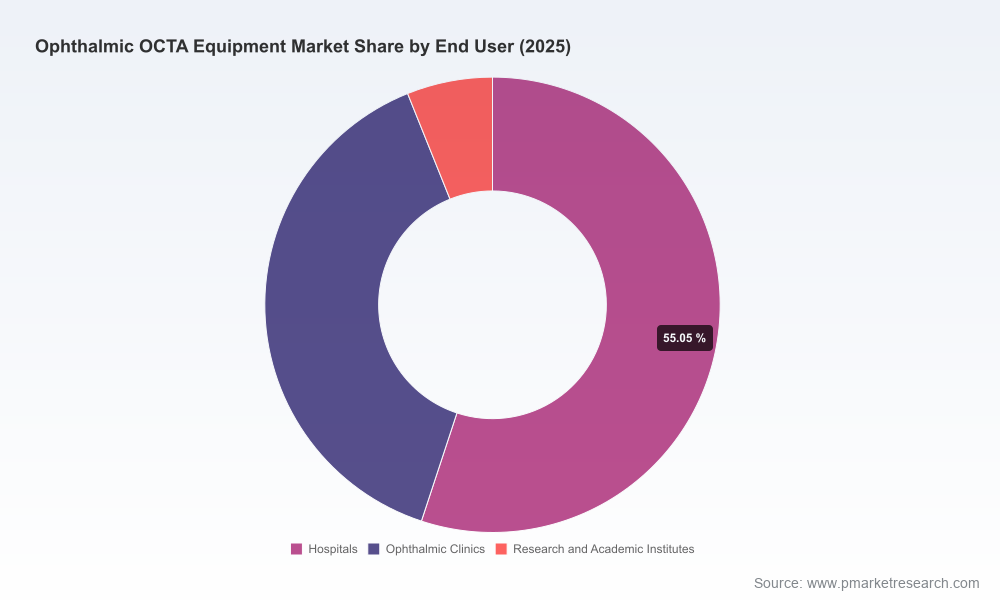

Ophthalmic Octa Equipment Market

Market snapshot: growth momentum and what it means for planning

Our topline modelling shows the global OCTA equipment market expanded meaningfully through the first half of the decade and is positioned for sustained double‑digit-like growth over the medium term. From a measured base at the start of the decade, the market reached a material inflection point by the 2025 base year and is projected to continue expanding into the 2026–2032 forecast window at a compound annual growth rate (CAGR) of approximately 9% (report currency USD, revenue unit: Million). For procurement and portfolio planning in 2026, this translates into a larger addressable market and heightened competition for capital allocations — both for new equipment acquisition and for software/service ecosystems that monetize imaging outputs.

Ophthalmic Octa Equipment Market

Drivers fuelling near‑term demand

- Reimbursement realignment: The introduction of CPT code 92137 in 2025 for OCT angiography — with a higher national average reimbursement compared to standard OCT codes — materially improves per‑scan economics for practices adopting OCTA. Importantly, billing rules (for example, restrictions on same‑day billing with certain other OCT codes) change the revenue calculus and workflow optimization requirements for clinics and hospitals.

- Regulatory progress and vendor innovation: Recent clearances and CE marks for next‑generation swept‑source and high‑speed spectral systems have reduced technical barriers to wider clinical use, particularly in retinal and glaucoma diagnostics and in challenging patient populations (supine, pediatric).

- Clinical maturation: As OCTA evidence matures across diabetic retinopathy, AMD and optic nerve disease, clinical pathways are incorporating angiographic imaging earlier in care algorithms, shifting demand upstream toward diagnostic capital investment.

- Capital dynamics: Hospital capital budgets and procurement behavior remain a key constraint. While median capital budgets remain significant, a substantial subset of executives continue to plan for cuts or deferred purchases given macro uncertainty; conversely, facility-level depreciation patterns and aging infrastructure are forcing selective investments that prioritize modular, upgradeable platforms.

Strategic implications for 2026 decision‑makers

For corporate executives, product teams, purchasing committees and private investors, three strategic themes should drive 2026 planning:

Ophthalmic Octa Equipment Market

- Shift from feature competition to solution economics. With reimbursement differentials favoring OCTA-enabled diagnostics, companies should foreground total cost of ownership, throughput optimization and post‑sale service bundles. Vendors that can demonstrate faster acquisition times, higher patient throughput and integrated billing/workflow tools will have an advantage when competing for constrained capital budgets.

- Design modular upgrade paths. Hospitals and multi‑site ophthalmic groups are increasingly prioritizing systems that can be upgraded via software or modular hardware swaps rather than full replacement. Manufacturers that offer clear migration routes (e.g., SD‑to‑swept‑source upgrades, optional OCTA modules) can capture higher lifetime customer value and reduce procurement friction.

- Operationalize reimbursement capture. The presence of a higher‑valued CPT code for OCTA is an opportunity, but realizing uplift requires operational changes — training billing teams, adjusting scheduling to avoid disallowed code combinations, and integrating angiography into standard care pathways. Vendors that provide turnkey coding playbooks and analytics to demonstrate revenue uplift will win more procurement decisions.

Competitive landscape: practical takeaways

The market continues to be shaped by a set of established imaging OEMs and more agile regional innovators. Leading companies deploy differentiated strategies — high‑end systems emphasizing wide‑field and deep imaging, compact integrated units targeting clinic workflows, and upgradeable platforms that bridge research and clinical needs. Recent regulatory milestones underscore these strategic paths: examples include CE marking for advanced swept‑source platforms enabling EU commercialization and multiple FDA clearances that expand use cases into pediatric and supine imaging.

- High‑performance platforms: Several legacy optics manufacturers continue to push the envelope on scan speed, axial resolution and wide‑field angiography — capabilities that command premium pricing in tertiary referral centers and research hospitals.

- Flexible, upgradeable systems: Providers offering modular SD‑OCT systems with optional OCTA upgrades and software licensing models are winning in high‑volume clinic environments where capital discipline is acute.

- Regional challengers: New entrants and regional OEMs emphasize price‑performance and rapid service networks, capturing share in markets where procurement teams prioritize short lead times and local support.

For procurement teams, the competitive consequence is straightforward: do not evaluate systems solely on headline throughput or vendor brand. Our research shows procurement outcomes improve when evaluation matrices include upgradeability, service SLAs, coding/billing support and lifecycle cost scenarios that model deferred capital vs. upgrade vs. replacement.

Risk vectors that will influence 2026 outcomes

- Reimbursement policy nuances and coding restrictions that create inadvertent workflow penalties if not implemented carefully.

- Capital spending uncertainty across hospital systems that can delay large purchases despite clinical need.

- Regulatory variability across jurisdictions that affects time‑to‑market for new imaging modalities and workflow innovations.

- Convergence with multimodal imaging and AI analytics — vendors that fail to integrate value‑added software risk commoditization of hardware.

What the PW Consulting report contains (practical, operational, ready to deploy)

Our full report is built as a practitioner’s toolkit for 2026 decision cycles. Highlights include:

- Topline market sizing and validated forecasts (base year 2025, forecast 2026–2032) with scenario modelling under multiple reimbursement and capital‑spend conditions.

- Commercial due‑diligence templates for vendor selection and procurement, including RFP scorecards that weight technical, financial and operational criteria.

- Reimbursement playbook that translates CPT coding changes into revenue scenarios, sample billing workflows and risk mitigation steps to avoid rejected claims related to code bundling.

- Deployment & integration guidelines for hospital and multisite clinic environments covering IT interoperability, image archiving, staff training and patient throughput optimization.

- Technology roadmaps comparing spectral‑domain and swept‑source OCTA architectures, upgrade paths and timing recommendations aligned with product life cycles and regulatory filings.

- Market entry and partnership frameworks for vendors assessing geographic expansion, channel partnerships or OEM co‑development agreements.

- Competitive profiles and strategic assessments of the primary OEMs, including recent regulatory clearances and product positioning — enabling faster benchmarking without needing to parse raw technical specifications.

- Financial models and valuation comparators aimed at M&A and private equity evaluation, with sensitivities for price erosion and software monetization.

How to convert insight into action in 2026

For each stakeholder group we recommend targeted actions in 2026:

- OEMs and product leaders: Prioritize modular upgradeability and integrate coding/billing support as part of the commercial offering. Accelerate regulatory clearances in priority markets to lock early adopters.

- Hospital procurement and health systems: Run TCO analyses that incorporate projected reimbursement uplift from OCTA and weigh retention strategies (service contracts, trade‑in programs) to manage depreciation and capital constraints.

- Clinical leaders: Pilot OCTA‑first diagnostic pathways in high‑volume retinal and glaucoma clinics with robust measurement of throughput, diagnostic yield and reimbursement realization.

- Investors and PE firms: Focus on platform plays that combine hardware with recurring software and AI analytics revenue streams; target assets with clear upgradeability and established service networks.

Conclusion and next steps

As 2026 planning cycles begin, ophthalmic OCTA equipment presents both opportunity and complexity. Higher reimbursement for angiography, accelerating regulatory approvals, and expanding clinical use cases create a favorable market tailwind. At the same time, capital constraints, coding intricacies and the imperative to bundle hardware with software and services complicate go‑to‑market strategies. PW Consulting’s full report converts these dynamics into executable roadmaps, procurement templates and financial models designed to support confident decisions in 2026.

For the complete dataset, segmented analysis, and downloadable decision tools referenced in this preview, please consult the full report on our website. Our clients receive the underlying spreadsheets, scenario models and vendor playbooks needed to implement the strategies outlined above.

For detailed analysis of this topic, please visit the official page:Ophthalmic Octa Equipment Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com