Europe Food Certification Market Trends, Challenges, and Forecast 2025 –2032

Health |

2026-06-22 06:39:44

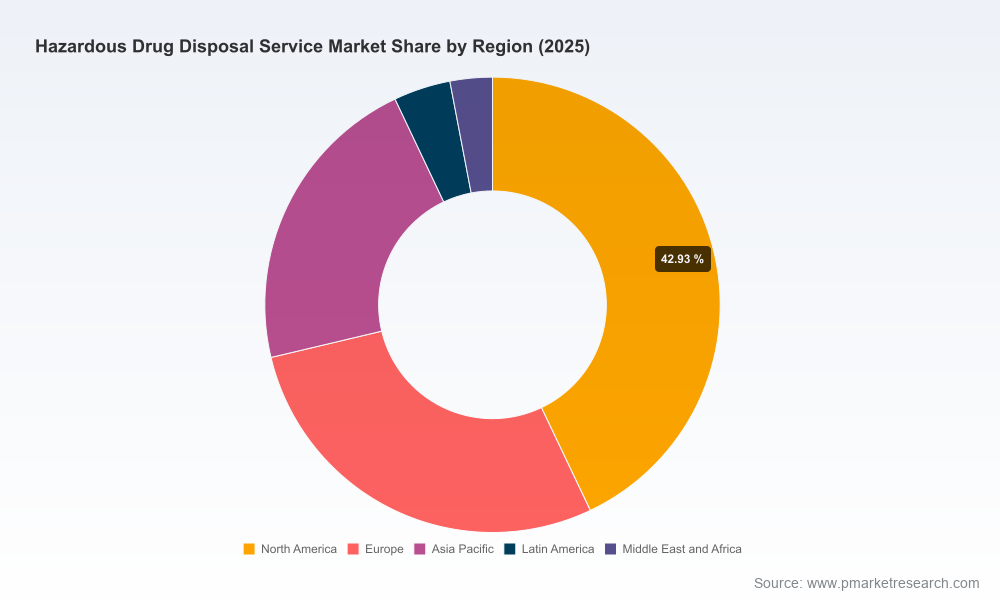

As healthcare systems, regulators, and waste-management providers enter 2026, the hazardous drug disposal service market is evolving from a compliance-driven niche into a strategic operating category with measurable implications for cost, patient and worker safety, and institutional risk. PW Consulting’s latest market study synthesizes five years of historical trends, a seven-year forecast horizon (2026–2032), primary interviews, and supplier benchmarking to equip executives with the decision-ready intelligence needed this year. The market is expanding at a compound annual growth rate (CAGR) of 7.34%; it grew from under USD 1.0 billion in 2020 to approximately USD 1.35 billion in 2025, and our base-case projection takes total revenues above USD 2.2 billion by 2032. These macro trajectories matter for capital planning, procurement design, and regulatory compliance investments in 2026.

Hazardous Drug Disposal Service Market

Regulatory acceleration: The patchwork adoption of EPA’s Hazardous Waste Pharmaceuticals Rule (Subpart P) across multiple states, combined with ongoing emphasis on USP General Chapter <800>, is turning previously discretionary segregation and disposal practices into auditable obligations. The EPA’s January 2026 guidance clarifying household medication disposal and RCRA management standards has further raised expectations for traceability and end-to-end control in certain care settings.

Hazardous Drug Disposal Service Market

Operational complexity: Increased outpatient chemotherapy, expansion of specialty clinics, and evolving pharmaceutical portfolios (including higher volumes of cytotoxic and controlled substances) are creating new waste streams and logistical challenges that standard medical-waste solutions are not optimized to handle.

Hazardous Drug Disposal Service Market

Commercial opportunity: Sustained mid-single-digit to high-single-digit CAGR means spending is meaningful and predictable, enabling suppliers to plan capacity investments and buyers to negotiate multi-year service agreements with performance incentives tied to compliance and sustainability outcomes.

This report is built for practitioners. Through a structured blend of quantitative forecasting and qualitative fieldwork, we provide:

The market exhibits a moderate level of concentration: the top three providers control a meaningful share of reported revenues while the top five extend that control to a clear majority of market activity. This structure creates a two-track strategic dynamic in 2026. On one hand, national integrators with logistics and treatment scale can offer end-to-end solutions attractive to large health systems. On the other, specialized mid-market players and regional innovators can capture share through differentiated services—such as formulary-level waste characterization, on-site neutralization technologies, and software-enabled chain-of-custody—that address specific buyer pain points. For buyers, this means opportunities to trade scale for specialization; for investors and service providers, it highlights acquisition and partnership routes that accelerate capability builds.

Our vendor analysis profiles incumbent leaders and emerging specialists across four capability vectors: compliance advisory, logistics and transport, destruction/treatment, and digital traceability. Key strategic postures we observe include:

Stericycle, Inc. — Positioned as the market leader in regulated medical and pharmaceutical waste services, Stericycle is reinforcing its regulatory advisory role, aligning client guidance with the latest Subpart P adoptions and USP <800> expectations. Recent public service updates and local procurement wins illustrate a playbook that combines compliance thought leadership with scale-based logistics.

Clean Harbors, Inc. — A dominant hazardous-waste handler with emphasis on treatment and destruction capabilities, Clean Harbors’ competitive strength lies in end-to-end hazardous material expertise and industrial-grade capacity for high-volume or complex waste streams.

Veolia Environnement S.A. — A global environmental-services integrator, Veolia brings cross-border treatment solutions—especially incineration and specialized healthcare waste handling—that appeal to multinational healthcare providers and nations upgrading centralized treatment infrastructure.

Waste Management, Inc. (WM) — Leveraging broad logistics footprints and existing relationships with healthcare systems, WM emphasizes integrated waste programs paired with sustainability commitments.

Specialized players (Daniels Health, MedPro, Sharps Compliance, US Ecology, and regional operators) — These vendors focus on secure pharmaceutical segregation, RCRA-compliant characterization, and niche services (e.g., witnessed incineration for controlled substances, formulary consulting). Their agility makes them attractive to specialty clinics and long-term-care operators.

Across these profiles, winners in 2026 will be those who combine regulatory advisory capabilities with reliable logistics, transparent traceability, and treatment capacity—backed by service-level commitments that translate regulatory risk reduction into measurable buyer value.

For healthcare providers (hospitals, clinics, long-term care): Move from tactical compliance to programmatic risk management. Conduct a rapid gap analysis against USP <800> and Subpart P, prioritize segregation protocols, and embed contractual clauses for witnessed destruction and audit access. Use multi-year procurement vehicles that incorporate compliance KPIs and price collars for volatile treatment costs.

For waste service providers: Differentiate by adding regulatory advisory services, granular chain-of-custody reporting, and investing in capacity for controlled-substance destruction. Consider partnerships with digital-traceability vendors to offer verifiable audit trails that reduce buyer operational burden.

For investors and corporate development teams: Prioritize targets that bring complementary capabilities—software traceability, treatment capacity, or specialty compliance consulting. The market’s moderate concentration suggests attractive roll-up economics, particularly where regional specialists can be scaled into broader integrated offerings.

This release is a strategic preview designed to surface the issues and opportunities that should shape 2026 planning cycles. The full report contains the comprehensive datasets, regional and end-user splits, detailed vendor scorecards, financial models, primary interview excerpts, and appendices that operational teams require to execute. To preserve the advisory value of the research and to encourage direct engagement, we have intentionally withheld segment-level tables and some granular contract benchmarks from this preview; purchasers of the full study will gain immediate access to those deliverables and to customized consulting sessions for rapid implementation.

Regulatory clarity in 2026 and predictable market expansion create a rare window for healthcare organizations and waste-service investors to convert compliance imperatives into strategic advantage. PW Consulting’s Hazardous Drug Disposal Service Market study equips leaders with the playbooks, financial tools, and supplier intelligence needed to act with confidence. For organizations that prioritize traceability, treatment certainty, and contractual discipline this year, the payoff will be reduced regulatory exposure, predictable costs, and a defensible sustainability narrative. For those that delay, 2026 is likely to bring higher audit risk and cost volatility.

PW Consulting — In-depth analysis, actionable recommendations, and implementation-ready tools to turn 2026 regulatory and market shifts into durable advantage.

For detailed analysis of this topic, please visit the official page:Hazardous Drug Disposal Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com