Intellectual Disabilities Service Market 2026: Strategic Imperatives for Providers, Payers, and Investors

PW Consulting today publishes its authoritative industry briefing accompanying the full Intellectual Disabilities Service Market report. Built on a five‑year historical base (2020–2025) and a seven‑year forecast horizon (2026–2032), the study synthesizes regulatory shifts, reimbursement dynamics, operational bottlenecks, and competitive moves that will shape decisions in 2026. In aggregate, the market reached approximately USD 424.5 billion in our 2025 base year and is projected to grow at a compound annual growth rate (CAGR) of 6.19% through 2032, reaching roughly USD 646.8 billion under our central scenario. These headline metrics frame a sector at once large, socially critical, and strategically attractive — yet fundamentally fragmented.

Intellectual Disabilities Service Market

Why this briefing matters for 2026 strategy

Health systems, managed care organizations, community providers, and private investors face three converging forces in 2026: (1) sustained public funding and shifting Medicaid program designs, (2) accelerating adoption of home- and community‑based services (HCBS) and digital therapeutics, and (3) persistent workforce constraints that force operational innovation. Our report translates these macro drivers into actionable choices — from capital allocation and M&A playbooks to payer contracting and front‑line staffing models. Importantly, the broad market size and mid‑single digit growth trajectory underscore that the sector is large enough for scale plays yet small and dispersed enough that localized execution matters.

Intellectual Disabilities Service Market

Market structure and competitive posture

The Intellectual Disabilities Service market remains highly fragmented: the three‑ and five‑firm concentration ratios are low (CR3 ≈ 8.5%; CR5 ≈ 12.3%), signaling a landscape dominated by regional providers, non‑profits, and mission-driven organizations rather than a handful of national giants. Fragmentation creates two strategic realities: it preserves plenty of buy‑and‑build opportunity for acquirers and places a premium on integration capabilities for firms seeking to scale outcomes, compliance, and margins.

Intellectual Disabilities Service Market

- Provider archetypes: national multi‑service platforms, regional community‑based specialists, clinical behavioral health players, and technology‑enabled therapy vendors each play distinct roles. The winners will be those that combine regulatory mastery, payer relationships, and repeatable workforce models.

- Payer dynamics: government and public funding remain the dominant payor of services in many markets, while private insurance and out‑of‑pocket channels are growing as complementarity opportunities — particularly for tele‑rehabilitation and specialized clinical pathways.

- Consolidation prospects: recent transactions demonstrate active strategic realignment, but low market concentration suggests many tuck‑in opportunities remain for scale‑seeking platforms.

Recent strategic moves — what they reveal

- Sevita’s acquisition of ResCare Community Living (completed March 2026) signals continued national consolidation focused on continuity of care and cross‑state platform expansion. Buyers are paying up for geographic reach and operational playbooks that convert public funding into consistent outcomes.

- BrightSpring’s 2025 acquisition of Community Options and subsequent portfolio adjustments underscore a twin trend: strategic aggregation of HCBS capabilities and the selective divestiture of non‑core assets to sharpen payer relationships.

- Partnerships to scale employment and supported living — exemplified by Lifeworks’ strategic alliance with The Arc — illustrate a playbook where national brands combine advocacy networks with execution capacity to win managed care contracts and philanthropic capital.

- Technology adoption is emerging beyond pilot stage: the Cerebral Palsy Alliance’s 2025 launch of CPAssist (a tele‑rehabilitation platform) shows how digital therapeutics and remote therapy platforms are moving from niche innovation to payer‑facing value propositions.

Regulatory and reimbursement inflection points to watch

Policy and reimbursement are the levers that rapidly reshape service models. Key developments highlighted in our analysis include:

- State Medicaid program design and waiver approvals: for example, New York’s OPWDD program spent significant Medicaid dollars in 2023 to serve people with intellectual and developmental disabilities — a practical illustration of how state budgets and allocation choices determine the addressable market for residential versus community services.

- Managed care expansions: Florida’s statewide rollout of an Intellectual and Developmental Disabilities Comprehensive Managed Care program in late 2025 illustrates how single‑plan models alter network participation, utilization management, and risk transfer for providers.

- Federal compliance requirements: CMS updates to HCBS quality measures and ongoing Conditions of Participation for certain institutional settings increase administrative burden but also create opportunities for providers that can demonstrate quality and outcome metrics.

- Labor market policy and rate setting: investments by states (e.g., targeted rate increases in Pennsylvania) that improve direct support professionals’ (DSP) wages have immediate operational impact, reducing vacancy rates and improving continuity of care.

What the full report delivers — practical, decision‑ready content

Our 200+ page deliverable is built as a practitioner’s toolkit for 2026. Highlights include:

- Dynamic market model and revenue forecast (historical 2020–2025; base year 2025; forecast 2026–2032) with scenario toggles for reimbursement, policy shifts, and technology adoption.

- Regulatory and payer tracker mapping federal and major state policy levers, waiver timings, and managed care rollout timelines.

- Provider benchmarking and operational diagnostics covering occupancy, staff mix, direct support professional economics, and productivity levers.

- Commercial due diligence templates and five M&A playbooks (platform build, roll‑up, capability‑buy, vertical integration, tech enablement).

- Workforce optimization and retention playbook, including compensation design, training pipelines, and technology augmentation strategies to reduce frontline turnover.

- Digital enablement roadmap (tele‑rehab, remote monitoring, care coordination platforms) with supplier matrix and interoperability considerations.

- Ten investment theses and risk assessments tailored to strategic acquirers, PE sponsors, and mission‑aligned capital allocators.

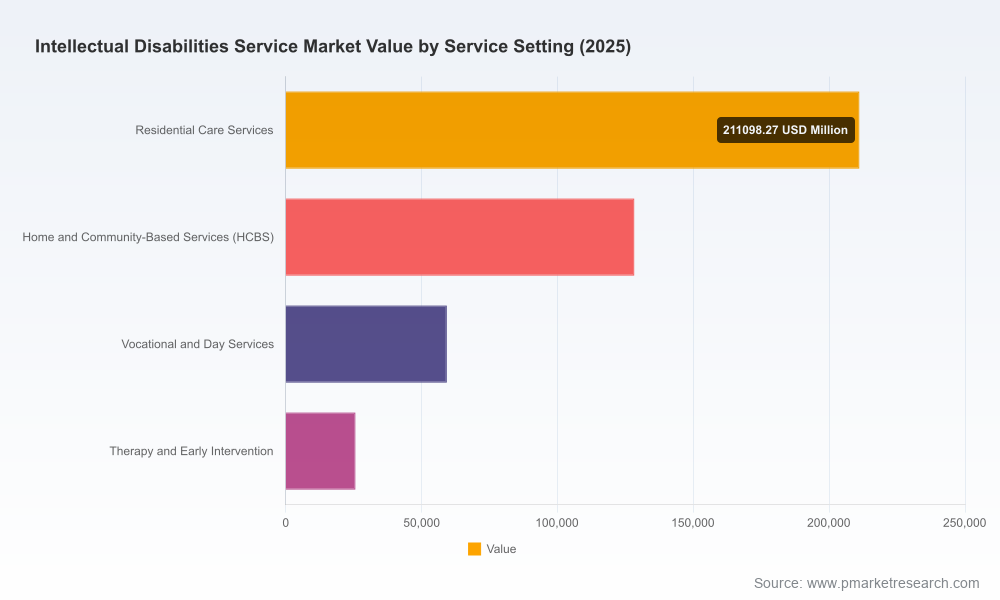

To preserve competitive confidentiality while signaling analytical depth, the public summary intentionally omits granular segment allocations and regional splits; these data and the underlying model are available with the full report and interactive dashboard.

Strategic actions for 2026 — concise playbook

- Providers: Prioritize HCBS expansion and integration with clinical care pathways; invest in standardized outcomes reporting to win value‑based contracts; and adopt focused workforce retention programs (career ladders, stabilized schedules, and targeted wage investments) to reduce churn.

- Payers: Design outcome‑based contracts that incentivize community integration and reduced institutionalization; partner with technology vendors to scale tele‑rehabilitation and remote monitoring as tools to lower total cost of care.

- Investors: Pursue roll‑up strategies where operators have replicable clinical models and compliance scale; favor asset‑light, tech‑enabled platforms that can aggregate referral flows and demonstrate defined ROI on DSP productivity.

- Policymakers and advocates: Align rate‑setting with workforce needs and quality metrics; ensure predictable funding pathways for HCBS and pooled supports; and use data to balance capacity between residential supports and community inclusion goals.

Risk factors and scenario sensitivities

Three risks materially change our central forecast if realized: abrupt Medicaid rate deferrals or cuts in one or more large states; failure to recruit and retain a DSP workforce at scale; or slow adoption of digital care models that keep per‑patient costs high. Conversely, accelerated managed care adoption with robust provider partnerships or broader telehealth reimbursement expansion could push outcomes above our central scenario.

Conclusion — an opportunity for focused, executional advantage

The Intellectual Disabilities Service market in 2026 offers a rare combination: sustained public funding and social imperative, significant fragmentation ripe for consolidation, and powerful operational levers (workforce and digital) that separate frontrunners from laggards. PW Consulting’s report equips executives with the market model, regulatory map, and execution playbooks required to convert social purpose into durable financial performance.

For the full dataset, interactive model, granular segment and regional analysis, and tailored advisory engagements, access the complete report and executive dashboard on PW Consulting’s website.

For detailed analysis of this topic, please visit the official page:Intellectual Disabilities Service Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com